The UK are outlawing Insurance renewal price walking (which relies of loyal customers paying more than new customers on renewal. In Australia things remain muddy at best, and people can save significantly by being proactive – yet most just roll over!

Go to the Walk The World Universe at https://walktheworld.com.au/

We look at data from our household surveys in the light of a recent The Conversation article. Many households are underinsured, and may be caught out in a crisis.

Australia is in the midst of a bushfire crisis that will affect local communities for years, if not permanently, due to a national crisis of underinsurance. Via The Conversation.

Already more than 1,500 homes have been

destroyed – with months still to go in the bushfire season. Compare this

to 2009, when Victoria’s “Black Saturday” fires claimed more than 2,000

homes in February, or 1983, when the “Ash Wednesday” fires destroyed

about 2,400 homes in Victoria and South Australia, also in February.

The 2020 fire season could end up surpassing these tragedies, despite the lessons learned and improvements in preparedness.

One lesson not really learned, though, is

that home insurance is rarely sufficient to enable recovery. The

evidence is many people losing their homes will find themselves unable

to rebuild, due to lack of insurance.

Research published by the Victorian government in 2017, meanwhile, estimated just 46% Victorian households have enough insurance to recover from a disaster, with 28%

underinsured and 26% having no insurance.

The consequences aren’t just personal.

They potentially harm local communities permanently, as those unable to

rebuild move away. Communities lose the vital knowledge and social

networks that make them resilient to disaster.

Miscalculating rebuilding costs

All too often the disaster of having your

home and possessions razed by fire is followed by the disaster of

realising by how much you are underinsured.

As researchers into the impact of fires,

we are interested why people find themselves underinsured. Our research,

which includes interviewing those who have have lost their homes, shows it is complicated, and not necessarily due to negligence.

For example, a woman who lost her home in

Kinglake, northeast of Melbourne, in the 2009 fires, told us how her

insurance calculations turned out to bear no resemblance to the actual

cost of rebuilding.

“You think okay, this is what I paid for

the property,” she said. “I think we had about $550,000 on the house,

and the contents was maybe $120,000.” It was on these estimates that she

and her partner took out insurance. She told us:

You think sure, yeah, I can rebuild my

life with that much money. But nowhere near. Not even close. We wound up

with a $700,000 mortgage at the end of rebuilding.

An extra mortgage

A common issue is that people insure based on their home’s market value. But rebuilding is often more expensive.

For one thing there’s the need to comply

with new building codes, which have been improved to ensure buildings

take into account their potential exposure to bushfire. This is likely

to increase costs by 20% or more, but is rarely made clear to insurance customers.

Construction costs also often spike following disasters, due to extra demand for building services and materials.

A further contributing factor is that

banks can claim insurance payments to pay off mortgages, meaning the

only way to rebuild is by taking out another mortgage.

“People who owned houses, any money that

was owing, everything was taken back to the bank before they could do

anything else,” said a former shop owner from Whittlesea, (about 30km

west of Kinglake and also severely hit by the 2009 fires).

This meant, once banks were paid, people had nothing left to restart.

She told us:

People came into the shop and cried on my

shoulder, and I cried with them. I helped them all I could there. That’s

probably why we lost the business, because how can you ask people to

pay when they’ve got nothing?

Undermining social cohesion

In rural areas there is often a shortage

of rental properties. Insurance companies generally only cover rent for

12 months, which is not enough time to rebuild. For families forced to

relocate, moving back can feel disruptive to their recovery.

Underinsurance significantly increases the

chances those who lose their homes will move away and never return –

hampering social recovery and resilience. Residents that cannot afford

to rebuild will sell their property, with “tree changers” the most

likely buyers.

Communities not only lose residents with local knowledge and important skills but also social cohesion. Research in both Australia and the United States suggested this can leave those communities less prepared for future disasters.

This is because a sense of community is

vital to individuals’ willingness and ability to prepare for and act in a

threat situation. A confidence that others will weigh in to help in

turn increases people’s confidence and ability to prepare and act.

