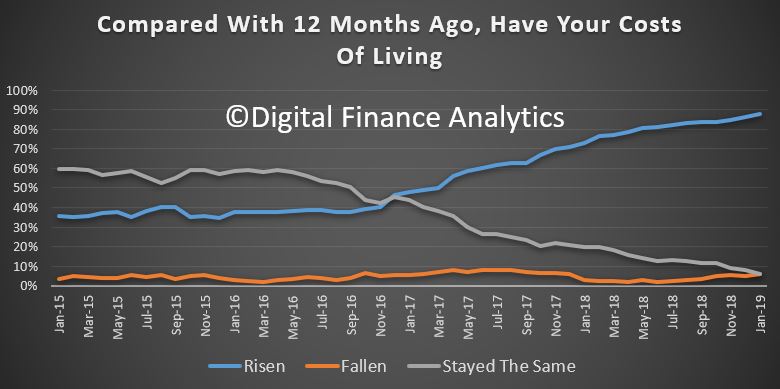

In the latest show John Adams and I discuss the theory that Australia is different, and will not see an economic crisis.

The full show (28 mins) is available on our “In The Interests of The People” channel.

This is a short, but complete extract.

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

In the latest show John Adams and I discuss the theory that Australia is different, and will not see an economic crisis.

The full show (28 mins) is available on our “In The Interests of The People” channel.

This is a short, but complete extract.

ASIC has today issued a consultation paper to update its guidance on responsible lending (CP 309).

The changes appear mainly clarifications and tweaks to language rather than substantive changes. But it does underscore the lenders obligations to make reasonable inquiries when making a loan. Nothing here that would open the credit taps, that I can see.

They are asking questions about credit which currently falls outside the guidelines, such as SACC and Business loans.

They do address HEM benchmarks saying that ” A benchmark figure does not provide any positive confirmation of what a particular consumer’s income and expenses actually are”. Its a plausibility test.

We propose to clarify our guidance in RG 209 on the use of benchmarks as follows:

(a) A benchmark figure does not provide any positive confirmation of what a particular consumer’s income and expenses actually are. However, we consider that benchmarks can be a useful tool to help determine whether information provided by the consumer is plausible (i.e. whether it is more or less likely to be true and able to be relied upon).

(b) If a benchmark figure is used to test expense information, licensees should generally take the following kinds of steps: (i) ensure that the benchmark figure that is being used is a realistic figure, that is adjusted for variables such as different income ranges, dependants and geographic location, and that is not merely reflective of ‘low budget’ spending; (ii) if the benchmark figure being referred to is more reflective of ‘low budget’ spending (such as the Household Expenditure Measure), apply a reasonable buffer amount that reflects the likelihood that many consumers would have a higher level of expenses; and (iii)periodically review the expense figures being relied upon across the licensee’s portfolio—if there is a high proportion of consumers recorded as having expenses that are at or near the benchmark figure, rather than demonstrating the kind of spread in expenses that is predicted by the methodology underlying the benchmark calculation, this may be an indication that the licensee’s inquiries are not being effective to elicit accurate information about the consumer’s expenses

This is the ASIC announcement:

ASIC’s guidance has been in place since 2010 when the responsible lending laws were first introduced. Although the laws have not changed since 2010, ASIC considers it timely to review and update the guidance in light of its regulatory and enforcement work since 2011, changes in technology, and the recent Final Report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

Our review of RG 209 will consider whether the guidance remains effective and identify changes and additions to the guidance that may help holders of an Australian credit licence to understand ASIC’s expectations for complying with the responsible lending obligations.

ASIC welcomes submissions on the update of our guidance on responsible lending from any interested party. In the consultation paper we have asked a series of questions about specific matters. We are also keen to hear from stakeholders about any other issues considered important that are not dealt with in the consultation paper.

ASIC is also considering whether to provide an opportunity for key stakeholders to speak to the Commission at public hearings in addition to making written submissions.

Further information about the consultation and its progress will be available on the ASIC website.

