Australia’s retirement savings system grew to $2.1 trillion by the middle of 2016, according to new statistics published by APRA

In its Annual Superannuation Bulletin, released yesterday, APRA revealed total assets hit $2.1 trillion as at 30 June 2016.

Of that total, $621.7 billion (29.6 per cent) was held in SMSFs and $1.29 trillion was held by APRA regulated superannuation entities.

The remaining $185.5 billion comprised exempt public sector superannuation schemes ($132.2 billion) and the balance of life statutory funds ($53.3 billion).

Retail funds held 26 per cent of the total $2.1 trillion; industry funds held 22.2 per cent; public sector funds held 17 per cent and corporate funds held 2.6 per cent.

As at 30 June 2016, there were 144 APRA-regulated RSE licensees responsible for managing funds with more than four members.

Of the funds with more than four members, the annual rate of return for the year ended June 2016 was 2.9 per cent. The five-year average annualised rate of return to June 2016 was 7.4 per cent and the 10-year rate of return was 4.6 per cent.

Australian superannuation members paid $11.72 billion in fees for the 12 months to 30 June 2016, according to APRA.

The Australian Securities and Investments Commission is taking action against Westpac in the Federal Court on Thursday, alleging that two of the bank’s subsidiaries breached “best interests” obligations and provided personal financial advice when they were not permitted to do so.

ASIC claims that a campaign by Westpac designed to get customers to consolidate multiple super accounts breached the financial advice laws by giving advice based on personal financial information in 15 phone conversations.

The calls were made by staff of Westpac Securities Administration Limited and BT Funds Management Limited.

ASIC claims the bank specifically recommended customers roll out of their non-Westpac superannuation funds, consolidating into Westpac-related superannuation accounts. It also says the bank did not provide proper comparisons between the funds.

Westpac claims it did not give personal advice.

“In each of the 15 conversations … our customers were given a ‘general advice warning’ as is standard and a required part of our process,” BT said in a statement.

ASIC is also taking the gloves off over aggressive marketing by super funds, with the corporate regulator poised to launch enquiries with over 50 super groups.

The funds, believed to be mostly from the for-profit retail sector, will receive letters from ASIC in coming days seeking information about their marketing practices, a spokesman told The New Daily.

Were inducements offered?

ASIC is concerned that funds have been using inducements and high-pressure tactics to get employers to sign them up to lucrative default fund agreements which include insurance arrangements. These agreements channel workers into membership if they don’t actively choose another fund.

The regulator’s inquiries will investigate the quality of advice and information that is provided to employers by trustees when they are making decisions about their default funds for their employees. It will examine the funds’ responses to its questions before deciding on further action.

“We’ll be looking at all of the material around the super fund trustee relationship including the type of marketing collateral funds give to employers,” Gerard Fitzpatrick, senior executive leader of investment managers and superannuation at ASIC, told Fairfax Media.

There have been allegations of inducements offered to employers by funds and that these can result in employees being channelled into inappropriate funds.

What deals are members getting?

“We are very interested in how members are treated, and if as a result of aggressive marketing approaches or competitive drive, whether members are being disadvantaged or are being provided with information that does not allow them to make appropriate investment decisions.”

Areas that will come under ASIC scrutiny will include “advice given to employers and how this is paid for, as well as looking at disclosure material that is provided directly for employers by trustees and entities”.

Around one-third of Australians with super accounts are enrolled in default funds through their employers.

Competition for default fund status is hotting up in the $2.1 trillion super sector with employer-owned funds increasingly vacating the field and handing the business to dedicated industry and retail funds.

According to Australian Prudential Regulatory Authority data only 31 out of a total of 231 funds were identified as “corporate funds” for the year to June 2015.

The latest manifestation of this trend is news that Equip Super is set to merge with mining giant Rio Tinto’s corporate super fund later this year in a move that would see a $13.5 billion super group created to manage funds for approximately 75,000 members.

Last August the Reserve Bank of Australia moved its super balances over to Sunsuper to manage. BHP Billiton has also rolled its super fund into MLC.

Investors whose wealth has increased through soaring property prices and rising assets face being pushed into riskier financial products as they gain sophisticated investor status, experts say.

While it may seem like an attractive option for investors to attain a “sophisticated investor” certificate allowing them to participate in complex share placements, exotic bonds and exclusive private equity deals, experts are calling for an urgent rethink of the criteria.

“There are alarming levels of financial illiteracy across all Australian demographics,” says Mark Brimble, chair of the Financial Planning Education Council and lecturer at Griffith University.

“We can’t just assume that because someone has a certain value of assets and income that they understand these products.”

As it stands, investors with net assets – including their residential property – of $2.5 million and/or a gross income of least $250,000 a year for the last two years qualify for an SI certificate signed by an accountant. This enables them to participate in pre-IPOs, IPOs and receive tax benefits for investing in Early Stage Innovation Companies (ESICs), among other things.

But as house prices have soared – the median in Sydney is up 65.9 per cent since 2012 and Melbourne is up 48 per cent – it is much easier for people to qualify for this status.

“These criterion were meant to be a significant hurdle for people,” says Peta Tilse, managing director of Sophisticated Access and founder of Cygura, a centralised online platform for sophisticated investor certification and validation.

