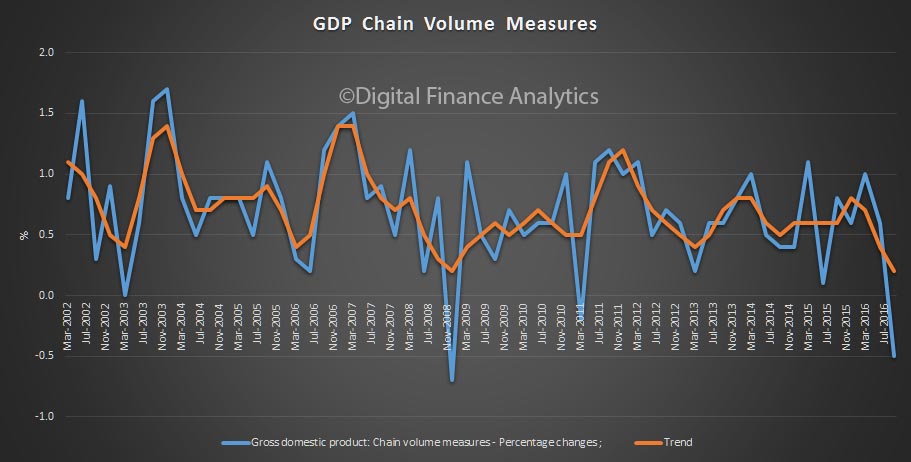

The ABS says the volume of activity in the Australian economy decreased 0.5 per cent in the September quarter 2016, the first quarter of negative growth since the Queensland flood affected March quarter 2011. Through the year growth remains positive at 1.8 per cent, reflecting the three previous quarters of growth.

This is worse than expected. So bad, there must be some questions asked about the data – for example a -0.3% “statistical adjustment”? But a rise in imports, fall in building activity, fall in household savings, and goverment spending, all could not offset a rise in household spending and agricultural exports. Another fall next quarter would make a recession, but we suspect there will be some reversals next time.

Economic activity contracted in a number of areas this quarter. Private investment in new buildings detracted 0.3 percentage points from GDP growth, while new engineering and new and used dwellings detracted 0.2 and 0.1 percentage points respectively. Public capital expenditure detracted 0.5 percentage points from growth as it declined from elevated levels in the June quarter. Net exports detracted an additional 0.2 percentage points from growth. Australia’s terms of trade rose 4.5 per cent through the September quarter.

The reduced building activity is reflected in the output of the construction industry which fell 3.6 per cent for the quarter and was the largest contributor to the fall in GDP growth on an industry basis. A number of other industries also recorded below trend growth, or declined, this quarter, including financial and insurance services, professional scientific and technical services, rental hiring and real estate services and administrative support services. The largest offset to these falls was agriculture which grew 7.5 per cent. Mining production contributed no growth, but maintained its historically high levels of production.

Subdued activity in the building industry contributed to a decline in the income of small businesses, with gross mixed income down 5.8 per cent. Private non-financial corporation’s gross operating surplus increased 1.2 per cent, supported by stronger mining commodity prices. Compensation of employees increased 1.3 per cent, and real gross national income increased 0.9 per cent for the quarter to be 3.2 per cent higher through the year.

Household final consumption expenditure increased 0.4% in seasonally adjusted terms. This was driven by a rise in Hotels, cafes and restaurants (2.2%) and Insurance and other financial services (1.3%). Government final consumption expenditure decreased 0.2% in seasonally adjusted terms.

Exports of goods and services increased 0.3% in seasonally adjusted terms. Seasonally adjusted Exports of goods fell 0.3%, with Non–rural exports down 1.2%. Non–monetary gold up 7.4% and Rural exports up 1.0%. Exports of services rose 2.4%. Imports of goods and services rose 1.3% in seasonally adjusted terms. Seasonally adjusted Imports of goods rose 0.8% with rises in Capital goods (3.5%), Intermediate goods (1.7%) and Non–monetary gold (22.5%). Consumption goods fell (–3.3%). Imports of Services were up 3.3%.

Dwelling investment fell 1.4% in the September quarter 2016 driven by New and Used Dwellings (down 1.6%) and Alterations and Additions (down 1.0%). The decline this quarter can be partly attributed to high rainfall levels. Through the year growth was still high at 7.2% and Private sector residential building approvals were more than $20.4b in original current price terms for the quarter, 9.4% higher than September quarter 2015. New building investment exhibited its strongest quarterly fall since September 2009 this quarter (falling 11.5%). The finalisation of construction projects as well as less construction work coming online drove this decrease.

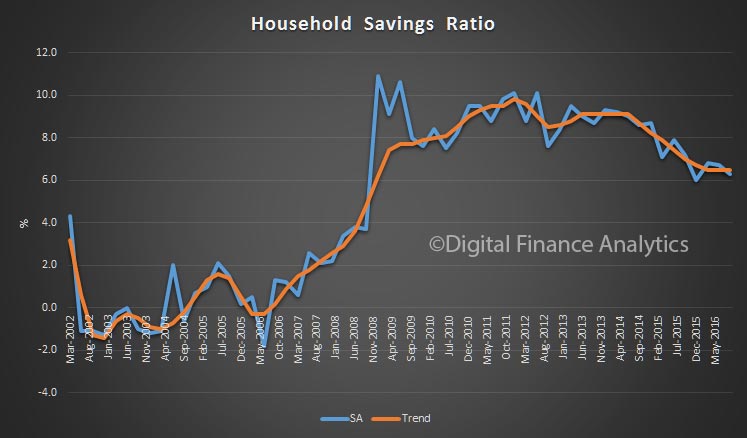

The Household saving ratio was 6.3% in seasonally adjusted terms in September quarter 2016, down from the 6.7% figure recorded last quarter. This decline was driven by a reduction in small business profits (Gross mixed income down 5.8%). The result occurred despite growth in wages and below trend growth in Household consumption.

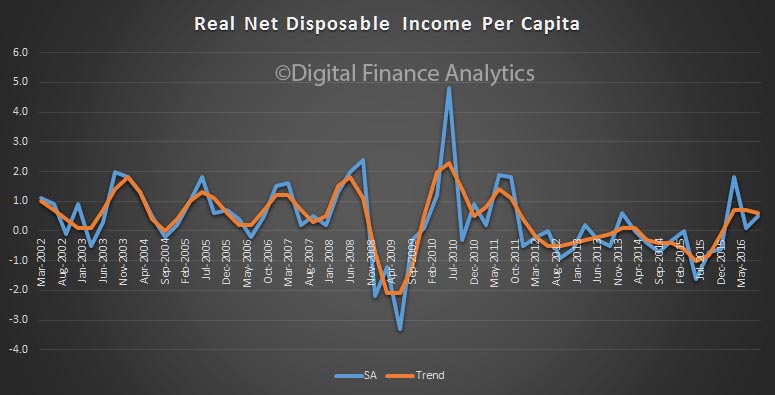

Worth noting that the real net disposable income per capital lifted a little, so not all bad news.

Worth noting that the real net disposable income per capital lifted a little, so not all bad news.