“The responsible lending obligations are an integral part of the regulatory framework for all consumer loans” said ASIC Commissioner Sean Hughes. “ASIC wants to ensure its guidance provides industry with certainty, including as a result of emerging technology and initiatives such as open banking and comprehensive credit reporting. We encourage everybody to participate in this extensive consultation process”.

The consultation is open for a period of three months, with comments due by Monday 20 May 2019.

Regulatory Guide 209 Credit licensing: Responsible lending conduct (RG 209) contains ASIC’s guidance on responsible lending for consumer credit. RG 209 was issued in 2010 and last revised in November 2014.

Since then there have been many matters that now mean it is timely for ASIC to update its guidance.

ASIC has also received anecdotal feedback that licensees may be applying the responsible lending obligations where the law does not require them to be applied (e.g. in small business lending). We are seeking feedback on whether there is a need to include some additional guidance in RG 209 which sets out particular examples where the law does not require responsible lending or related obligations to apply.

The new CO:Lab home loans, a collaboration between Tic:Toc and the $7 billion La Trobe Financial, can help self-employed Australian’s and business owners excluded by traditional eligibility requirements, as well as customers looking to refinance to invest money into their business.

Tic:Toc launched the World’s first instant home loan™ in July 2017 in partnership with Bendigo and Adelaide Bank, and is now collaborating with another key partner and shareholder, La Trobe Financial, to help bring the home loan process up to speed for a broader range of self-employed and small business applicants.

Announcing the launch of CO: Lab, Tic:Toc founder and CEO, Anthony Baum, said while major lenders continue to tighten lending to small businesses, Tic:Toc has specifically broadened its home loan suite to offer digital home loans to many more Australians, including a broader range of self-employed professionals and small business owners.

“More than 17% of Australians work for themselves, so it’s important home loans keep pace with the shifting workforce to support self-employed customers. “Australia’s self-employed and small business owners have traditionally endured a notoriously difficult home loan process, with an often impractical burden to provide large amounts of documentation.

“Our partnership with La Trobe Financial, one of Australia’s longest operating and leading non-bank credit specialists, has created a broader set of loan options via Tic:Toc’s streamlined home loan assessment and approval technology. This means business owners and self-employed customers now have more loan options, with less hassle and at a lower cost.

“For example, a business owner can use the equity in their home to invest in their business at home loan prices. This could save them up to around 6% per year on standard business loans from the major banks, and they can apply and be approved the same-day via our award-winning online platform.

La Trobe Financial President and CEO, Greg O’Neill said, “As a key shareholder in Tic:Toc, we’re excited to partner with Tic:Toc in developing and launching digital CO:Lab home loans and bring this unique digital approach to market for Australia’s business owners needing finance at such a very important time in the credit cycle. “As one of Australia’s longest operating and leading non-bank credit specialists, we want to support innovation in our industry. We are very proud to back Tic:Toc as they embrace smarter and more customer centric ways to assess and secure home loan and other finance for a broader range of clients moving forward.

Wayne Byres, APRA Chairman spoke at the Financial Stability Institute (FSI) Executives’ Meeting of East Asia-Pacific Central Banks (EMEAP) – Basel Committee on Banking Supervision (BCBS) High Level Meeting, Sydney in Sydney.

He gave APRA a good wrap for is progress on the Basel based supervisory framework. His comments on their mortgage sector interventions were, well, interesting (I would say, too little too late!).

In 2014, we initiated a quite intensive supervisory effort to lift and reinforce lending standards. Our concern was that due to strong competitive pressures, policies were not suitably calibrated to the Australian environment at the time – one of high and rising house prices, high household debt, subdued household income growth and historically low interest rates. We issued additional supervisory guidance, and allocated significant resources to ensure lending policies were suitably aligned with it. Unfortunately, this provided evidence that strong incentives to grow profit and market share often saw lenders weaken and/or override policies in order to generate sales. Moreover, the dangers did not seem to be strongly called out by compliance and audit functions.

To me, the perspective he paints is still far too narrow in terms of really tacking financial stability, Basel is but one element, not the universe!