“But it’s become very outdated and thanks to the booming property market, including the family home, opens that sophisticated investor door right up,” says Ms Tilse.

The Australian Securities and Investments Commission (ASIC) offers client consumer protection to retail investors where financial advisors deliberately miscategorise their clients or when companies fail to properly disclose their businesses. However these protections are not available to sophisticated investors.

Another law, established in 1991, automatically upgrades an investor from retail to wholesale or sophisticated if they invest $500,000 or more in one particular product.

“It’s a law not many people know about and it was made when the average full time earnings were $19,000 per year, rather than the $80,000 now,” says Ms Tilse.

Yesterday the Treasury released, late in the day, a consultation on the “Development of the framework for Comprehensive Income Products for Retirement“. The framework appears to open the door to new products, which offer significant opportunities for industry players to invent yet more fees and charges. Just remember the biggest killer on superannuation in the accumulation phase is the level of fees and charges. We fear this exercise will open the door to more income flows to industry participants in the income draw-down phase of retirement, and raise more disclosure questions. This could be exacerbated if distributed via Robo-advice platforms.

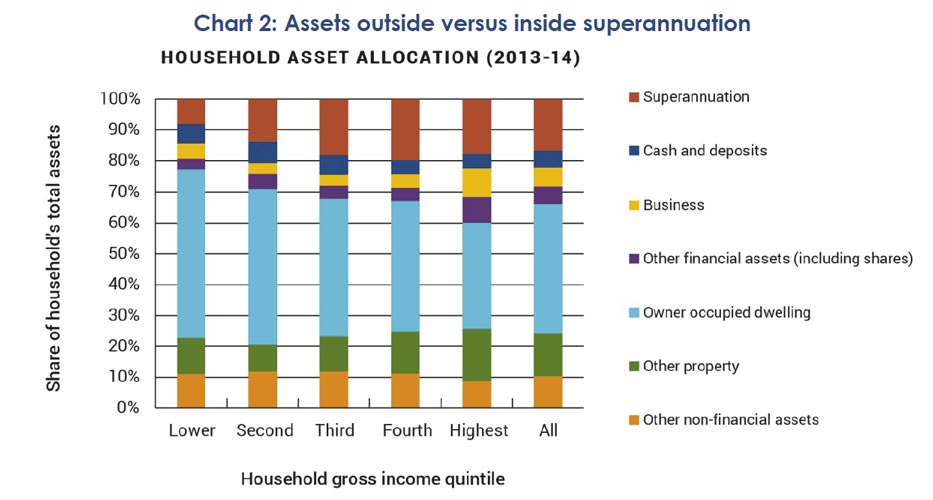

Bear in mind also that superannuation savings is a relatively small proportion of total household assets – property being the largest element (thanks to the massive rise in value), according to the ABS.

The paper says the CIPRs framework is not intended to encourage annuities over other products; compel retirees to take up a certain retirement income product; or replace the need for financial advice. We shall see.

The Government agreed to support the development of more efficient retirement income products and to facilitate trustees offering these products to members, in response to the Financial System Inquiry.

These products were labelled by the Murray Inquiry (Financial System Inquiry) as ‘Comprehensive Income Products for Retirement’, or CIPRs; however the Government proposes to use ‘MyRetirement products’ as a more consumer‑friendly and meaningful label.

The MyRetirement framework is intended to increase individuals’ standard of living in retirement, increase the range of retirement income products available, and empower trustees to provide members with an easier transition into retirement. Through this framework, the Government is aiming to increase the efficiency of the superannuation system so it can better achieve the proposed objective of superannuation, which is to provide income in retirement to substitute or supplement the Age Pension.

The Government has released, for public consultation, a discussion paper that explores the key issues in developing the framework for Comprehensive Income Products for Retirement, or MyRetirement products. Views are sought from interested stakeholders, in particular on:

the structure and minimum requirements of these products;

the framework for regulating these products; and

the offering of these products.

The Government is committed to consulting extensively with stakeholders on this framework.

A public consultation process will run from 15 December 2016 to 28 April 2017.

The discussion paper covers a lot of ground, in this complex policy area.

WHAT IS A COMPREHENSIVE INCOME PRODUCT FOR RETIREMENT (CIPR)?

It is envisaged that a CIPR would be a mass-customised, composite retirement income product (for example, combining a pooled product with a product that provides flexibility), which trustees could choose to offer to their members at retirement.

The offering of a CIPR would provide an ‘anchor’ to help guide individuals in their retirement income decision-making. Importantly, an individual would have the freedom to choose whether to take up the CIPR or take their retirement income benefits in another way.

Under the CIPRs framework although different product providers (for example, life insurance companies) could administer the underlying component products, trustees would offer a single income stream to their members.

If a trustee designs a product that: meets the proposed minimum product requirements; is in the best interests of the majority of their members; and offers the product in line with the offering requirements, it is proposed that the trustee will receive a safe harbour. The safe harbour would protect the trustee from a claim on the basis that the CIPR was not in the best interest of an individual member. This is intended to provide legal certainty for trustees in undertaking the CIPR offering.

