The Australian Competition and Consumer Commission has issued a draft determination proposing to deny authorisation to 16 insurance companies to agree to a cap of 20 per cent on commissions paid to car dealers who sell their add-on insurance products.

The Australian Securities and Investments Commission (ASIC) report, A market that is failing consumers: The sale of add-on insurance through car dealers (link is external), found that consumers are being sold expensive products that often provide little to no benefit. At the point of sale the consumer is focused on the purchase of a vehicle, not insurance, and the sales environment involves high-pressure selling tactics, a lack of adequate information, very high commissions, and conflicts of interest.

“The factors identified in ASIC’s report mean that consumers are often unable to make optimal, well-informed choices when buying add-on insurance products when buying a car from a dealer. A cap on commissions does not address these issues and will not remove the opportunity and incentive for insurers and dealerships to sell consumers expensive, poor value products,” ACCC Chairman Rod Sims said.

“This proposal doesn’t help to create an environment where consumers are in control and can benefit from effective competition. It is unlikely to address these market failures or improve the industry for consumers.”

“The ACCC considers that the proposed cap is unlikely to result in a public benefit.”

“While insurers would benefit from a cap at the expense of car dealers, this conduct is likely to lessen competition between insurers, including by creating greater opportunities for explicit or tacit collusion and greater shared knowledge between insurers of competitors’ costs.”

“The ACCC is also concerned that these arrangements, if implemented, could significantly delay the development of more effective solutions to the problems that ASIC has identified,” Mr Sims said.

Background

Add-on insurance products are products that may be sold at the time of purchasing a motor vehicle. The add-on insurance may be connected to finance associated with the motor vehicle such as consumer credit insurance, gap insurance, walk away insurance, and trauma insurance. Alternatively, it may relate to the vehicle itself, such as comprehensive insurance, extended warranty insurance, or tyre and rim insurance.

The corporate regulator’s review into insurance has uncovered concerns about how claims are handled but no evidence of industry-wide misconduct.

The Australian Securities and Investments Commission said on Wednesday that delays in claims handling and the evidence insurers require when assessing claims were the most common cause of disputes with customers.

The review of 15 insurers that make up 90 per cent of the industry showed that declined claim rates were highest for total and permanent disablement.

There were higher claims denial rates for insurance policies sold directly to consumers with no financial advice.

Some insurers had substantially higher than average declined claims rates and a substantially higher than proportionate share of disputes about claims.

However, nine out of 10 claims made on four major types of life insurance policy between 2013 to 2015 were paid out.

“While not finding evidence of cross-industry misconduct, ASIC’s review identified issues of conern in relation to higher claims denial rates and claims handling procedures,” ASIC said.

In a related probe, ASIC’s has obtained about 60,000 documents and has interviewed a range of people as part of its investigation into Commonwealth Bank’s CommInsure.

ASIC said it will work with the Australian Prudential Regulation Authority and insurers over 2017 to establish a public reporting regime that details claims outcomes and dispute levels.

“To improve public trust, there is a clear need for better quality, more transparent and more consistent data on life insurance claims,” it said.

Industry Super Australia chief executive David Whiteley said the recommendations were a step in the right direction, but that government should ban all sales commissions on life insurance.

“Given the importance of life insurance to Australians, the government and industry need to ensure that financial advice is only in the interests of consumers and all conflicts of interests are removed,” he said.

Law firm Maurice Blackburn principal Josh Mennen said an enforceable code of conduct and a Royal Comission were the only credible options for reform.

“The report identifies that particular insurers remain a problem, but does not identify specific insurers against its findings,” he said.

“The public has a right to know who the worst offenders are.”

ASIC says they have reviewed the sale of add-on general insurance policies through car dealers and found that the market is failing consumers.

Our report released today (REP 492) finds that consumers are being sold expensive, poor value products; products that provide consumers very little to no benefit; and a sales environment with pressure selling, very high commissions and conflicts of interest.

These products are sold to consumers when they purchase a new or used car, and cover risks relating to the car itself or relating to the loan that the consumer takes out to purchase the car. Examples include consumer credit insurance and tyre and rim insurance.