Here is his introduction…

Translating prudential policy into prudent practice

I’ve been asked to speak this morning about the challenge of translating prudential policy into prudent practice. From a global perspective, that’s an important issue to focus on because policy reform will mean little if it does not translate into improved practices and behaviours.

Translating global reform proposals to improved banking practice is a four-step process:

The first of these steps is pretty much complete. A decade on from the financial crisis, the marathon international policy-making efforts to restore and protect the resilience of the global banking system have, by and large, reached the finish line. Greatly strengthened risk-based capital requirements, a supplementary leverage ratio, with additional buffers for systemically important banks, liquidity and funding requirements in the form of the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR), tighter large exposure limits and new margining requirements for OTC derivatives, and an enhanced disclosure regime provide a comprehensive package of prudential policy reforms. The Basel Committee has worked long and hard, and should be commended for the final product.

The Basel Committee’s output – besides lots of paper! – are agreements on the design and calibration of minimum standards. Those agreements are critical to global financial stability. Unfortunately, they are not worth the paper they are written on if they are not translated into domestic regulation by member jurisdictions – the second step in the process I referred to earlier. To repeat the frequent exhortations of the G20 leaders, to achieve the desired objective of a resilient global financial system the reforms need to be implemented in a “full, timely and consistent manner”.

A quick look at the Basel Committee’s latest implementation monitoring report shows something of a mixed scorecard. While the core Basel III risk-based capital requirements and the LCR are largely in force around the world, there has been less progress in some other areas: many requirements are subject to lengthy transitional periods, implementation of the NSFR has been disappointingly slow in a number of jurisdictions, and margining and disclosure requirements can be described as a little patchy.

In short, not all commitments to act have been met by action. That is disappointing. While some delays and trade-offs are valid, on occasion it appears to reflect a regulatory version of the “first mover disadvantage” that supervisors often criticise the industry for – jurisdictions not wanting to do the right thing and move promptly because of a concern that other jurisdictions may not follow suit. This reveals a disappointing penchant to put the interests of banks and their shareholders above that of their depositors and the broader community – something that prudential supervisors must constantly guard against.

For our part, we’ve made good progress on the financial reform agenda in Australia. While the banking sector here escaped the worst of the crisis a decade ago, that didn’t mean APRA was complacent about the importance of building resilience. The core capital, liquidity and funding reforms of Basel III are all in place, with a conservative overlay in many areas. Moreover, we have done this without the extensive transitional periods that have been necessary in other parts of the world. I acknowledge, though, that we don’t have a perfect record and still have a few gaps to close, such as the enhanced Pillar III disclosure requirements. We are committed to addressing these as soon as we can.

The New Zealand Reserve Bank said today that the Official Cash Rate (OCR) remains at 1.75 percent. They expect to keep the OCR at this level through 2019 and 2020. The direction of the next OCR move could be up or down.

Employment is near its maximum sustainable level. However, core consumer price inflation remains below our 2 percent target mid-point, necessitating continued supportive monetary policy.

Trading-partner growth is expected to further moderate in 2019 and global commodity prices have already softened, reducing the tailwind that New Zealand economic activity has benefited from. The risk of a sharper downturn in trading-partner growth has also heightened over recent months.

Despite the weaker global impetus, they expect low interest rates and government spending to support a pick-up in New Zealand’s GDP growth over 2019. Low interest rates, and continued employment growth, should support household spending and business investment. Government spending on infrastructure and housing also supports domestic demand.

As capacity pressures build, consumer price inflation is expected to rise to around the mid-point of our target range at 2 percent.

There are upside and downside risks to this outlook. A more pronounced global downturn could weigh on domestic demand, but inflation could rise faster if firms pass on cost increases to prices to a greater extent.