PROPOSED STRUCTURE AND MINIMUM PRODUCT REQUIREMENTS OF A CIPR

Ensuring all CIPRs meet minimum product requirements is a key way to achieve good outcomes for consumers and to increase comparability between products.

The paper seeks feedback on possible minimum product requirements of this composite product, such as requiring a CIPR to:

deliver a minimum level of income that would generally exceed an equivalent amount invested 1.in an account-based pension drawn down at minimum rates, with recognition of the benefit of a guaranteed level of income where relevant;

deliver a stream of broadly constant real income for life, in expectation (in particular, to manage 2.longevity risk); and

include a component to provide flexibility to access a lump sum (for example, via an 3.account-based pension) and/or leave a bequest.

PROPOSED REGULATION OF CIPRS AND TRUSTEES

The paper also seeks views on how to regulate both trustees and CIPRs, in addition to regulation of the proposed minimum product requirements outlined above.

Trustees could choose to design a single mass-customised CIPR that would be in the best interests of, and offered to, the majority of their members. However, trustees would not be required to design and/or offer a product that is in the best interests of any particular member. In designing the product, trustees would need to consider whether it is in the best interests of members to outsource the administration of underlying component product(s) where the trustee does not have the necessary skill set or scale to administer the underlying component product(s).

As is currently the case, trustees and other product providers such as life insurers could also create new retirement income products that are tailored to particular member segments or individuals, rather than to the majority of the membership. These products could be offered via personal financial advice (including through robo advice) where the adviser is required to consider the individual’s circumstances and needs. Individuals could also purchase these products via direct channels. If these products are certified to meet the proposed minimum product requirements of a CIPR, it may be appropriate to allow a label to be attached indicating that the product ‘meets the minimum product requirements of a CIPR’.

WHAT THE CIPRS FRAMEWORK IS NOT ABOUT

It is important to debunk some myths about the CIPRs framework. The CIPRs framework is not intended to:

encourage annuities over other products;

compel retirees to take up a certain retirement income product; or

replace the need for financial advice.

EXAMPLES

Below are three illustrative examples of possible CIPRs: ‘the cut’, ‘the stack’, and ‘the wrap’.

For ‘The cut’ CIPR, the deferred longevity product component could represent as little as 15 to 20 per cent of an individual’s total superannuation balance and still provide a higher and more stable

income than an account-pension drawn down at minimum rates. The large account-based pension component provides a high degree of ‘flexibility’, thereby efficiently managing the concern about dying early and forfeiting an individual’s superannuation savings.superannuation savings.

‘The stack’ CIPR would provide an individual with the flexibility to access ‘lumpy’ income throughout retirement from an account-based pension component drawn down at minimum rates. Compared to ‘The cut’, a larger proportion of the individual’s total superannuation balance would go towards a longevity product component.

‘The wrap’ CIPR represents a combination of ‘The cut’ and ‘The stack’ CIPRs and in doing so, delivers a balance of their benefits. ‘The wrap’ provides longevity risk management (through the deferred longevity product), higher income than an account-based pension drawn down at minimum rates, and provides a degree of flexibility to access ‘lumpy’ income throughout retirement.

FEES AND CHARGES

Increasing the fees charged on a CIPR, post-commencement

Currently, fees for annuities and defined benefit pensions are essentially ‘locked in’ at the time of purchase due to the guaranteed level of income these products provide. However, for an account-based pension component or a group self-annuitisation component of a CIPR, there is a risk that increases in administration fees would decrease income in retirement. Individuals would not easily be able to change CIPRs in response to an increase in fees.

One option may be to restrict administrative fees from increasing over the life of a CIPR, although there is a risk that if administrative costs increased substantially accumulation members may need to cross-subsidise members in the pension phase.

Another option may be to rely on the income efficiency concept. However, given that administration fees would have a small effect on efficiency as compared with bequests and capital costs, there would need to be a large increase in fees before income efficiency is affected.

An alternative option could be to allow trustees to increase fees so long as there is no differentiation between the fees paid by existing members and new members of the CIPR. This would ensure trustees continue to face competitive fee pressure.

Trustees could lose the right to offer a CIPR to new members if they increased their fees only for existing members.

This paper also seeks alternative ideas on how to protect individuals from significant increases in fees that would erode retirement incomes.

TIMETABLE

In due course, consultation will also be undertaken on exposure draft legislation and regulations to give effect to the CIPRs framework.

It is envisaged that the CIPRs framework would not commence until trustees and other product providers have had sufficient lead-time to develop appropriate products. Given a commencement date for alternative income stream product rules of 1 July 2017, and the Government is currently reviewing the social security means testing of retirement income streams, the CIPRs framework is not expected to commence any earlier than mid-2018.

The Government could, at a later date, and following an appropriate transition period, consider whether certain trustees should be obliged to offer CIPRs to any of their members. Given this, it will be important for the current proposed CIPRs framework to be sufficiently robust to accommodate a potential change in trustee obligations down the track.