ASIC Deputy Chairman Peter Kell said, ‘There are serious problems in this market that need to be immediately and comprehensively addressed by insurers.’

‘ASIC will be undertaking further work, including potential enforcement action, to ensure that this market delivers acceptable outcomes for consumers. We will also be looking at how insurers can refund consumers who have been sold inappropriate products,’ said Mr Kell.

For the three year period that we reviewed, we found that:

Consumers obtained little financial benefit from buying add-on insurance, with consumers paying $1.6 billion in premiums and receiving only $144 million in successful insurance claims – representing a very low claims payout of nine per cent. For some major add-on products, the benefit to consumers was even lower, with consumer credit insurance claims payouts representing just five cents for each dollar of premium

Car dealers earned $602 million in commissions – over four times more than consumers received in claims, with commissions paid to car dealers as high as 79 per cent

Payment for these insurance products is commonly packaged into the consumer’s car loan as a single upfront premium. This can substantially increase the cost of the product by increasing the loan amount and interest paid. Research shows that consumers are often unaware that they even have the policy when it is paid upfront as a single premium, and they may not get a premium refund if they repay their car loan early. Policies have been sold where it is impossible for the consumer to receive a claim payout that is greater than the cost of the insurance

The car sales environment inhibits good decision making about these products because of the conflicts of interest and pressure sales built into the distribution model. The consumer is focussed on purchasing a car and financing that purchase – not on the details of the complex insurance policy

Today’s report follows ASIC’s release of two reports in February this year about the sale of add-on life insurance by car dealers. ASIC stressed the need for insurers to address the high costs, poor value and poor claim outcomes of life insurance products sold this way.

ASIC is putting general insurers on notice that they need to improve consumer outcomes by making substantial changes to the pricing, design and sale of add-on insurance products or face additional regulatory action. The key commitments we are seeking from insurers are:

A significant reduction in the amount of commissions paid to anyone who sells an add-on insurance product through car dealers

A significant improvement in the value offered by these products, through substantial reductions in price and better product design and cover

A move away from single upfront premiums that are financed through the loan contract, given the adverse financial impact this has on consumers

Providing refunds to consumers who have been sold policies in circumstances that were unfair, such as where a policy has been sold to a consumer who was never eligible to claim under the policy

Insurers have notified ASIC that they intend to implement a 20 per cent cap on commissions, which is a positive step. Insurers in this market will be also providing ASIC with data on prices, premiums and claims on a regular basis so that we can monitor the impact of changes on consumers.

ASIC Deputy Chairman Peter Kell said, ‘While we welcome the initial steps taken by the insurers to improve the value of these products for consumers, there is still a long way to go. If industry does not deliver swift improvements for consumers, ASIC will take further action, including enforcement action where appropriate.’

ASIC’s review of these products is ongoing. ASIC will continue to work with insurers and consumer representatives to ensure that proposals for change deliver significantly improved value to consumers.

The General Insurance sector is one of the laggards across financial services when it comes to digital transformation. However, according to a new report from McKinsey, whilst the sector lags in digital sophistication and so examples of the full benefits of digital are scarce; they suggest that the top 20 or 30 processes can account for up to 40 percent of costs and 80 to 90 percent of customer activity. Digitizing these processes can take out 30 to 50 percent of the human service costs while delivering a much better customer experience. And the benefits do not end there.

The nature of competition in property and casualty (P&C) insurance is shifting as new entrants, changing consumer behaviors, and technological innovations threaten to disrupt established business models. Though the traditional insurance business model has proved remarkably resilient, digital has the power to reshape this industry as it has many others. Innovations from mobile banking to video and audio streaming to e-books have upended value chains and redistributed value pools in industries as diverse as financial services, travel, film, music, and publishing. As new opportunities emerge, those insurers that evolve fast enough to keep up with them will gain enormous value; the laggards will fall further behind. To succeed in this new landscape, insurers need to take a structured approach to digital strategy, capabilities, culture, talent, organization, and their transformation road map.

