Given the near $6 trillion of residential real estate, and the near $1.6 trillion of loans on these properties, future house price dynamics are important for households, banks, regulators and the wider economy. So it is worth thinking about where house prices might go. There is no rule that house prices can only rise. In the US they fell up to 40% and in the UK up to 25% post the GFC. Domain today reported falls in many states in the past few months. In Australia, prices are way above long term trends.

Any modelling of future outcomes will be wrong. However we have been developing an econometric model which draws current data from our segmented household surveys and using a range of relationships we seek to estimate average house and unit prices by state, for properties in the main urban areas, and separately in the regional areas. Averages across Australia mask too many differences to be useful. Having used the model to track events over the past year, we feel confident enough of the algorithms to share some of the results. But to stress, this model is only a guide, and its results are wrong!!

Our point of departure is data from the ABS on house and unit prices. We overlay our survey data with a range of factors to drive our modelling from a range of sources. These include:

- Supply of property by type (building approvals and construction)

- Demand for property by type (from the DFA survey)

- Population growth and demography (combination of DFA survey and ABS)

- Income growth (from ABS)

- Unemployment rate (from ABS)

- Inflation rate (from ABS)

- GDP Growth rate (from ABS)

- Demand for finance (from the survey)

- Supply of finance (RBA and ABS data)

- Interest rates (RBA)

- Mortgage interest margins (RBA and DFA analysis)

- Mortgage underwriting interest rate floors (APRA)

- Choice modelling between investment types (DFA survey)

- Choice modelling between property types (DFA survey)

- Tax breaks (DFA survey and ATO)

- Mortgage default rates (Various, including DFA survey)

- Lender mortgage write-downs (Company results)

- Penetration of Lenders Mortgage Insurance (DFA surveys and analysis)

We have six scenarios:

- Strong recovery

- Mild up turn

- Base case (no changes from current settings)

- Mild down turn

- Severe down turn

- Armageddon

Over the coming days we will discuss some of the initial analysis we have completed. Today, we look at NSW.

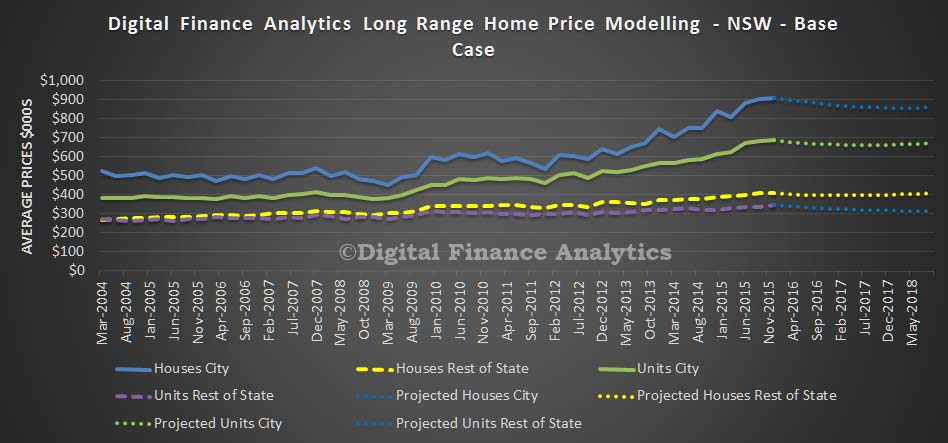

In our base case to mid 2018, we expect to see the average house price in Sydney fall by 5.5% to $860,000 and the average unit in Sydney fall by 1.2% to $400,000. In regional areas, the average house price will fall 2.5% to $395,000 and units will fall by 10.6% to $309,000.

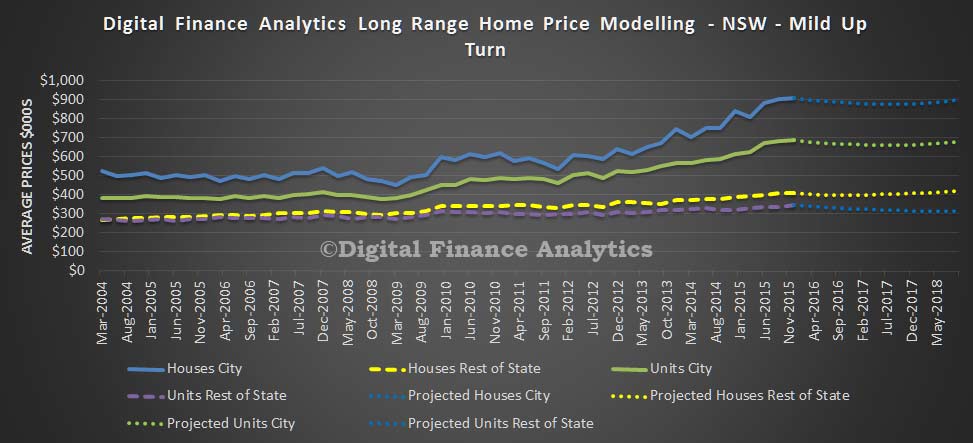

If economic momentum becomes stronger, to mid 2018, the average house price in Sydney will still fall a little, by 1.4% to $897,000 and the average unit in Sydney will fall by 1.1% to $677,000. In regional areas, the average house price will rise 3.3% to $418,000 but units will fall by 9.3% to $313,000. The falls in Sydney will continue given the previous strong run, lower demand for investment property and static incomes.