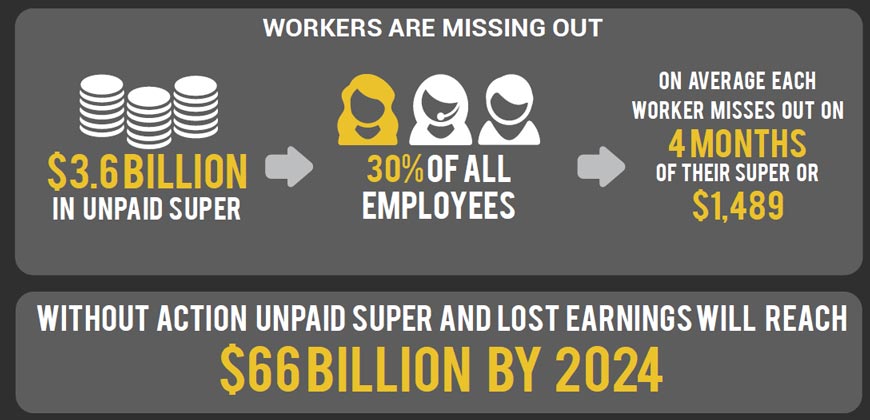

Businesses should review their obligations for compulsory superannuation contributions or potentially suffer the consequences, say experts, as a spotlight is shone on the $3.6 billion of unpaid super across the nation.

On its last sitting day on Thursday, the Senate referred the non-payment of superannuation guarantee contributions by Australian employers to the economics references committee for review in 2017. Superannuation groups have been busy modelling the scale of these non-payments, with a report from Industry Super Australia (ISA) and industry super fund Cbus released over the weekend pinning the value of unpaid super at $3.6 billion in 2013-14.

The report was completed by former Treasury official Phil Gallagher, who believes the $3.6 billion figure is “conservative”. The report highlights underpayment in the building and hospitality industries in particular, claiming the Australian Tax Office has to date been too laid back in pursuing businesses that fail to comply with the 9.5% employee super payments required by Australian law.

Over the past two years a number of studies have revealed that Australian SMEs are not focused enough on retirement planning, are sometimes tempted to put off contributing to their own superannuation and can be confused about their obligations to other staff members, particularly when employees volunteer to forgo their super. But experts warn that businesses must be vigilant in key areas of confusion, because the consequences can cost you.

Key concerns: Contractors and loopholes

The ISA report draws attention to the tendency of some businesses to incorrectly classify employees as contractors so as to avoid paying superannuation and other conditions – and that this problem increases or decreases depending on wider employment conditions.

However, David McKellar of Allied Accountants told SmartCompany that while businesses might not have to pay super contributions for a sole contractor for certain types of work, too often businesses continue to classify a worker as a contractor even after their role has come to fit the characteristics of an employee.

“In these cases, both the employer and contractor might not know there’s a liability there,” McKellar says.

The Fair Work Ombudsman directed SmartCompany towards its checklist for classifying employees and independent contractors, highlighting that contractors need to use their own equipment to complete work, work to a specific project outcome rather than on an ongoing basis, and have a high level of control over how the project is completed.

“The main thing is if the majority of the work is provided in the labor, not materials, provided by a person, then in all likelihood and most probability they will need to pay super,” senior lecturer at Deakin Business School Dr. Adrian Raftery says.

If a business owner is unsure about their responsibilities, the ATO also has a tool to calculate payments, but Raftery says some employers may be advised to pay the super guarantee to avoid facing fees for non-compliance later.

“If anything, err on the side of being conservative.”

One “loophole” the ISA report highlights as a key issue is around employees volunteering to salary sacrifice some of their wage into super. Under the current regulations, an employer is able to count this amount as part of the 9.5% that it pays into a worker’s super. However, super groups view this as contributing to further issues down the line, with many Australians already stressing over whether their retirement savings will see them through to the end of their lives.

“With access to government pensions tightening and home ownership in decline, future generations of retirees will be increasingly reliant on superannuation,” the report says.

What small businesses need to know

Small business owners have reported that they’re behind in their own retirement planning for a variety of reasons, from uncertainty over the future of the Coalition’s now-passed super changes to issues with cashflow that see them pay the business’s costs before paying themselves.

However, the costs of not upholding your obligations on super in smaller businesses can be high – even if the only person you’re not paying is yourself. While sole contractors don’t have the same requirements, the minute you operate as a business, you have to uphold your obligations, even if staff have volunteered to forgo super, says Raftery.

“Ethically, these small businesses who are struggling with super say, ‘I’ll pay all the other employees first’ and will be a bit more slack with themselves,” he says.

This is problematic because the fees that the ATO charge for late payments apply even if a business owner has chosen not to pay themselves.

“It’s essentially a penalty on each quarter that you’re late – however much super that you should be charging plus an interest rate of 10%, plus an admin fee per employee, per quarter,” says Raftery.

“The other thing that is really important is that if you get hit up with the super guarantee charge, you cannot claim that as a tax deduction.”

McKellar says for those in small family businesses, there’s only really one scenario where super contributions don’t need to be paid.

“The only way around it would be perhaps if someone is working for no payment,” he says.

Other than that, you must pay up. And while business owners might feel stress in the short term, when it comes to their own retirement planning, paying themselves is the best choice for tax planning, says Raftery.

“There’s a legal obligation and if you don’t pay your own and the ATO does its investigation, they won’t treat you any differently than a independent employee,” he says.