They will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

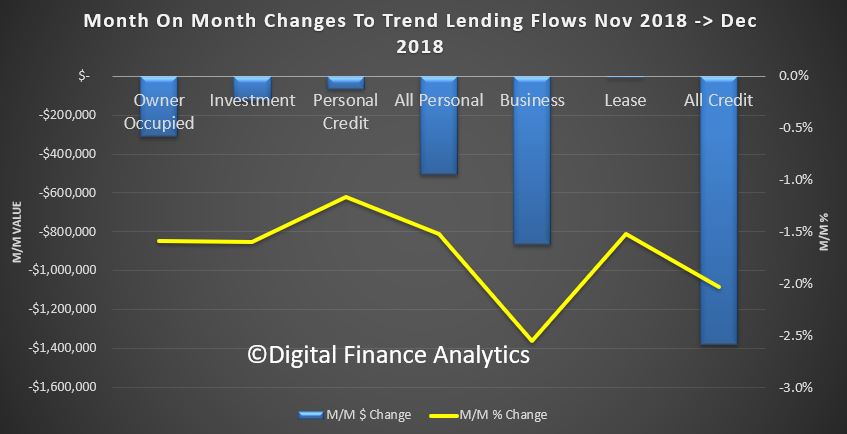

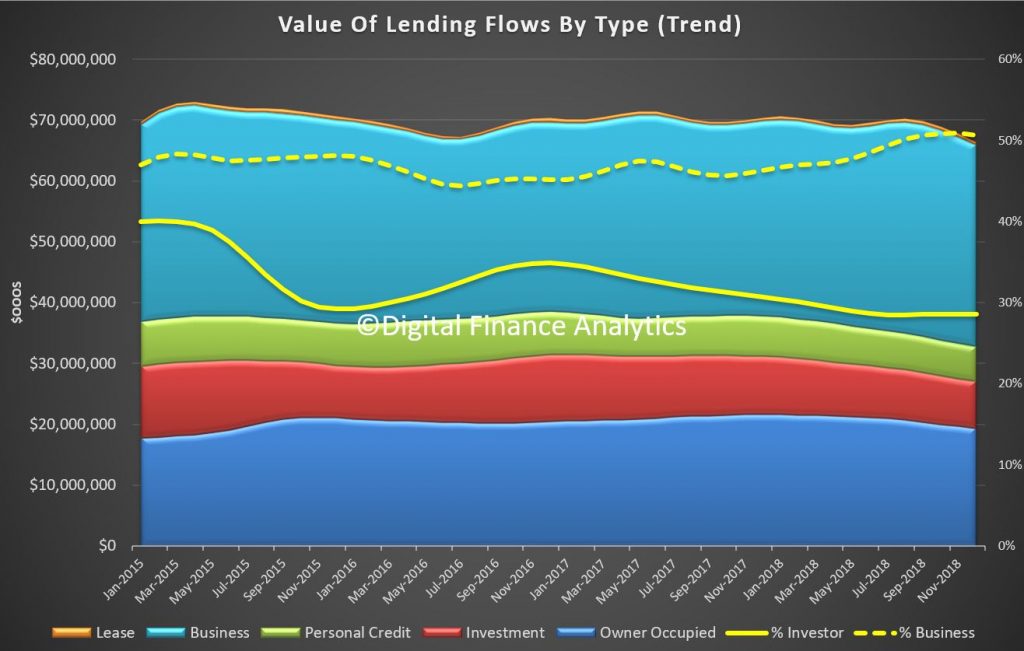

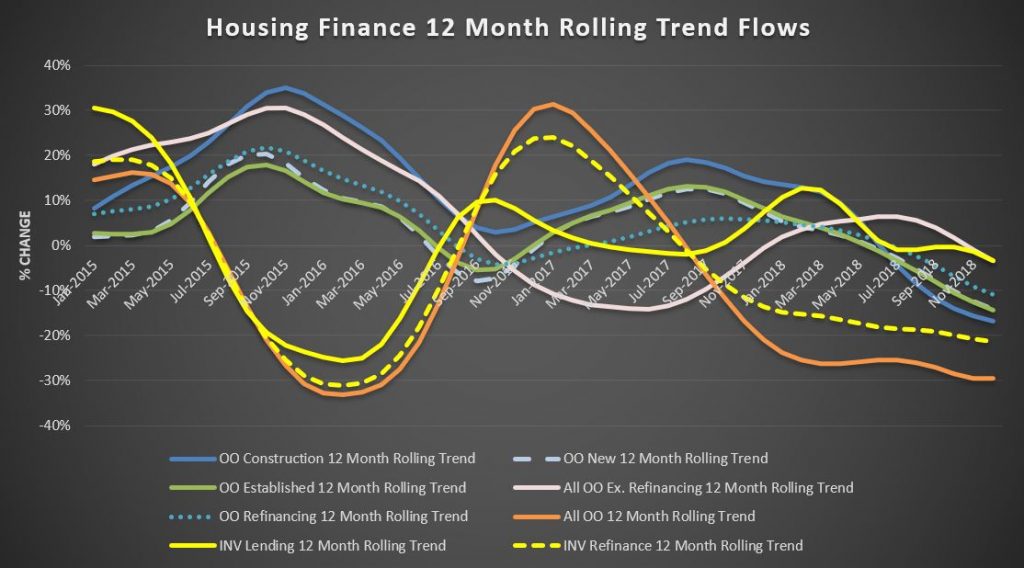

The ABS has released the first in its new combined series of household and business finance – “ 5601.0 – Lending to households and businesses, Australia, Dec 2018″.

The new data required a rebuild of our analytics, but it is very clear that the rate of growth of new credit continues to ease across the board. The focus of the release is credit flows, the rate of new loans being written. The RBA of course reports the stock at the economy level, and APRA the Bank (ADI) stock. Today we look at the flow data.

Owner Occupied lending flows fell by 1.59% from November to December, down $310 million dollars. Investment lending fell 1.6%, down $125 million dollars and personal credit fell 1.17%, down $68 million dollars. Total credit flows to households fell 1.52% down $506 million dollars. Business credit flows fell 2.55%, down $866 million dollars and total credit flows dropped 2.03% by $1.38 billion dollars, to $66.5 billion dollars.

