We have been watching the continued switching between owner occupied and investor loans – $1.4 billion last month, and more than $56 billion – 10% of the investor loan book over the past few months.

This has, we think been driven by the lower interest rates on offer for owner occupied loans, compared with investor loans. But, we wondered if there was “flexibility with the truth” being exercised to get these cheaper loans.

So we were interested to read the latest from UBS which further underscores the possibility of untruths being told as part of the mortgage underwriting processes – to the extent of $500bn (on a book of $1.6 trillion).

This is based on survey results from 907 mortgage applicants over the last year. There are significant differences across channels and individual lenders. The net effect is that loan portfolios contain more risks than banks believe – something which our own analysis also demonstrates.

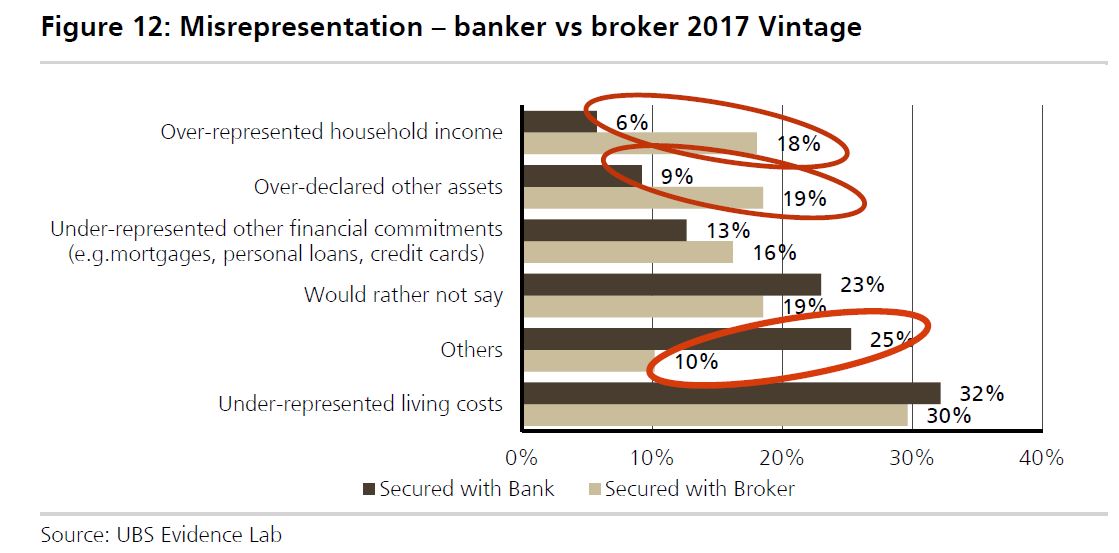

Understating living costs was the most significant misrepresentation, plus overstating income, especially loans via brokers.

In 2017 one-third of mortgage applications were not factual and accurate UBS Evidence Lab found that only 67% of respondents stated their mortgage application was “completely factual and accurate” in 2017 – a statistically significant reduction from the 2016 Vintage (72%). This year 25% of participants said their application was “mostly factual and accurate”, 8% said it was “partially factual and accurate”, while 1% “would rather not say”. By channel the level of “completely factual and accurate” mortgages fell across both brokers to just 61% (from 68%) and via the branches to 75% (from 78%). At a bank level there was a statistically significant fall in factual accuracy at NAB to 62%. While at ANZ the level of factual accuracy fell to 55% in 2017, statistically significantly lower than the Industry (99% confidence level).

Given the rising level of misstatement over multiple years we estimate there are now ~$500bn of factually inaccurate mortgages on the banks’ books (ie ‘Liar Loans’ – a term used in USA during the Financial Crisis for mortgages where documentation was not accurate). While household debt levels, elevated house prices and subdued income growth are well known, these finding suggest mortgagors are more stretched than the banks believe, implying losses in a downturn could be larger than the banks anticipate.

We are underweight Australian banks and are very cautious the medium term outlook.

Expect the normal rebuttals from the lenders, but that has more to do with protecting their positions than wanting to understand the truth – a core cultural problem across the sector.

I see super funds are now pushing a “new investment class” called “Buy to Rent” and that US fund managers were amazed that individual people could own rental properties. Why all the funds need need is a housing price crash that provide both a pool of cheap homes to buy and bankrupted people to rent them.