“But for their tax incentives it’s to their advantage to pay into super – otherwise they’re just being taxed at the corporate tax rate.”

The inquiry into superannuation payments will look at the accuracy of data collected by regulatory bodies around the value of payments made, as well as the ATO’s approach to compliance.

Pillar Administration, a Wollongong-based company with over $100 billion in funds under administration, has been acquired by Mercer.

The NSW government announced it would be putting Pillar up for sale in December 2015 as part of its ‘asset recycling’ program.

Link Group was initially a frontrunner to acquire the business, but its hopes were dented when the ACCC raised objections to the acquisition in October 2016.

In a statement Mercer said the acquisition would make it the largest provider of outsourced superannuation administration services in Australia.

Mercer’s managing director Ben Walsh said: “We will add further value to our clients and to members through the investments we are making in our business and through strategic partnerships, alliances and acquisitions such as this one.”

“Specifically, we know many super funds are seeking a proactive and sustainable business partner who can provide superior administration and related services, reduce costs and help funds get closer to members.

“For this reason we have invested heavily in our people capability, process innovation and technologies to ensure we are ready for these opportunities. This deal provides Mercer with the capability and scale to enhance our clients’ relationships with their members,” Mr Walsh said.

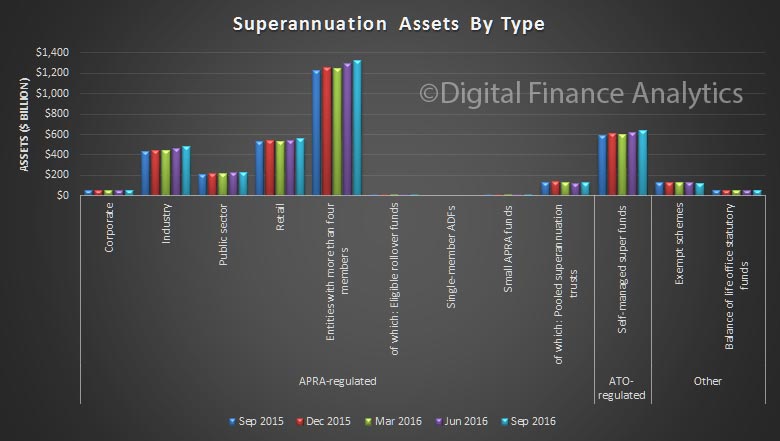

APRA has released the latest superannuation statistics to September 2016. Total superannuation assets are worth $2,145.6 billion up +7.4% in the past year. Of this, $1,330.5 billion are in entities regulated by APRA, up 8.7% in the past year.

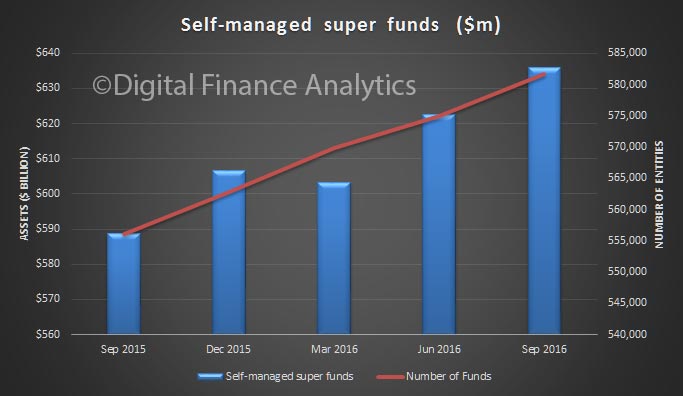

Self managed superannuation balances reached $635.9 billion, up +8.0% in the past year.

Total assets in MySuper products totalled $492.2 billion at the end of the September 2016 quarter. Over the 12 months from September 2015 there was a 13.6 per cent increase in total assets in MySuper products, and a 23.7 per cent decrease in total assets in accrued default amounts to $39.6 billion.

There were $23.2 billion of contributions in the September 2016 quarter, down 4.7 per cent from the September 2015 quarter ($24.4 billion). Total contributions for the year ending September 2016 were $103.1 billion. Outward benefit transfers exceeded inward benefit transfers by $1.0 billion in the September 2016 quarter.

There were $17.0 billion in total benefit payments in the September 2016 quarter, an increase of 6.6 per cent from the September 2015 quarter ($15.9 billion). Total benefit payments for the year ending September 2016 were $65.7 billion. Lump sum benefit payments ($8.3 billion) were 49.1 per cent and pension benefit payments ($8.6 billion) were 50.9 per cent of total benefit payments in the September 2016 quarter. For the year ending September 2016, lump sum benefit payments ($33.0 billion) were 50.2 per cent and pension payments ($32.7 billion) were 49.8 per cent of total benefit payments.

Net contribution flows (contributions plus net benefit transfers less benefit payments) totalled $5.3 billion in the September 2016 quarter, a decrease of 30.4 per cent from the September 2015 quarter ($7.6 billion). Net contribution flows for the year ending September 2016 were $31.7 billion.

The Gratton Institute says compulsory superannuation payments help many middle-income earners to save more for retirement, but super is simply the wrong tool to provide an adequate support for low-income earners. Their analysis shows top-up measures targeted at helping this group save for retirement are poorly targeted and an expensive way to do so.