The share of investment loan flows for residential property was 28.5% of housing flows, and lending for business fell to 50.6% of all credit flows.

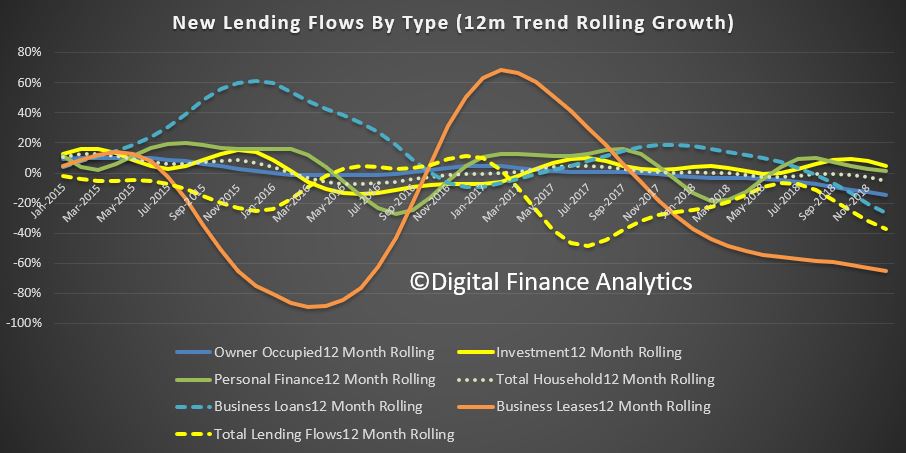

The credit impulse (the rate of change of credit growth) continues to ease, which signals a weaker economy, and lower home prices ahead. Significantly, owner occupied lending is slowing faster than investor lending now.

Within the housing categories the rolling 12 month growth rates in credit flows shows that owner occupied construction are down 16.7%, finance for new builds is down 14,2%, finance for established property is down 14.3% and refinanced loans is down 10.9% over 12 months. New investment loan flows fell 3.4% and refinanced investor loans was down 21.3%, which is a significant drop. These are the factors which feed into my overall home price models, and this downward momentum of the credit impulse is highly significant, and why I am looking for more home price falls ahead. Note again, its the owner occupied sector on the slide, not just property investors!