Though the P&C insurance business has long been insulated against disruption thanks to regulation, product complexity, in-force books, intermediated distribution networks, and large capital requirements, this is changing. Sources of disruption are emerging across the value chain to reshape:

Products. Semiautonomous and autonomous vehicles from Google, Tesla, Volvo, and other companies are altering the nature of auto insurance; connected homes could transform home insurance; new risks such as cybersecurity and drones will create demand for new forms of coverage; and Uber, Airbnb, and other leaders in the sharing economy are changing the underlying need for insurance.

Marketing. Evolving consumer behavior is threatening traditional growth levers such as TV advertising and necessitating a shift to personalized mobile and online channels.

Pricing. The combination of rich customer data, telematics, and enhanced computing power is opening the door to usage- and behavior-based pricing that could reduce barriers to entry for attackers that lack the loss experience formerly needed for accurate pricing.

Distribution. New consumer behaviors and entrants are threatening traditional distribution channels. Policyholders increasingly demand digital-first distribution models in personal and small commercial lines, while aggregators continue to pilot direct-to-consumer insurance sales. Armed with venture capital, start-ups like Lemonade—which raised $13 million in seed funding from well-known investors including Sequoia Capital—are exploring peer-to-peer insurance models.

Service. Consumers expect personalized, self-directed interactions with companies via any device at any hour, much as they do with online retail leaders like Amazon.

Claims. Automation, analytics, and consumer preferences are transforming claims processes, enabling insurers to improve fraud detection, cut loss-adjustment costs, and eliminate many human interactions. Connected technologies could allow policyholders and even smart cars and networked homes to diagnose their own problems and report incidents. Self-service claims reporting such as “estimate by photo” can create fast, seamless customer experiences. Drones can be used to assess damage quickly, safely, and cheaply after catastrophes. All these disruptions are being driven and enabled by digital advances, as illustrated with examples from auto insurance. No single competitor or innovation poses a threat across the entire value chain, but taken together, they could lead to the proverbial death by a thousand cuts: many small disruptions combining to fell a giant.

Volatility in financial markets globally and competition from smaller “challengers” like Youi (an Australian registered company owned by South Africa’s Rand Merchant Investment Holdings) have been driving down big insurance companies’ profits, putting pressure on these companies to find ways of cutting costs.

Figures released by the Australian Prudential Regulation Authority (APRA) reveal the performance of the Australian insurance sector as a whole.

APRA figures show that revenue is declining across the sector. For the 110 insurers in the Australian market, bottom line profit after tax declined substantially from a combined $4.1 billion to $2.4 billion in 2015, a drop of 73%.

The total cost of claims made by policyholders was effectively flat for 2015, so the main driver of the slump in profit was the downturn in global financial markets. When policyholders pay their insurance premiums, insurers don’t hold these as cash. In fact, of the $119 billion of total assets of Australian insurance companies, less than 2% is held as cash. Instead, a substantial portion – $68.4 billion (57%) – is invested, with over $50 billion held as interest bearing assets such as bonds.

For the 2014 calendar year, investment returns for the sector as a whole were slightly over $4.2 billion, whereas in 2015 investment returns nearly halved to $2.2 billion. In the year ahead there may be more of a threat to insurance companies from investments in the markets.

In the first months of 2016 in Australia, the All Ordinaries Index has fallen nearly 8% and there are indicators that returns for both global bonds and shares may not improve much in the short term. Australian insurers may have to look elsewhere for returns on investments.

Increasing competition

Insurers will need to both increase revenue and decrease expenses to ensure sustainable profitability. The major insurers have embarked on cost cutting plans, which do seem to be having the desired effect.

This is important, as challenger companies the likes of Youi and Budget Direct are taking a small, but growing, portion of the $16 billion personal insurance market (which includes home, content and motor), currently dominated by IAG and Suncorp Group. This level of competition is seen in the APRA figures, which indicate that the while total premiums increased by just under 4%, the number of policyholders also increased (by over 4%), so the premium per policyholder actually declined by 1% from $612 to $605.

This increase in competition doesn’t necessarily mean a price war in the insurance sector. Gary Dransfield, personal insurance chief executive at insurer Suncorp says his company won’t look to recover its lost market share by reducing premiums.

“We don’t think that’s the way to deal with the competitive environment.”