Australia’s superannuation lobby wants the government to define in law that the purpose of Australia’s A$2 trillion super system is to provide an adequate retirement income for all Australians. The government disagrees: it confirmed instead that the purpose of super is to supplement or substitute for the Age Pension.

The government is right: super can’t do everything. Income from the superannuation of low-income earners will inevitably be small relative to the value of the Age Pension. The government boost to super aimed at low income earners is not tightly targeted. And fees will eat up a material portion of government support provided through superannuation.

With the Age Pension and Rent Assistance, government already has the right tools for assisting lower income Australians.

Government provides two super top-ups for low income earners

The Low Income Superannuation Contribution (LISC), introduced by the Labor government in 2013, puts extra money in the accounts of low-income earners who make pre-tax super contributions. Under the LISC, those earning less than A$37,000 receive a government co-contribution of 15% of their pre-tax super contributions, up to a maximum of A$500 a year.

The Abbott government was set to abolish the LISC, but the Turnbull government now plans to retain it, renaming it the Low Income Superannuation Tax Offset (LISTO), at a budgetary cost of A$800 million a year.

The super co-contribution, introduced by the former Howard government in 2003, puts extra money in the accounts of low-incomes earners who make post-tax super contributions. It boosts voluntary super contributions made by low-income earners out of their post-tax income by up to A$500 a year, at a budgetary cost of A$160 million a year.

Super can’t help many low income earners

Superannuation is a contributory system: you only get out what you put in. And low-income earners don’t put much in.

Their wages, and resulting super guarantee contributions, are small and their means to make large voluntary contributions are even smaller. Their super nest egg will inevitably be small compared to Australia’s relatively generous Age Pension.

For example, a person who works full time at the minimum wage for their entire working life and contributes 9.5% of their income to super would accumulate super of about A$153,000 in today’s money (wage deflated), making standard assumptions about returns and fees. If the balance were drawn down at the minimum rates, this would provide a retirement income of about A$6,500 a year in today’s money.

By contrast, an Age Pension provides a single person with A$22,800 a year. For someone who worked part time on the minimum wage for some or all of their working life, super would be even less, but the Age Pension would be pretty much the same.

Top-ups are not tightly targeted to those that need them

The LISC and the super co-contribution aim to top up the super and thus the retirement incomes of those with low incomes. But our research shows about a quarter of the government’s support leaks out to support the top half of households.

Whereas eligibility for the pension is based on the income and assets of the whole household, including those of a spouse, eligibility for superannuation top ups depends only on the income of the individual making contributions. That means the top ups also benefit low-income earners in high-income households. A far better way to help low-income earners is to increase income support payments such as the Age Pension.

Super top ups provide some help to households in the second to fourth deciles of taxpayers. But they do very little for the bottom 10% of those who file a tax return.

These households, many of which earn little if any income, only receive about 7% of the benefits of top ups. A further set of households file no tax returns – typically because welfare benefits provide most of their income. Very few of them receive any material super top up.

Super fees erode super top ups

Super fees will erode a sizeable share of the funds in the super accounts of low-income households, as a result of super top ups. Our research shows that super fees levied on most workers receiving the LISC erode between 20 and 25% of the value of the extra funds at retirement. This finding is consistent with previous Grattan work on super fees.

But super fees do not usually erode super top ups as much as they erode contributions to super in general. Fees eat up a higher proportion of the super savings of people with low balances because most fees have a fixed component that’s the same whatever the account balance. In effect the personal super contributions of low-income earners absorb that fixed component, which is typically the same whether or not government tops up the account.

However for those with very low super savings and sporadic employment, fixed fees can erode the value of their super top ups. That’s because at some point in their lives, their super balances can drop close enough to zero and fixed administration fees eat into the value generated by the top up.

Many Australians face low incomes and irregular work. They may not be able to contribute enough to their super to make up for fixed fees.Lucy Nicholson/Reuters

Some top up is still needed for low income earners

Superannuation compels people to lock up some of their earnings as savings until retirement. High-income earners are compensated for this delayed access because their contributions are only taxed at 15%, rather than their marginal rate of personal income tax.

Without the LISC, which reduces the tax rate on their compulsory super contributions to zero, those earning between A$20,542 and A$37,000 would receive relatively little compensation for locking up their money in superannuation. The 15% tax on contributions would be only slightly less than their 19% marginal tax rate.

And for those earning less than A$20,542, the absence of a LISC would take them backwards when they made super contributions taxed at 15% rather than keeping the money in their pocket tax free.

Better ways to provide adequate retirement incomes for low-income earners

However super top ups should not be expanded. It is too hard to target them tightly at those most in need, and super fees can eat up their value.

Instead, a targeted boost to the Age Pension would do far more to ensure all Australians have an adequate retirement. But there is an even better way to improve the retirement incomes of those most in need.

As previous Grattan research shows, retirees who do not own their own homes are the group at most risk of being poor in retirement. A A$500 a year boost to rent assistance for eligible seniors would be the most efficient way to boost retirement incomes of the lowest paid, at a cost of A$200 million a year. Only 2% of it would flow to the top half of households, with net wealth of more than A$500,000.