In Whittlesea, for example, residents

reported a change in their sense of community cohesion after the Black

Saturday fires. “The newer people coming in,” one interviewee told us,

“aren’t invested like the older people are in the community.”

Australia is one of the few wealthy

countries that heavily relies on insurance markets for recovery from

disasters. But the evidence suggests this is an increasingly fraught

strategy, particularly when rural communities also have to cope with the

reality of more intense and frequent extreme weather events.

If communities are to recover from bushfires, the nation cannot put its trust in individual insurance policies. What’s required is national policy reform to ensure effective disaster preparedness and recovery for all.

Authors: Chloe Lucas, Postdoctoral Research Fellow, Geography and Spatial Sciences, University of Tasmania; Christine Eriksen, Senior Lecturer in Geography and Sustainable Communities, University of Wollongong; David Bowman, Professor of Pyrogeography and Fire Science, University of Tasmania

The Reserve Bank of New Zealand (RBNZ) and Financial Markets

Authority (FMA) today released their findings on life insurers’ responses to

the joint Conduct and Culture Review.

Overall, the regulators were

disappointed by the responses. Significant work is still needed to address the

issues of weak governance and ineffective management of conduct risk,

identified in the regulators’ report earlier this year.

Rob Everett, FMA Chief

Executive, said: “While we’re disappointed, we’re not surprised as the

responses confirm what we found in our original review. It’s clear that

progress has been slow and not as far-reaching as required.

Some providers have started

work to identify the customer and conduct issues they face, others have not

provided any detail on this.”

Sixteen life insurers were

asked to provide work plans outlining the steps they will take to improve their

existing processes and address the regulators’ findings and recommendations.

There was wide variance in

the comprehensiveness and maturity of the plans provided.

Adrian Orr, Reserve Bank

Governor, said, “We’re disappointed the industry’s response has been

underwhelming. The sector has failed to demonstrate the necessary urgency and

prioritisation, around investment in systems, to provide effective governance

and monitoring of conduct risk.”

There was also a wide

variance in the quality and depth of the systematic review of policyholders and

products. Some did not complete this exercise and others did not provide data

on the number of policyholders affected or the estimated cost of remediation

activities. Insurers that completed the exercise identified at least 75,000

customer issues requiring remediation, with a value of at least $1.4 million.

Some of the new issues identified included:

Overcharging of premiums and benefits not being updated due to system errors, human errors and under-reporting of deaths

Poor customer conversations overlooking eligibility criteria and poor post-sale communications, which lead to declined claims and underpayment of benefits

Poor value products were identified, where premiums charged were not fair value for the cover provided.

Sales incentives and

commissions

The FMA and RBNZ committed

to report back on staff incentives and commissions for intermediaries. Previous

reports by the FMA reflected the concerns with conflicted conduct associated

with high up-front commissions and other forms of incentives, (like overseas

trips) paid to advisers.

Although some insurers have

committed to removing sales incentives for employees and their managers, not

all committed to removing or altering indirect sales incentives.

Those providers that have

removed sales incentives for employees don’t typically use external advisers to

distribute products. Providers using external advisers told the regulators that

changing long-held business arrangements and distribution models is difficult

and will take time to implement.

Mr Everett said, “We’re

ready to work with life insurers to ensure they prioritise their focus on

serving the needs of their customers, while at the same time balancing the need

to remunerate advisers for the important work they do to help these customers.

But we do not think high up-front commissions create confidence that insurers

and advisers are acting in the best interests of customers.”

Mr Orr said, “Good

governance within insurance firms requires the effective management of conflicts

of interest. We need to see much better systems and controls in place to manage

the inherent conflicts where advisers or sales staff are offered incentives to

sell or replace insurance policies.”

Next steps

Those companies that have

not undertaken comprehensive systematic reviews of policyholders and products

have been asked to complete further reviews of their systems to identify

issues, and to develop mature plans to respond and remediate any of their

findings. These plans must be completed by December 2019.