However, if competition continues to intensify, the ability for insurers to increase premiums is somewhat limited.

Technology

Insurers may be able to make savings by improving the use of technology that gives these companies insight into customers’ actions. These technologies include telematics and Big Data. Telematics is the use of communications devices to send, receive and store information relating to a remote object, such as a vehicle. Big Data relates to large amounts of data creation, storage, retrieval and analysis. Both of these technologies allow insurance companies to better understand their customers.

Which is important, because the purpose of insurance companies is to collect premiums for those they insure, and to pay out to those few who do have to call upon their insurance protection (i.e. for hail damage to a car, or flood damage to a house). A major impact on profitability is the ability of an insurance company to properly assess and price the risk that the company will have to pay out. This is why the premiums for younger drivers are higher, as they judged to be a higher risk of having an at-fault claim.

More detailed information about policyholders improves the ability of insurance companies to do that, and this can occur in a variety of ways. Rather than simply base the risk of the policyholder on general category information such as age, gender, or the postcode where the vehicle is garaged, factors such as the number of kilometres driven, the time of day and location of the driving, and even speed zones provide valuable insights to insurers.

Gathered information on customers also assists insurers in other ways. In 2013 IAG purchased Wesfarmers’ insurance business for close to $2 billion, allowing it to get a better grasp of consumer choices through rewards cards purchases and permitting it to tailor insurance products accordingly.

The insurance sector is inevitably at the mercy of natural disasters – and Australia has experienced increasingly intense storms, bushfires and cyclones in recent years. But it is also facing stormy conditions on investment markets and in the competitive landscape. Those insurers that innovate – making the best use of sophisticated data science and financial tools – will weather difficult times best.

Authors: David Bon, Senior Lecturer, Accounting Discipline Group, University of Technology Sydney; Anna Wright, Senior lecturer, University of Technology Sydney.

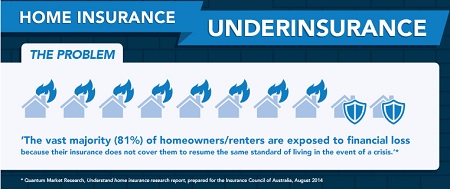

The vast majority of households with home insurance may well be exposed to unexpected loss according to ASIC. Following a survey of 23 home insurance brands covering 12 insurers, ASIC is calling for further improvements across the sector to help consumers make good decisions about their home insurance cover.

In response to ASIC’s recommendations from October 2014, insurers have made a range of improvements. In particular, most insurers have implemented, or are implementing, the following changes:

Incorporating a sum insured calculator into point of sale processes, including through updated sales scripts, and providing better access to online calculators. This helps consumers select an appropriate sum insured amount during the quote and sales process, an important way to help reduce the risk of underinsurance; since October 2014, four additional insurers have made available sum insured calculators in both their telephone and online sales channels.

Training staff so that information provided to consumers about the sum insured, and the maximum amount paid by the insurer, is clear and in plain English; since October 2014, an additional eight insurers have adopted this practice for their telephone sales and an additional 11 for their online sales.

Providing information or assistance to consumers about the effect of changes to building codes which may increase the cost of rebuilding homes after a total loss; since October 2014, four additional insurers have made changes to provide this information.

Although welcoming these changes, ASIC’s survey identified that there is scope for insurers to take additional steps. In particular, we would like insurers to help consumers select the right insurance cover by:

explaining that the sum insured amount needs to enable complete replacement of contents or complete rebuilding of their home;

providing guidance about coverage or sum insured amounts, rather than simply referring consumers to the product disclosure statement;

referring to the Key Facts Sheet to assist decision making; and

providing information and guidance about natural perils risks and additional rebuilding costs due to natural perils, to better estimate rebuilding costs after a total loss.

An example of an initiative that is aimed at providing more information and guidance to consumers is one insurer’s website that allows consumers to enter their suburb or postcode and receive targeted information about that area including relevant risks, types of claims, types of weather events, and a dollar figure for how much other consumers in the area insure their building and contents.

ASIC has been working with the insurance industry to better understand barriers to the provision of financial product advice to consumers purchasing home insurance. ASIC has already taken steps to encourage and facilitate insurers operating under general advice models to provide useful information to consumers.