By contrast, a wholesale A$500 boost to all Age Pension recipients would cost A$1.3 billion, with half the benefit going to households with net wealth of more than A$500,000, mainly because the home is exempt from the Age Pension means test.

In defining an objective for Australia’s superannuation system, the government is right that super is not a universal pocket knife. Super top ups are a costly way to ensure that every Australian enjoys an adequate retirement.

Authors: John Daley, Chief Executive Officer, Grattan Institute; Brendan Coates, Fellow, Grattan Institute; William Young, Associate, Grattan Institute

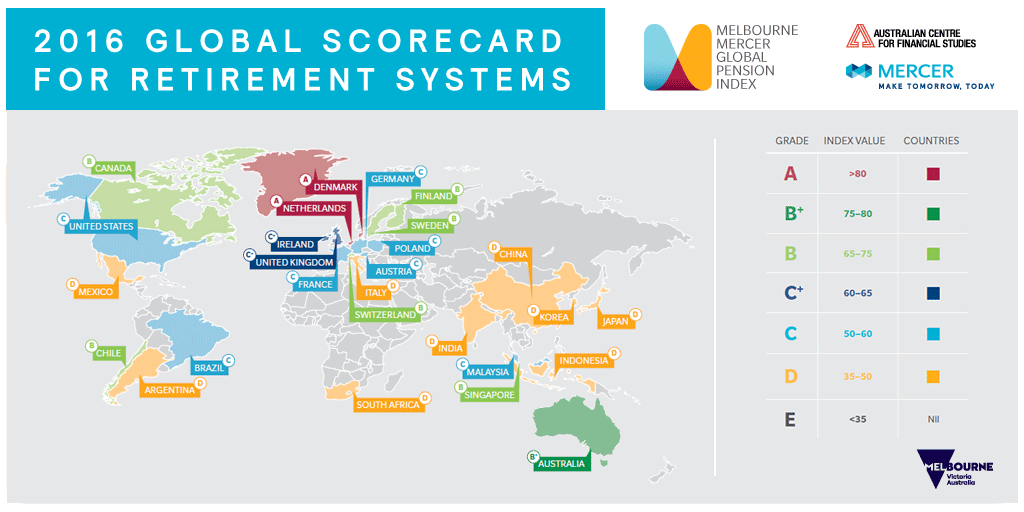

Despite retaining its third-place ranking behind Denmark and Netherlands in the 2016 Melbourne Mercer Global Pension Index (MMGPI), Australia has sustained a slight drop in the rating of its pension system for the second consecutive year.

Whilst not alarming, narrowly missing out on the Index’s A-grade ranking by receiving a score between 75 and 80 for a sixth consecutive year indicates that despite being superior in many ways, further reform is required to ensure that Australia’s retirement system is considered world class, as is the case for Denmark’s and Netherlands’, which both retained their A-grade rankings.

Measures that were suggested to improve Australia’s system include:

Introducing a requirement for an income stream to comprise part of the retirement benefit;pension age relative to ongoing increases in life expectancy;

Increasing the preservation age;

Continuing to increase labour participation rate at older ages.

Australia’s overall Index Value saw a decline from last year’s 79.6 to this year’s 77.9. Author of the report and Senior Partner at Mercer, Dr. David Knox, attributed this to a “reduction in the net replacement rate”, caused by the federal government’s decision last year to defer the increase of the Superannuation Guarantee from its current 9.5 per cent to the proposed 12.

Despite its deferral affecting this year’s Australian adequacy rating, former Commonwealth Bank CEO and most recent Chairman of the Financial System Inquiry (FSI) Dr. David Murray AO insisted in his interview with Franklin Templeton Managing Director Ms. Maria Wilton, that an increased superannuation guarantee was necessary for a sufficient adequacy, given the tightening of the taxation arrangements around superannuation by the Federal Government.

“The nominal contribution rate [of the current superannuation guarantee] is 9.5 per cent. In effect, this is closer to 8 on an after-tax basis, and in adequacy terms” he believed this was insufficient. “You would have to get at least 11 after tax… on a pre-tax basis, allowing for the contributions tax, that’s around 14-15%”, Dr. Murray explained.

More alarmingly perhaps, Dr. Knox hinted at the fact that Australia’s score could undergo a further decline in future years, due to the Index not yet having taken into consideration the tougher 2017 Age Pension assets test, which will see a reduction in pension payments.

“At the moment, there is no allowance for the new assets test that comes on January 1 next year. I’m expecting our net replacement rate… to fall again”, Dr. Knox stated.

Despite these issues, Dr. Knox confirmed that the positives associated with the Australian pension system far outweighed the negatives, noting that a significant factor in Asian countries such as India, Singapore and Korea being the biggest improvers in the 2016 index ratings, was these countries considering the Australian system an archetypal source of recommendations.

These sentiments were endorsed by Dr. Murray, who deduced that “in a low growth world, with unfunded systems from much of the developed world” a country taking Australia’s third rank was “more likely to come from Asia” than anywhere else.