The FMA and RBNZ will

continue to monitor how the insurers are responding to recommendations and

implementing their work plans. Life insurers are currently not legally required

to become more customer-focused and the FMA and RBNZ found that the sector has

a weak appetite for change.

Deficiencies in some of the

plans received, and some insurers’ lack of commitment to implementing the

regulators’ recommendations, further demonstrates the need for additional

obligations to be included in the regulation of conduct of life insurers.

ASIC says that Allianz Australia Insurance Limited (Allianz) will refund over $8 million in consumer credit insurance (CCI) premiums and fees including interest to more than 15,000 consumers.

This follows ASIC’s review of the sale of CCI by lenders in Report 622 Consumer credit insurance: Poor value products and harmful sales practices (REP 622), and forms part of ASIC’s broader priority to address harms and unfair practices impacting consumers in insurance.

Allianz’s refund relates to the sale of cover to

consumers who were ineligible to make a claim for unemployment or

disability, the sale of death cover to customers under 21 years of age

who were unlikely to need that cover, and the charging of fees to

customers who paid premiums by the month without adequate disclosure.

The remediation program covers certain CCI products

issued by Allianz including mortgage and loan protection policies sold

through financial institutions. These CCI products provided cover

against the risk of consumers being unable to meet loan commitments

because of death, injury, illness or involuntary unemployment.

To address these issues, Allianz will,

for ineligible sales of unemployment and disability cover,

refund premiums charged plus interest for active, cancelled or lapsed policies sold between 1 January 2011 to 31 December 2018;

reassess all withdrawn and declined claims where the consumer was ineligible for the policy at the time of sale;

invite consumers to submit a claim if they have not already done so and pay valid claims plus interest; and

continue to honour active policies and not rely on employment eligibility criteria as a basis to decline an unemployment or disability claim;

for sales of death cover to customers under 21 years of age,

refund all premiums charged plus interest for active, cancelled or lapsed policies sold between 1 January 2011 to 31 December 2018; and

preserve existing death cover for active policyholders on current terms without charging for it;

for monthly policy payment customers,

refund all administration fees and loading charged plus interest; and

correct any future direct debit amounts.

ASIC Commissioner Sean Hughes said, ‘Disappointingly,

our work on the sale of CCI has highlighted widespread mis-selling and

poor product design. This remediation outcome is only one of many

examples where CCI has failed consumers. We expect insurers to cease to

sell insurance products that provide little or no value.’

‘We need a financial system that is fair. Insurers and

other financial institutions need to rise to the challenge and embed the

principle of fairness into their businesses to ensure we do not see any

further instances of this kind of poor value product being pushed on to

consumers’ added Mr Hughes.

Allianz will stop issuing new CCI policies from 30

September 2019. It will continue to fulfil its obligations to existing

CCI policyholders.

Allianz is expected to write to all affected consumers

about their refund offer from October 2019. Consumers with questions

about their cover should contact Allianz by email at here_to_help@allianz.com.au.

Background

ASIC’s recent review of the sale of CCI has resulted in

refunds of over $100 million due to more than 300,000 affected

consumers. On 11 July 2019, we released Report 622 Consumer credit insurance: Poor value products and harmful sales practices (REP 622) detailing our findings and setting minimum standards for lenders and insurers who issue or sell CCI (19-180MR).

ASIC is currently consulting on a proposal to ban the

sale of CCI and direct life insurance through unsolicited telephone

calls (19-188MR).

The proposed ban aims to address unfair sales conduct and protect

consumers from being sold products that they do not need, want or

understand.

ASIC has also commenced investigations into a number of entities that have been involved in mis-selling CCI to consumers.

Separately, in 2018, Allianz refunded $45.6 million to

68,000 consumers for add-on insurance sold through car dealerships that

were of little or no value (18-008MR).