‘ASIC is keen to see industry make improvements in all of the areas identified in ASIC’s 2014 report,’ ASIC Deputy Chair Peter Kell said.

‘Our goal is to make sure that consumers buy insurance that better meets their needs – including by helping to reduce levels of underinsurance, especially when there are natural disasters.’

ASIC will continue this work with the insurance industry to further enhance the sector’s ability to assist consumers in purchasing home insurance that better meets their needs.

Background

ASIC released two reports in October 2014 exploring consumer experiences with the sale of home insurance.

In Report 415, ASIC reviewed the sales practices of 13 insurers who sell home insurance across Australia. Report 415 found that for sum insured policies, it is important to help consumers to set an appropriate sum insured amount, so that they are adequately insured in the event of a total loss.

Most home insurance policies in Australia are ‘sum insured’ policies, where the insurer agrees to pay only up to an agreed amount (the sum insured), nominated by the consumer, to repair or rebuild a damaged or destroyed home.

ASIC encourages insurers to inform consumers that the building sum insured amount should reflect the amount that it would cost to completely rebuild their home. Similarly, the contents sum insured amount should reflect the amount it would cost to completely replace all contents with new items at today’s prices. The sum insured amount should also reflect the cost to rebuild the consumer’s home to meet new building codes and standards, and any other supplementary costs. For information on supplementary costs see MoneySmart’s page on home insurance supplementary costs

Findings from Report 415 were considered in the Financial System Inquiry which called for improved guidance (including tools and calculators) and disclosure for general insurance, especially in relation to home insurance. The Government has agreed to support work by industry to increase guidance and disclosure in general insurance.

ASIC also notes and welcomes subsequent industry recommendations targeted at effective disclosure. Some of the Effective Disclosure Taskforce’s recommendations align with ASIC’s findings, particularly in relation to improving the provision of information to consumers about natural hazard risk, and integrating sum insured calculators into the sales process.

A new IMF working paper investigates the emerging global landscape for public-private co-investments in infrastructure. The creation of the Asian Infrastructure Investment Bank and other so-called “infrastructure investment platforms” are an attempt to tap into the pool of both public and private long-term savings in order to channel the latter into much needed infrastructure projects. This paper puts these new initiatives into perspective by critically reviewing the literature and experience with public private partnerships in infrastructure. It concludes by identifying the main challenges policymakers and other actors will need to confront going forward and to turn infrastructure into an asset class of its own.

Institutional investors such as pension funds, insurance companies and mutual funds, and other investors such as sovereign wealth funds hold around $100 trillion in assets under management. One gets a clearer grasp of the enormous size of this global wealth by comparing it to US nominal GDP $18 trillion in 2015.

Against this backdrop of a largely untapped pool of global savings, estimates suggest that the world needs to increase its investment in infrastructure by nearly 60 percent until 2030. There is a huge infrastructure investment gap in a large number of countries. The average infrastructure investment gap amounts to between $1 to 1.5 trillion per year. Infrastructure investment needs are mostly earmarked for upgrading depreciating brownfield infrastructure projects in the EU and in the US and for greenfield investments in low-income and emerging markets. The future growth in the demand for infrastructure will come increasingly from emerging economies.

There is growing recognition globally that development banks can play an important role in facilitating the preparation and financing of infrastructure projects by private long-term investors. A number of infrastructure platform initiatives have been launched very recently, most of them still at a prototype development stage. We discuss four different models that are currently at various stages of development. These platforms are all different attempts to tap into the vast pool of global long-term savings by better meeting long-term investor needs to attract them to infrastructure assets and by relaxing operating and governance constraints traditional development banks have been facing.