This year, 27 countries were included in the MMGPI, all of which obtained an index value based on more than 40 indicators, each belonging to one of three sub-indices; adequacy, sustainability and integrity. Covering almost 60% of the global population, one of its primary aims is to highlight the shortcomings in each country’s retirement income system, and suggest possible areas of reform.

THE VERY SIGNIFICANT IMPACT OF AGEING POPULATIONS ON GLOBAL PENSIONS

As well as dealing with annual rankings, this year’s edition of the MMGPI closely inspected the impact of an ageing global population, and how well equipped each country in the Index is to deal with this issue.

It was found that each country has experienced improvements, albeit to varying extents, in life expectancy over the last four decades. As outlined by Dr. Knox, when these projected increases in life expectancies are combined with recent marked decreases in fertility rates, the result is that “many countries are facing a significant [old] age dependency ratio over the next 25 years”.

“[In] 1980, we had almost 6 workers per older person, a couple of years ago, we had 4.7 and by 2040, we will have 2.3”.

It was found that of the countries in the Index, the one best placed to tackle this issue of an ageing population was Indonesia, due to the combined effects of its relatively low projected old age dependency ratio in 2040, and its preferable scoring on a range of mitigating factors, which it was explained by Dr. Knox, were very likely to offset the inevitability of having more aged.

These mitigating factors include:

Labour force participation rate for 55-64

Labour force participation rate for 65+

Amount of increase in the labour force participation rate for 55-64

Projected increase in the retirement period over the following 2 decades;

Pension fund assets as a % of GDP.

Professor Rodney Maddock, Interim Executive Director of the Australian Centre for Financial Studies, who hosted the Index’s official launch, echoed Dr. Knox’s thoughts, noting that an adjustment to both the retirement and pension eligibility age was necessary to ensure the continuing sustainability of Australia’s superannuation system: “Australians are living longer, living larger portions of their life in retirement and spending more in retirement, so we need to be well-placed to ensure fulfilling, adequately-funded retirements.”

From a more global perspective, perhaps in a much more dire state, is a nation such as Japan, which according to Dr. Knox, will have “one retiree for every 1.44 people of working age by 2040”, demonstrating the “alarming” projected old age dependency ratios in some nations.

ASIC has released Report 499 Financial advice: Fees for no service (REP 499). They say to date, approximately $23.7 million of fee refunds and compensation has been paid, or agreed to be paid, to over 27,000 customers of ANZ, NAB, CBA, Westpac and AMP. But further reviews are being conducted and based on estimates, compensation may increase by approximately $154 million, plus interest, to over 175,000 further customers, meaning that total compensation for related failures could be over $178 million, plus interest.

The report provides an update on ASIC’s work to address financial institutions’ and advisers’ systemic failures, over a number of years, to provide ongoing advice services to customers who paid fees to receive those services. The report summarises ASIC’s work to ensure customers are fairly compensated. The report is part of ASIC’s Wealth Management Project which is focusing on the conduct of the largest financial advice firms, including the advice arms of AMP, ANZ, CBA, NAB and Westpac groups (refer: 15-081MR).

The failures set out in the report relate to instances where customers were charged a fee to receive an ongoing advice services, but had not been provided with this service because:

The customer did not have an adviser allocated to them, but was charged a fee for ongoing advice – usually by deduction from the customer’s investment products; or

The adviser allocated to the customer failed to deliver on their obligation to provide the ongoing advice service and the licensee failed to ensure that the service was provided.

To date, approximately $23.7 million of fee refunds and compensation has been paid, or agreed to be paid, to over 27,000 customers of ANZ, NAB, CBA, Westpac and AMP under various Australian Financial Services (AFS) licensees that are owned by these businesses. Further reviews are being conducted by the licensees to determine the extent of their ongoing service fee failures. Refunds and compensation are expected to increase substantially as the licensees’ investigations and reviews continue. Based on estimates provided by the licensees to ASIC, compensation may increase by approximately $154 million, plus interest, to over 175,000 further customers, meaning that total compensation for related failures could be over $178 million, plus interest.

ASIC has commenced several enforcement investigations in relation to this conduct.

Most of the failures outlined in this report occurred before the commencement of the Future of Financial Advice (FOFA) reforms. The changes made by those reforms were a significant factor in the identification of the failures, and also substantially reduce the likelihood that the type of systemic failures described in this report will occur in the future. In particular, the requirement to now provide an annual Fee Disclosure Statement to the client, and the requirement for the client to ‘opt-in’ to the advice relationship every two years, will significantly reduce the risk of fees being charged without any advice service provided.

‘Changes introduced through the FOFA reforms have shone a light on the advice fees that customers are paying and the services they should be receiving in return,’ said ASIC Deputy Chair Peter Kell. ‘Our report identifies the institutions’ systemic failures in this area, which we are putting right by ensuring that customers are fairly compensated.’

ASIC’s MoneySmart website has updated information on how much financial advice costs and what to expect from a financial adviser. Customers should check they are receiving the services they are paying for. Customers who are paying ongoing advice fees for services they do not need can ask for those fees to be switched off. Customers who have paid fees for services they did not receive may be entitled to refunds and compensation, and should lodge a complaint through the bank or licensee’s internal dispute resolution system or the Financial Ombudsman Service.