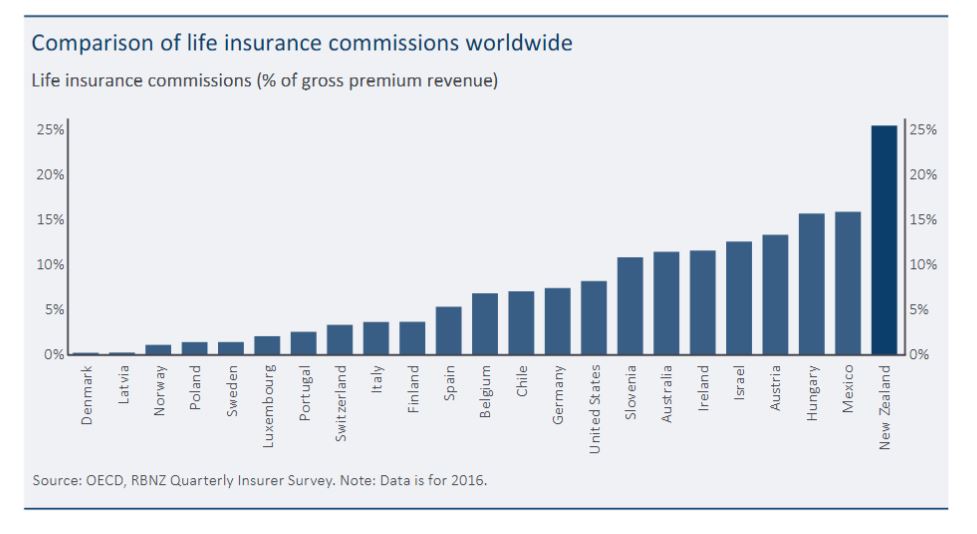

The Financial Markets Authority (FMA) and Reserve Bank of New Zealand (RBNZ) have completed their joint review of 16 New Zealand life insurers. This review follows the regulators’ bank review published in November 2018.

The findings appear to mirror the Australian Royal Commission, with a focus on shareholders rather than customers – sounds familiar? In addition commissions are extremely high in New Zealand.

Rob Everett, FMA Chief Executive said: “Overall the report shows the life insurance sector in a poor light. Life insurers have been complacent about considering conduct risk, too slow to make changes following previous FMA reviews and not sufficiently focused on developing a culture that balances the interests of shareholders with those of customers.”

The regulators found extensive weaknesses in life insurers’ systems and controls, with weak governance and management of conduct risks across the sector and a lack of focus on good customer outcomes.

Adrian Orr, Reserve Bank Governor said: “The industry must act urgently and undergo major change to address these weaknesses, as their services are vulnerable to misconduct and the escalation of issues that have been seen in other countries. Public trust in life insurers could be eroded unless boards and senior management transform their approach to conduct risk and achieve a customer-focused culture. Ultimately insurers need to take responsibility for whether customers are experiencing good outcomes from their products, regardless of how they are sold.”

Other key findings:

Limited evidence of products being designed and sold with good customer outcomes in mind.

Some insurers did little or nothing to assess a product’s ongoing suitability for customers.

Sales incentives structures risk sales being prioritised over good customer outcomes.

Where sales were through an intermediary, there was a serious lack of insurer oversight and responsibility for the sales and advice, and customer outcomes.

Remediation of conduct issues is generally very poor, with insurers slow to respond to issues and in some cases not sufficiently remediating them.

The review did not find widespread cases of misconduct on the part of life insurance companies. However, there were several instances of poor conduct. There were also a small number of cases of potential misconduct (i.e.: breaches of the law) that are now subject to investigations by the appropriate regulator.

Some of the issues and themes are similar to those highlighted in the Australia Royal Commission, albeit on a smaller scale. The FMA and RBNZ are not confident that insurers themselves are aware of all the current issues. This creates a serious risk of further conduct issues arising.

