The Government has released for public consultation draft legislation and associated explanatory materials for changes to improve the integrity of the superannuation system. These changes are being progressed as part of a package of amendments to address concerns that have been raised in the implementation of the superannuation reform tax package.

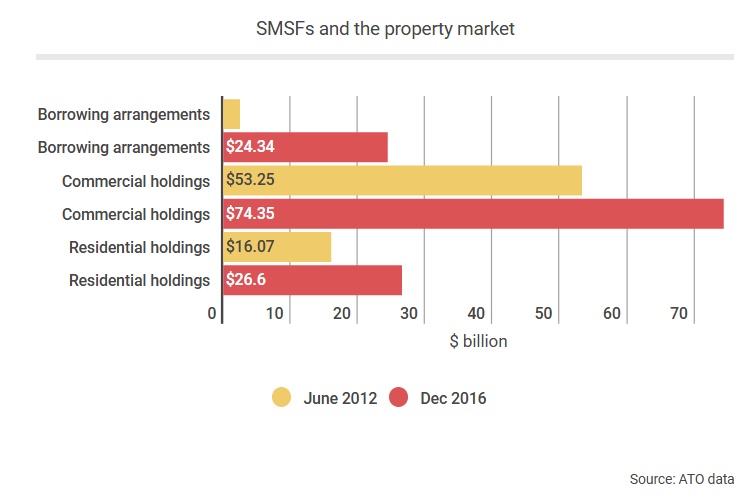

The draft legislation will include the use of limited recourse borrowing arrangements (LRBA) in a member’s total superannuation balance and transfer balance cap to the transfer balance cap and total superannuation balance. The amendments will address concerns about the ability of SMSF members to use LRBAs to circumvent contribution caps and effectively transfer accumulation growth to retirement phase that is not captured by the transfer balance cap.All interested parties are invited to make a submission by Wednesday 3 May 2017. More information on the Government’s superannuation changes is available on the Treasury website.

The two worked examples make things a little clearer, but in essence it attempts to stop SMSF property investment being used to circumvent the $1.6m tax free cap.

Example 1

Bob is 65 and is the only member of his SMSF. Bob’s superannuation interests are valued at $3 million and are based on cash that the SMSF holds.

Bob’s SMSF acquires a $2 million property. This property is purchased after 1 July 2017 using $500,000 of the SMSF’s cash and an additional $1.5 million that it borrows through an LRBA.

Bob then commences an account-based superannuation income stream. The superannuation interest that supports this superannuation income stream is backed by the property, the net value of which is $500,000 (being $2 million less the $1.5 million liability under the LRBA). Bob therefore receives a transfer balance credit of $500,000 under item 2 of the table in subsection 294-25(1).

In the first year, Bob’s SMSF makes monthly repayments of $10,000. Half of each repayment is made using the rental income generated from the property. The other half of each repayment is made using cash that supports Bob’s other accumulation interests.

At the time of each repayment, Bob receives a transfer balance credit of $5,000, representing the increase in value of the superannuation interest that supports his superannuation income stream.

The repayments that are sourced from the rental income that the SMSF receives do not give rise to a transfer balance credit because they do not result in a net increase in the value of the superannuation interest that support his superannuation income stream.

Example 2

Peter and Sue are the only members of their SMSF. The value of Peter’s superannuation interests in the fund is $1 million. The value of Sue’s superannuation interests is $2 million. All of the assets of the fund that support their interests are cash.

The SMSF acquires a $3.5 million property. The SMSF purchases the property using $1.5 million of its own cash and borrows an additional $2 million using an LRBA.

The SMSF now holds assets worth $5 million (being the sum of the $1.5 million in cash and the $3.5 million property). The fund also has a liability of $2 million under the LRBA.

Of its own cash that it used, 40 per cent ($600,000) was supporting Peter’s superannuation interests and the other 60 per cent ($900,000) was supporting Sue’s interests. These percentages also reflect the extent to which the asset supports Peter and Sue’s superannuation interests.

Peter’s total superannuation balance is $1.8 million. This is comprised of the $400,000 of cash that still supports his superannuation interest, the 40 per cent share of the net value of the property (being $600,000), and the 40 per cent share of the outstanding balance of the LRBA (being $800,000).

Sue’s total superannuation balance is $3.2 million. This is comprised of the $1.1 million of cash that still supports her superannuation interest, the 60 per cent share of the net value of the property (being $900,000), and the 60 per cent share of the outstanding balance of the LRBA (being $1.2 million).