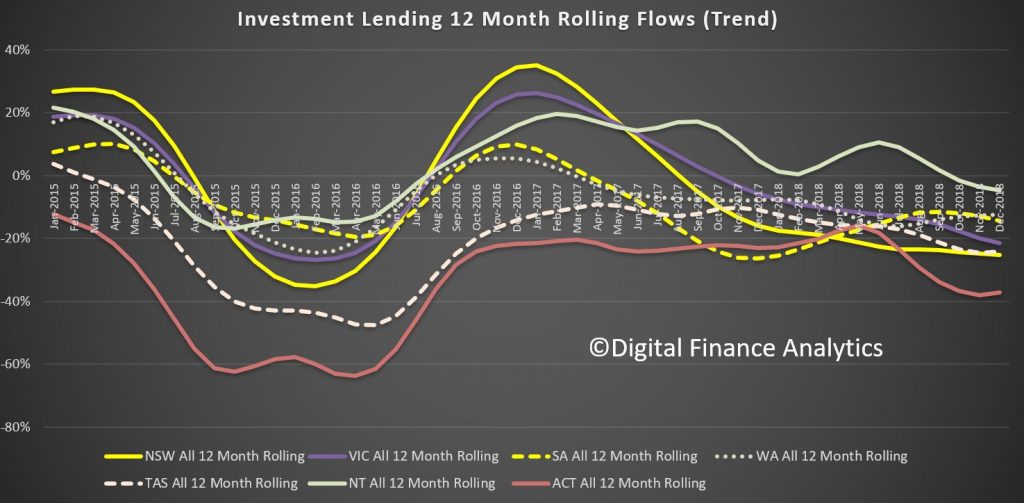

We can look at credit flows for investor purposes across the states. NSW is down more than 25%, VIC down 21.5%, SA down 14%, WA down 12% TAS down 24%, NT down 4.7% and ACT down a massive 37%; all over the past 12 months.

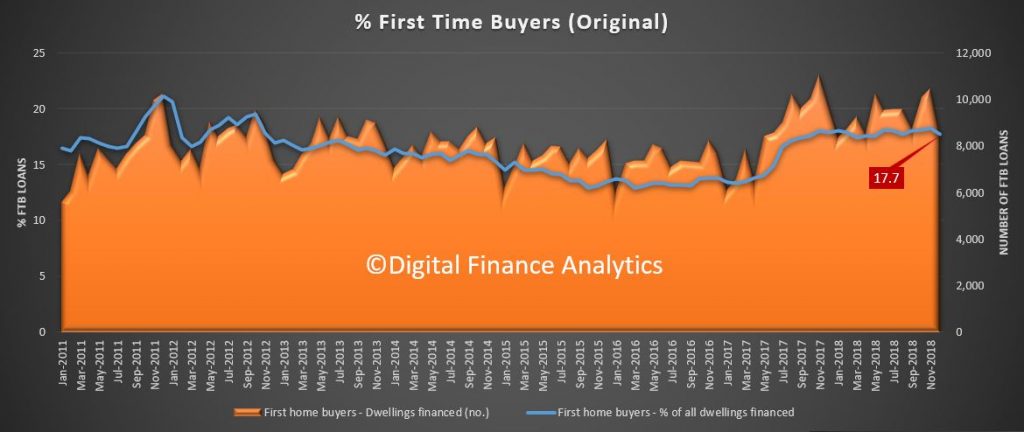

First time buyers continue at a lower rate as our tracker shows, with 17.7% of new loans for first time buyers, down from 18.3% last month, a drop of 1,976 transactions compared with last month, to 8,517.

In addition the number of first time property investor buyers dropped again.