Next steps

All 16 life insurers will receive individual feedback. By 30 June 2019, each insurer will need to report back to the regulators. They will need to provide an action plan that the regulators will review, including how they will address incentives based on sales volumes for internal staff and commissions for intermediaries. Regular reporting on progress and implementation will be required.

Concerns for consumers

Purchasing life insurance is one of the most important financial decisions people will make. Customers should be able to have confidence their insurance will do what the insurance company or their financial adviser has told them. Many customers do experience the benefits of their insurance policies every year.

A positive finding in the report showed that, in general, frontline claims teams were focused on good outcomes with a strong desire to do the right thing for their customers.

The purpose of the thematic review and the report’s recommendations are to ensure the industry responds with urgency to the issues identified.

Further information and guidance for consumers can be found on the FMA website, here fma.govt.nz/investors/life/

Regulatory issues

Insurer conduct is currently only regulated indirectly through the FMA’s regulation of financial advice, which is generally provided by intermediaries. No one regulator has oversight of insurers’ and intermediaries’ conduct over the entire insurance policy lifecycle.

The report sets out some areas where the regulators recommend that the Government consider addressing regulatory gaps, similar to those put forward in our review of banks. The regulators acknowledge further policy work will be required and that any additional regulation will need to drive better outcomes for customers.

In a statement this morning, Bank of Queensland said the BOQ and Freedom had mutually agreed to terminate the St Andrews Insurance sale and purchase agreement.

“Following the termination of the agreement with Freedom, BOQ will continue to assess its strategic options in relation to St Andrew’s. In the meantime, St Andrew’s continues to be a strongly capitalised business that remains focused on delivering for its customers and corporate partners,” BOQ said.

The troubled Freedom Insurance Group last week completed its

strategic review, which was prompted by ASIC’s recommendations about the

life insurance industry.

As part of the review, which was conducted in collaboration with

Deloitte, the Freedom board identified that the company may face a

liquidity shortfall during calendar year 2019 arising from the timing of

payments of commission clawbacks in the absence of receipts of

commissions from new business sales.

Freedom had been pursuing equity funding for the purposes of the St Andrews acquisition, the process of which has included the provision of confidential due diligence to prospective third-party investors and negotiation of related transaction documentation.

it became clear that the conditions of the transaction would not be satisfied within the time limits contained in the sale agreement they said..

“In this regard, the company is considering alternate options to address the potential shortfall,” the group said in a trading update”.

“In addition, Freedom is implementing initiatives to improve operational efficiency and reduce costs.”

Freedom expects to make a provision for net remediation costs in its

financial accounts for the period ending 31 December 2018 of between

approximately $3 million and $4 million.

AMP was aware that it was charging dead customers life insurance premiums as far back as 2016 but failed to report the matter to regulators, the royal commission has heard, via InvestorDaily.

On Monday (17 September), the Hayne royal commission learned of a number of emails between AMP staff members dating back to 2016 raising the issue of insurance premiums being charged to dead people.

A 2016 email from an AMP staff member, Luke Wilson, regarding a claim being paid to a dead person observed that “this has been going on well before I started in the team”.

Counsel assisting Mark Costello questioned witness and AMP chief customer officer Paul Sainsbury about what Mr Wilson meant by this.

The AMP executive told the royal commission that, as he understood it, the “problem” had been going on for some time.

That problem, the commission learned, was AMP’s practice of charging dead people insurance premiums.

In another email, AMP staffer Luke Wilson wrote:

The issue is that [corporate superannuation] continued to charge premiums for the insurance even after AMP has been notified of the member’s passing. We have raised this with [sic] corp in the past and asked them why they continue to charge the insurance premiums once they are notified of a customer’s death. Back in 2016 I believe that they were of the understanding that premiums are refunded when the policy is paid, which is incorrect.

However, AMP only opened an investigation into the matter in April 2018, which was prompted by similar events at CBA, Mr Sainsbury told the commission.

“It was as a result of the CBA’s circumstances around premiums on deceased members. A question was asked in AMP ‘could this happen to us?’” Mr Sainsbury told the commission.