If economic momentum becomes stronger, to mid 2018, the average house price in Sydney will still fall a little, by 1.4% to $897,000 and the average unit in Sydney will fall by 1.1% to $677,000. In regional areas, the average house price will rise 3.3% to $418,000 but units will fall by 9.3% to $313,000. The falls in Sydney will continue given the previous strong run, lower demand for investment property and static incomes.

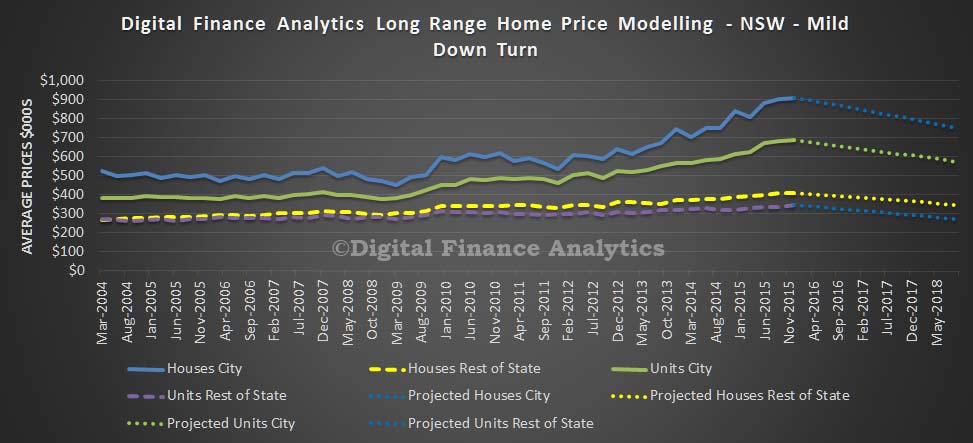

If economic momentum falls, to mid 2018, we expect to see the average house price in Sydney fall by 17.5% to $751,000 and the average unit in Sydney fall by 16.3% to $573,000. In regional areas, the average house price will fall 14.6% to $346,000 and units will fall by 21.9% to $269,000. In this scenario, growth remains low, unemployment moves higher, incomes remain flat, and demand for property slows.

If economic momentum falls, to mid 2018, we expect to see the average house price in Sydney fall by 17.5% to $751,000 and the average unit in Sydney fall by 16.3% to $573,000. In regional areas, the average house price will fall 14.6% to $346,000 and units will fall by 21.9% to $269,000. In this scenario, growth remains low, unemployment moves higher, incomes remain flat, and demand for property slows.

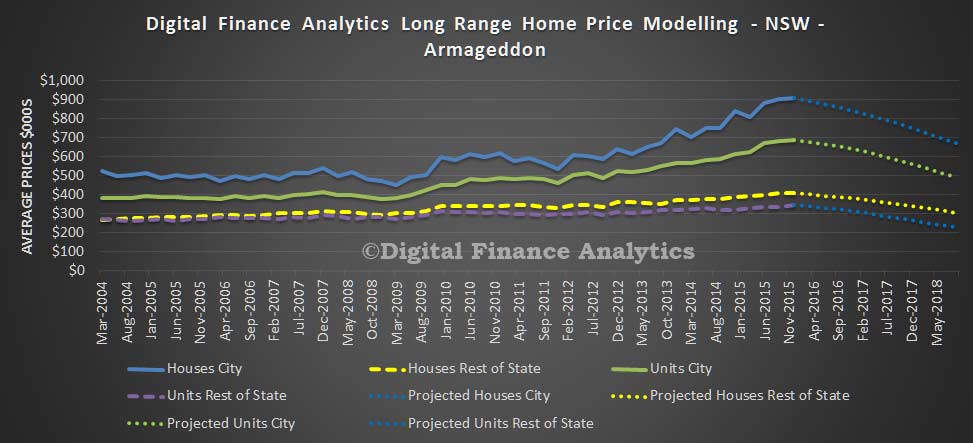

If economic momentum falls significantly, to mid 2018, we expect to see the average house price in Sydney fall by 26.1% to $672,000 and the average unit in Sydney fall by 28.4% to $490,000. In regional areas, the average house price will fall 25.2% to$303,000 and units will fall by 34.5% to $226,000. In this scenario, cash interest rates are cut further, unemployment rises, income falls in real terms, and demand for property falters. This is our Armageddon scenario.

If economic momentum falls significantly, to mid 2018, we expect to see the average house price in Sydney fall by 26.1% to $672,000 and the average unit in Sydney fall by 28.4% to $490,000. In regional areas, the average house price will fall 25.2% to$303,000 and units will fall by 34.5% to $226,000. In this scenario, cash interest rates are cut further, unemployment rises, income falls in real terms, and demand for property falters. This is our Armageddon scenario.

Our conclusion is that in NSW, there is more down side than upside in property at the moment and this will continue for some time to come. How severe the correction will be depends on the economic and growth outcomes.

Our conclusion is that in NSW, there is more down side than upside in property at the moment and this will continue for some time to come. How severe the correction will be depends on the economic and growth outcomes.

Results are rather different in other states, and we will explore these scenarios in the next few days.

3 thoughts on “Econometric House Price Modelling”