Another country takes steps to cool their housing market.

Moody’s reports that changes to lending standards by the Hong Kong Monetary Authority (HKMA) will reduce the risks in the Hong Kong housing market which has been buoyant in recent years.

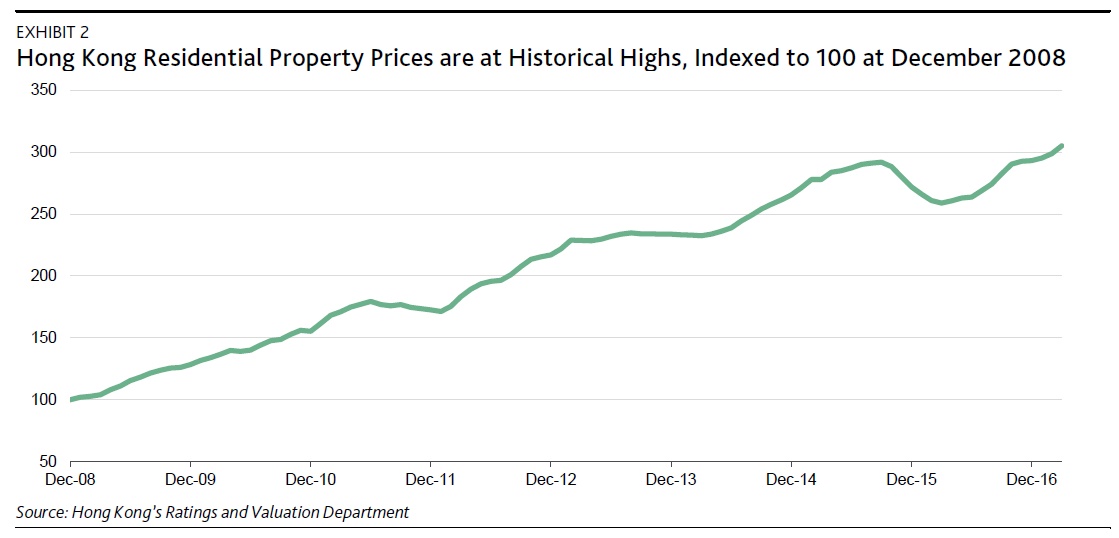

Current elevated property prices pose latent risks to the banking system and make banks increasingly vulnerable to a property price decline. According to Hong Kong’s Rating and Valuation department, residential property prices in the territory have risen for 12 consecutive months since March 2016. Average residential prices rose 4.0% in March 2017 from the end of 2016 and were 4.5% above the previous peak in September 2015.