Counsel assisting Mark Costello asked: “Stopping the premiums being charged when you’ve been notified that the person is dead seems like a rather obvious step, doesn’t it?”

“Yes it does,” Mr Sainsbury said.

Costello: “But it wasn’t taken in 2016?”

Sainsbury: “No. The system was coded to refund it when the claim was admitted.”

Costello: “Why was that?”

Sainsbury: “I couldn’t tell you.”

The royal commission then heard about a case in which a customer had died on 24 February 2015 but premiums were still being deducted at June 2016. There was a request for the charged premiums to be reversed. The issue was not reported to ASIC.

“I can only assume the claim wasn’t admitted at that time. It’s a process as I’ve described. A refund occurs automatically by the system when a claim is actually finalised,” Mr Sainsbury explained.

Commissioner Hayne then sought further clarification of what Mr Sainsbury meant by a “refund”: “A refund of what is deducted? A refund plus the earnings it would have earned? A refund of what?”

“Commissioner, I believe it is a refund of the premiums,” Mr Sainsbury said.

“So the time value of money goes to AMP’s benefit?” the commissioner asked.

Mr Sainsbury replied: “Potentially.”

“Charging premiums for life insurance to someone who’s dead. That’s the position isn’t it?” Mr Hayne said.

“Yes,” said the AMP executive. “That’s the way the system is treating it today for a portion of our business.”

The royal commission heard that neither APRA nor ASIC were told that AMP was aware that it was charging life insurance premiums to dead people in 2016.

AMP charged 4,645 deceased persons life insurance premiums totalling approximately $1.3 million, the commission heard.

The Hayne royal commission has learned that the corporate watchdog allowed CBA to pay a substantially reduced fine despite misleading customers in its advertising, via InvestorDaily.

The royal commission has heard that ASIC not only gave CBA a severe discount for the misleading conduct but also let Australia’s biggest bank draft the media release regarding the action.

Senior counsel assisting Rowena Orr, QC opened Thursday’s hearing by questioning Helen Troup, the executive general manager of CBA’s insurance business CommInsure.

Ms Troup was taken through four pieces of advertising for CommInsure’s life and trauma insurance policy to determine how they discussed coverage for a heart attack.

Ms Troup accepted that in every case someone reading the adverts would believe the trauma policy covered all heart attacks.

The royal commission heard that CommInsure made a $300,000 voluntary community benefit payment as part of its agreement with ASIC to resolve the issue of misleading advertising.

Ms Orr pointed out to the commission that the maximum penalty for misleading conduct was 10,000 penalty units or almost $2 million per contravention.

In this instance, as Ms Troup had agreed to four adverts being misleading, it could have led to a fine of $8 million. But CommInsure only had to pay $300,000 as part of its agreement with ASIC to resolve the issue.

ASIC in fact seemed to have asked CBA if they thought the $300,000 was appropriate as Ms Orr read out to the commission a letter from the senior executive of ASIC, Tim Mullaly, addressed to CBA:

Could you please consider and let us know whether this is sufficient for CommInsure to resolve the matter, including by way of payment of the community benefit payment, in absence of infringement notices.

This provoked commissioner Hayne to ask if it was a case of the bank stipulating the terms of the punishment.

“The regulator asking the regulated whether the proposal was sufficient in the eyes of the party alleged to have broken the law, is that right?” he asked.

“We could have taken the approach of continuing to defend our position, so this was the alternative,” Ms Troup said.

Commissioner Hayne continued and asked Ms Troup if CommInsure viewed the community payment as a form of punishment.

“The $300,000 community benefit payment was a form of punishment,” she said.

Up until today’s hearing, CBA had not acknowledged the misleading adverts and had even advised ASIC on what language to use in their press release, said Ms Orr.

Ms Orr concluded by summarising that ASIC had given CommInsure notice of its findings, took no enforceable action and gave CommInsure the opportunity to make changes to the media release.