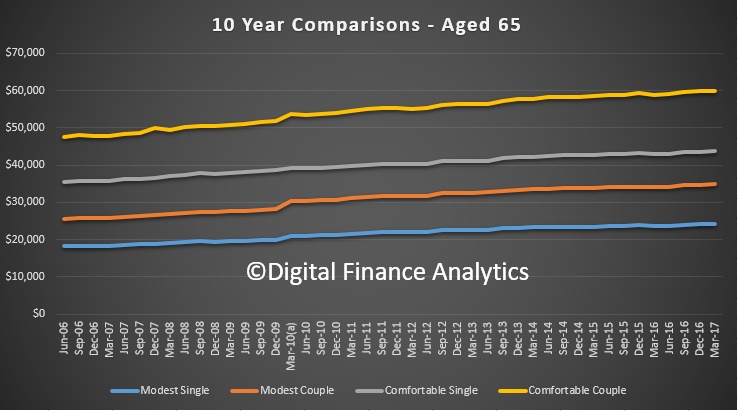

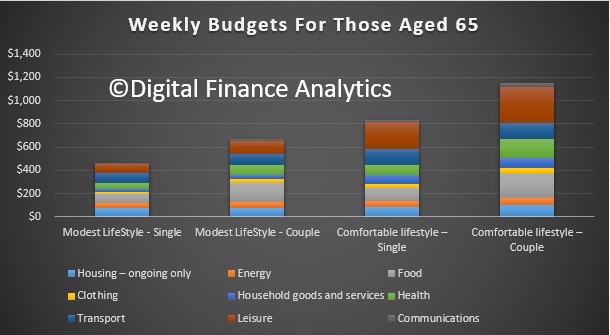

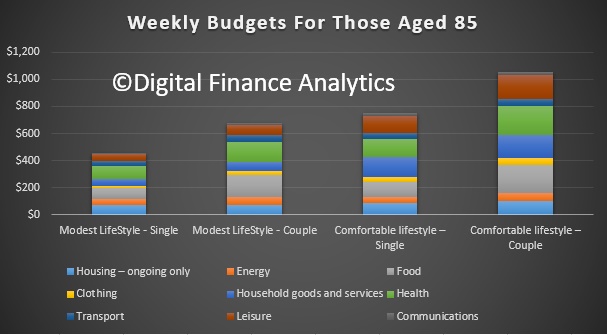

Rising costs of living are impacting retired households according to new research. The figures reveal couples aged around 65 will need to spend $59,971 a year and singles $43,665.

Significant hikes in the cost of power, health care, food and rates over the past 10 years have driven increases in the amounts needed to achieve both modest and comfortable retirements, according to the latest data from the Association of Superannuation Funds of Australia (ASFA).

It is more than a decade since the first release of the modest and comfortable ASFA Retirement Standard (RS) budgets.

Every three months since June 2006, they have tracked the rise and fall of items that comprise average household budgets. Updates reflect inflation and provide detailed budgets of what singles and couples need to support their chosen lifestyle.

Between June 2006 and March 2017, the RS budget at the modest level for a single person increased by 33 per cent, while the single comfortable budget rose by 23 per cent.

The budget for a couple at the modest level increased by 36 per cent and at the comfortable level by around 26 per cent.

ASFA CEO Dr Martin Fahy said the figures compared to an overall 28.6 per cent increase in the Consumer Price Index (CPI).

“The categories of expenditure that really impacted the budgets are not altogether surprising,” he said.

“Over the period, electricity costs increased by 124 per cent, health costs by 60 per cent, property rates and charges by 83 per cent and food costs by 24 per cent.

“Price changes for less essential items tended to be lower and in some cases prices fell.

“The price of clothing fell by a total of three per cent over the period with an eight per cent fall in the cost of communications (including telephone and mobile phone charges).

“The cost of international holidays rose by a relatively modest 16 per cent over the period.”

Over the more than 10 year period, the maximum Age Pension increased in real terms, by 70 per cent for a single person and 54 per cent for a couple, from a starting base far too close to the poverty level.

The Age Pension is adjusted by what is the greater of the increase in average wages or the CPI. During the period, average earnings rose by 43 per cent.

There also were some discretionary increases made to the rate of the Age Pension, particularly to the single rate. However, despite these various increases, the Age Pension alone still does not permit a retiree to achieve even a modest standard of living in retirement at the levels set by the ASFA RS.

The increases in the Age Pension over and above the increase in the CPI and in wages have helped contain the savings required at the time of retirement, in order to support either a modest or comfortable lifestyle.

On the other hand, the tightening of the means test has led to an increase in the amount of retirement savings needed to support a comfortable standard of living in retirement.

Other price increases of interest included: tobacco (not in RS budgets but consumed by many retirees) up by 178 per cent; wine up by only six per cent, but beer up 45 per cent; rents up 51 per cent; postal services up 45 per cent; vet fees (not in RS budgets) up 49 per cent; and, insurance costs up 72 per cent.

Dr Fahy said both budgets assume retirees own their own home outright and are relatively healthy.

“Of increasing concern is the reality of many more retirees at the mercy of the private rental market, so when you consider the increase in renting costs, it highlights the need for increasing numbers of retirees to have much greater super balances to support a reasonable retirement,” he said.

In the latest RS updates for the March quarter, there was a slight increase in the cost of living for retirees, with increases in the prices of petrol, medical and hospital services and electricity.

The ASFA RS March quarter figures indicate couples aged around 65 living a comfortable retirement need to spend $59,971 per year and singles $43,665, both up 0.3 per cent on the previous quarter.

Total budgets for older retirees increased by around 0.3 per cent at the comfortable level and 0.6 per cent at the modest level.

Over the year to the March quarter, there was a 1.8 per cent increase in the budgets, slightly lower than the 2.1 per cent increase in the All Groups CPI.

Dr Fahy said the cost of retirement over the most recent quarter only increased by a relatively small amount but many individuals would still find it difficult to achieve a comfortable standard of living in retirement.

“Over the longer term, the cumulative increase in retirement costs has been considerable,” he said.

The most significant price increases in the March quarter contributing to the increases in annual budgets were for automotive fuel (5.7 per cent), medical and hospital services (1.6 per cent) and electricity (2.5 per cent). Fluctuations in world oil prices continue to influence domestic fuel prices.

The most significant offsetting price falls were for international holiday travel and accommodation (-3.8 per cent) and fruit (-6.7 per cent).

Overall, food prices fell 0.2 per cent in the March quarter. The main contributor to the fall was fruit (-6.7 per cent), due to plentiful supplies of both year-round and summer fruit. Over the last 12 months, food prices rose by 1.8 per cent.

International holiday travel and accommodation prices fell 3.8 per cent due to the winter off-peak seasons in Europe and America.

Clothing and footwear prices fell 1.4 per cent in the quarter, reflecting discounting during the post-Christmas sales.

The price rises for both medical and hospital services and pharmaceutical products reflect the annual cycles for the Medicare Benefits Scheme and Pharmaceutical Benefits Scheme (PBS).

Insurance prices increased 0.8 per cent in the quarter. Over the last 12 months, insurance prices have increased by 6.8 per cent.

Expenditure on education is not included in the retirement budgets but some retirees paying school fees for their grandchildren would be affected by a 4.1 per cent increase in secondary education school fees following the commencement of the new school year.