A first obvious lesson from an analysis of these platforms, is that the ability of development banks to leverage public money –committed capital from government contributions—by attracting private investors as co-investors in infrastructure projects is increasing the efficiency of development banks around the world. It is not just the fact that development banks are able to invest in larger-scale infrastructure projects and thus obtain a greater bang for the public buck, but also that these private investors together with development banks can achieve more efficient PPP concession contracts. Development banks are not just lead investors providing some loss absorbing capital to private investors. They also give access to their expertise and unique human capital to private investors, who would otherwise not have the capabilities to do the highly technical, time-consuming, due diligence to identify and prepare infrastructure projects. In addition, they offer a valuable taming influence on opportunistic government administrations that might be tempted to hold up a private PPP concession operator. Private investors in turn keep development banks in check and ensure that infrastructure projects are economically sound and not principally politically motivated. No wonder that this platform model is increasingly being embraced by development banks around the world.

The paper has documented that new platforms of investments have emerged. Notwithstanding, they are confronted with serious structural limitations. These platforms will certainly help on two important fronts namely on financing and origination of infrastructure projects, which this paper has focused on. Formally integrating these dimensions in models of PPP are important avenues for academic research.

Besides financing and origination, there are other important challenges to complete the broader task that lie ahead, such as in making infrastructure investment an asset class of its own. Two important directions are needed to further the agenda. First, the lack of standardization of underlying infrastructure projects is an important impediment to the scaling up of investment into infrastructure-based assets. Large physical infrastructure projects are indeed complex and can differ widely from one country to the next. In that respect, making use of securitization techniques such as collateralized bond obligations (or CBOs) or collateralized loan obligations (or CLOs) allow for better price discovery which will enhance the efficiency of the market and allow a more effective pooling of risk. It would also allow to “bulk up” the bond offering by addressing the problem of insufficient large sized bond issues. Overall, securitization will provide many advantages such as diversification for investors, lower cost of capital by allowing senior tranches to be issued with higher credit ratings, as well as higher liquidity. At the same time, securitization also creates debt instruments of variable credit risks to match the different risk appetites of investors. Second, there are important complementarities between actors participating in the “value chain” created by platforms including host countries, financial investors, guarantors and financial intermediaries. For all these reasons, the EIB has recently launched a renewable energy platform for institutional investors (REPIN) to offer repackaged renewable energy assets in standardized, liquid forms to institutional investors15. Although interest from institutional investors has been limited so far, the new carbon footprint disclosures and regulations of institutional investors that are expected be implemented after the Paris COP 21 climate summit, could nudge more pension and sovereign wealth funds to take on these securities.

Finally, host countries may put forth viable long term infrastructure projects but without the provision of guarantees to address construction, demand, exchange rate risks or without the securitization of underlying assets by financial intermediaries, those projects will not be funded, thus leaving everyone worse off. There is obviously also a need for enhanced coordination and cooperation across the various platforms in existence and for the creation of a global infrastructure investment platform. Part of the coordination should lead to risks being assumed by those best placed to hold them. Governments are the natural holders of political, regulatory and governance risks. The private sector for obvious incentive reasons should take on most of the construction risk, and demand risk should probably be shared, depending on the sector and type of project.

Note: IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage debate.The views expressed in IMF Working Papers are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board,or IMF management.

The Government has released draft legislation for public comment. By way of background, on 6 November 2013, the Government announced that it would proceed with a 10 per cent non-final withholding tax on the disposal, by foreign residents, of certain taxable Australian property. The purpose of the regime is to assist in the collection of foreign residents’ capital gains tax liabilities.

Where the seller of certain Australian assets is a foreign resident, the buyer will be required to pay 10 per cent of the price to the Australian Taxation Office as withholding tax. This obligation will apply to the acquisition of an asset that is taxable Australian real property; an indirect Australian real property interest; or an option or right to acquire such property or interest.

This withholding obligation will not apply to residential property valued under $2.5 million. The purpose of this exclusion is to minimise compliance costs and ensure that the amendments are clearly inapplicable to most residential property sales conducted between Australian residents. This alleviates the need for purchasers to undertake the preliminary compliance obligation of determining the residency status of the vendor.

In October 2014, the Government released a discussion paper consulting on the design of the measure.

Closing date for submissions is Friday, 7 August 2015.