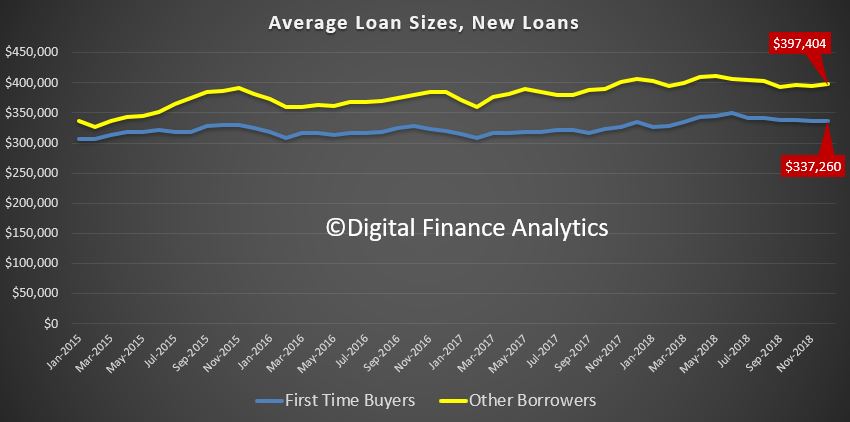

The average loan size for a first time buyer fell to $337,260, indicating tighter lending standards, while other loans were bigger at $397,404.

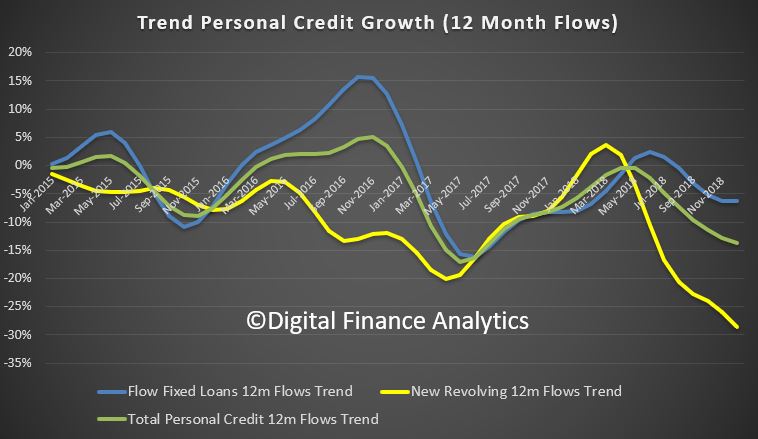

Finally, personal credit flows were down again, with new revolving loans especially hard hit.

In conclusion, there is nothing in this data to suggest increased momentum in credit, but then this is in December, and before the APRA statement that lending standards will remain tight (7% hurdle rate applies) and the Royal Commission left responsible lending rules where they were.

My conclusion is that the credit impulse will continue to slow. This will have a flow on effect to home prices and household consumption. The decade of credit driven expansion looks to be over for now. The problem is of course this will lead to weaker economic out-turns ahead, and falling home prices.

That said, credit is still growing unsustainably faster than income or inflation with housing credit at 4.9% growth over 12 month. But the rate of growth, as we showed here is easing back.

And I do not think the credit tap will be opened up “to 11” again anytime soon. Welcome to a new, but uncomfortable normal. One in which those with loans they should never have had in the first place continue to struggle with them, and new borrowers, should they chose to borrow, will need to jump through a whole series of higher hoops.

20-30% peak to trough falls in home prices anyone?