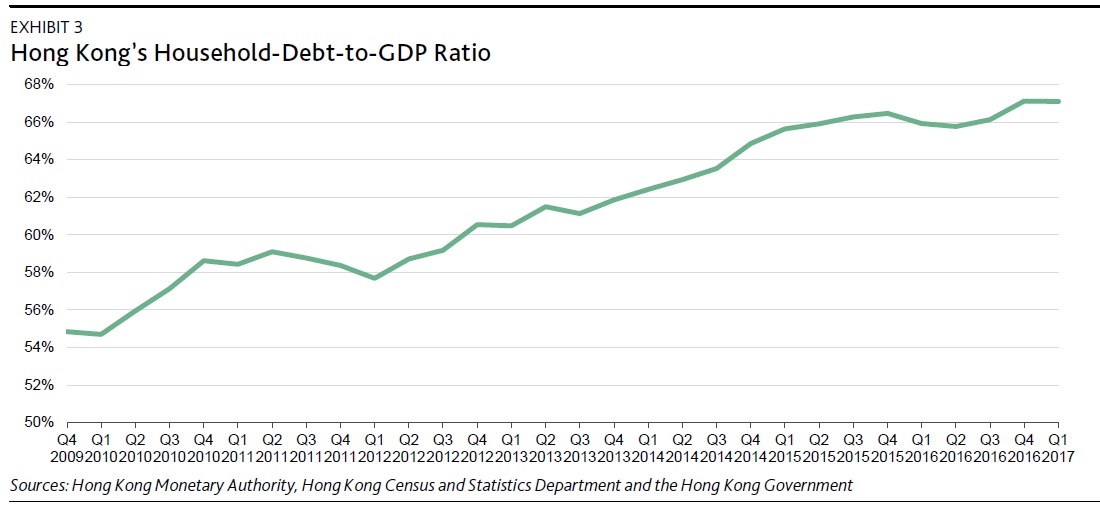

Hong Kong’s housing affordability is among the lowest in the world, with a price-to-income ratio of more than 20x. The household debt-to-GDP ratio is also at a historical high (see Exhibit 3), raising the specter of a substantial rise in household debt-servicing burden as interest rates rise.

One mitigating factor for these risks is that Hong Kong banks maintain very low loan-to-value (LTV) ratios. The average LTV ratio for new mortgage loans was 51% in March 2017. The new measures will help banks build up more buffers against potential property prices decline.

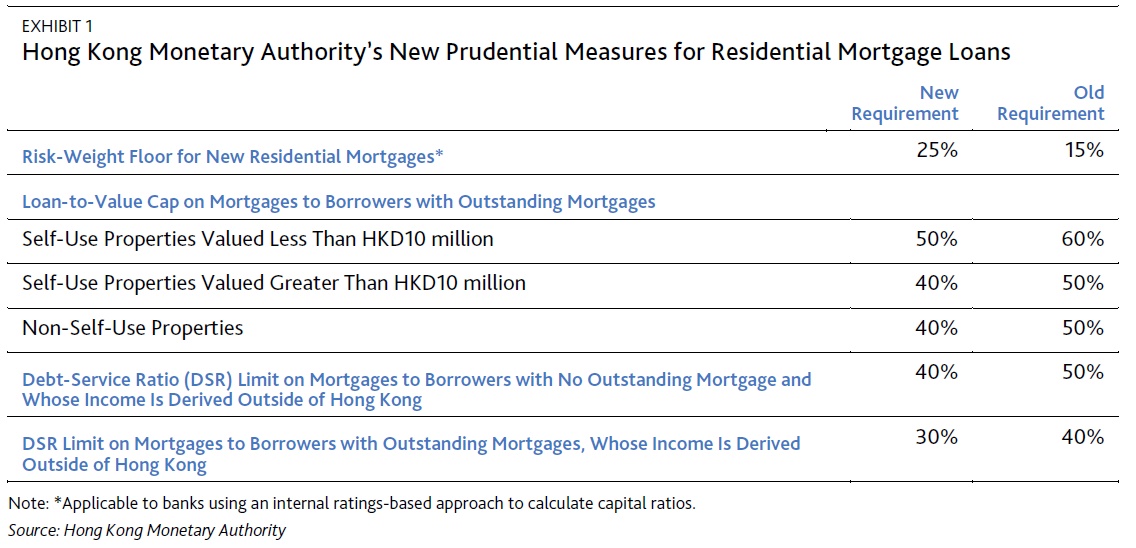

The measures are credit positive for Hong Kong banks and enhance their resilience in a potential property downturn. The new measures target non-first-time home buyers and borrowers whose income is mainly derived from outside of Hong Kong (see Exhibit 1). These measures will temper credit demands from property investors with high leverage and limit the growth of residential mortgages loans, which increased in March to record year-on-year growth of 5.3%, compared with 4.2% year-on-year growth in December 2016.

Hong Kong banks’ intense competition in the mortgage business has squeezed their interest margins. Pricing for most mortgages has come down to Hong Kong Interbank Offered Rate (HIBOR) plus 1.28% from HIBOR plus 1.7% 18 months ago. HKMA’s requirement to raise the risk weight for new residential mortgage loans to 25% from 15% should deter banks from competing for mortgage business through further price cuts.

Worth reflecting on the fact that Australia’s household debt to GDP ratio is 123, significantly higher than Hong Kong, once again highlighting the issues we have locally!