Though the P&C insurance business has long been insulated against disruption thanks to regulation, product complexity, in-force books, intermediated distribution networks, and large capital requirements, this is changing. Sources of disruption are emerging across the value chain to reshape:

Against this backdrop of a largely untapped pool of global savings, estimates suggest that the world needs to increase its investment in infrastructure by nearly 60 percent until 2030. There is a huge infrastructure investment gap in a large number of countries. The average infrastructure investment gap amounts to between $1 to 1.5 trillion per year. Infrastructure investment needs are mostly earmarked for upgrading depreciating brownfield infrastructure projects in the EU and in the US and for greenfield investments in low-income and emerging markets. The future growth in the demand for infrastructure will come increasingly from emerging economies.

There is growing recognition globally that development banks can play an important role in facilitating the preparation and financing of infrastructure projects by private long-term investors. A number of infrastructure platform initiatives have been launched very recently, most of them still at a prototype development stage. We discuss four different models that are currently at various stages of development. These platforms are all different attempts to tap into the vast pool of global long-term savings by better meeting long-term investor needs to attract them to infrastructure assets and by relaxing operating and governance constraints traditional development banks have been facing.A first obvious lesson from an analysis of these platforms, is that the ability of development banks to leverage public money –committed capital from government contributions—by attracting private investors as co-investors in infrastructure projects is increasing the efficiency of development banks around the world. It is not just the fact that development banks are able to invest in larger-scale infrastructure projects and thus obtain a greater bang for the public buck, but also that these private investors together with development banks can achieve more efficient PPP concession contracts. Development banks are not just lead investors providing some loss absorbing capital to private investors. They also give access to their expertise and unique human capital to private investors, who would otherwise not have the capabilities to do the highly technical, time-consuming, due diligence to identify and prepare infrastructure projects. In addition, they offer a valuable taming influence on opportunistic government administrations that might be tempted to hold up a private PPP concession operator. Private investors in turn keep development banks in check and ensure that infrastructure projects are economically sound and not principally politically motivated. No wonder that this platform model is increasingly being embraced by development banks around the world.The paper has documented that new platforms of investments have emerged. Notwithstanding, they are confronted with serious structural limitations. These platforms will certainly help on two important fronts namely on financing and origination of infrastructure projects, which this paper has focused on. Formally integrating these dimensions in models of PPP are important avenues for academic research.Besides financing and origination, there are other important challenges to complete the broader task that lie ahead, such as in making infrastructure investment an asset class of its own. Two important directions are needed to further the agenda. First, the lack of standardization of underlying infrastructure projects is an important impediment to the scaling up of investment into infrastructure-based assets. Large physical infrastructure projects are indeed complex and can differ widely from one country to the next. In that respect, making use of securitization techniques such as collateralized bond obligations (or CBOs) or collateralized loan obligations (or CLOs) allow for better price discovery which will enhance the efficiency of the market and allow a more effective pooling of risk. It would also allow to “bulk up” the bond offering by addressing the problem of insufficient large sized bond issues. Overall, securitization will provide many advantages such as diversification for investors, lower cost of capital by allowing senior tranches to be issued with higher credit ratings, as well as higher liquidity. At the same time, securitization also creates debt instruments of variable credit risks to match the different risk appetites of investors. Second, there are important complementarities between actors participating in the “value chain” created by platforms including host countries, financial investors, guarantors and financial intermediaries. For all these reasons, the EIB has recently launched a renewable energy platform for institutional investors (REPIN) to offer repackaged renewable energy assets in standardized, liquid forms to institutional investors15. Although interest from institutional investors has been limited so far, the new carbon footprint disclosures and regulations of institutional investors that are expected be implemented after the Paris COP 21 climate summit, could nudge more pension and sovereign wealth funds to take on these securities.Finally, host countries may put forth viable long term infrastructure projects but without the provision of guarantees to address construction, demand, exchange rate risks or without the securitization of underlying assets by financial intermediaries, those projects will not be funded, thus leaving everyone worse off. There is obviously also a need for enhanced coordination and cooperation across the various platforms in existence and for the creation of a global infrastructure investment platform. Part of the coordination should lead to risks being assumed by those best placed to hold them. Governments are the natural holders of political, regulatory and governance risks. The private sector for obvious incentive reasons should take on most of the construction risk, and demand risk should probably be shared, depending on the sector and type of project.