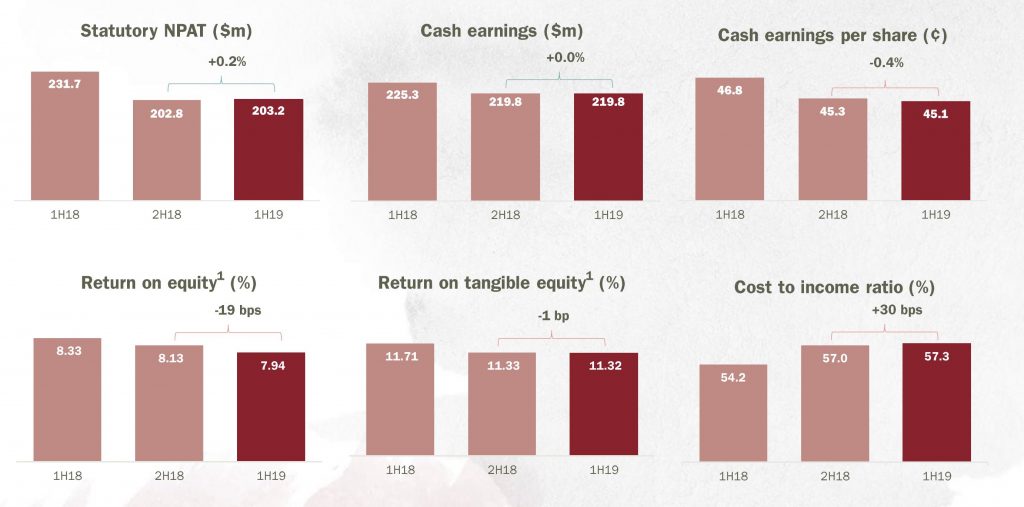

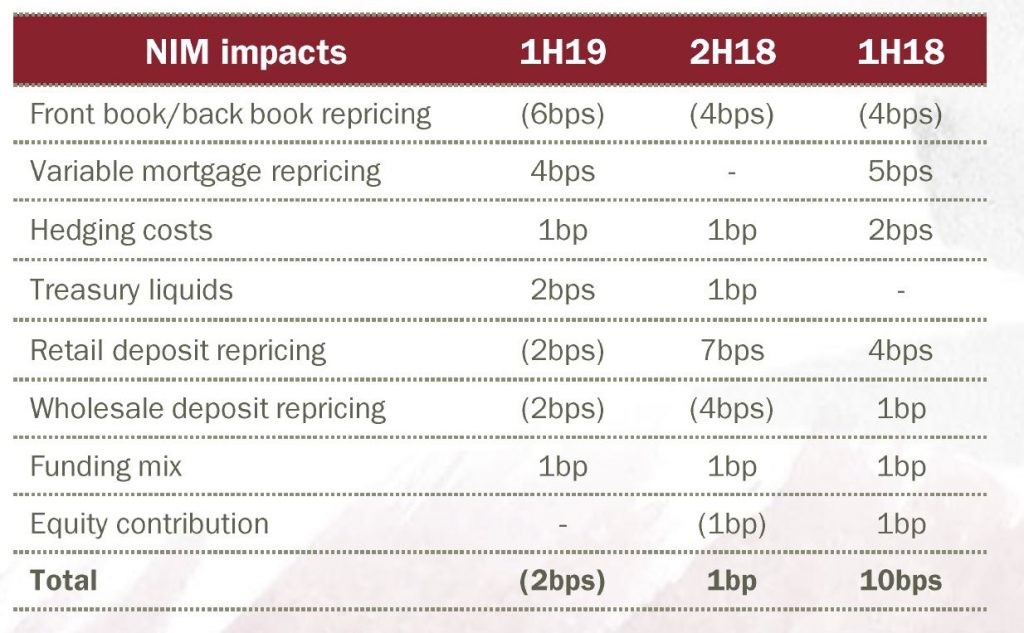

Yesterday Bendigo and Adelaide Bank released their results for the half year to December 2018. The after tax statutory profit was $203.2 million up 0.2% on the prior half, but significantly lower than the $231.7 million in 1H18. The cash earnings was flat at $219.8 million, but again lower than $225.3 million in 1H18. The earnings per share was 45.1 cents, down 0.2 cents and the fully franked dividend was 35 cents per share. The return on equity fell 19 basis point half on half.

They are positioning as “Australia’s fifth largest retail bank” and they saw a rise of 18% in new customers joining and according to research are the 9th most trusted brand in Australia. Have no doubt the franchise and “local” approach is attractive to some customers, but the question is, can the current formula work in the current tight margin, highly competitive market at a time when home loan momentum is falling. One signal is cost to income, which is rising – a reflection of the high touch model.

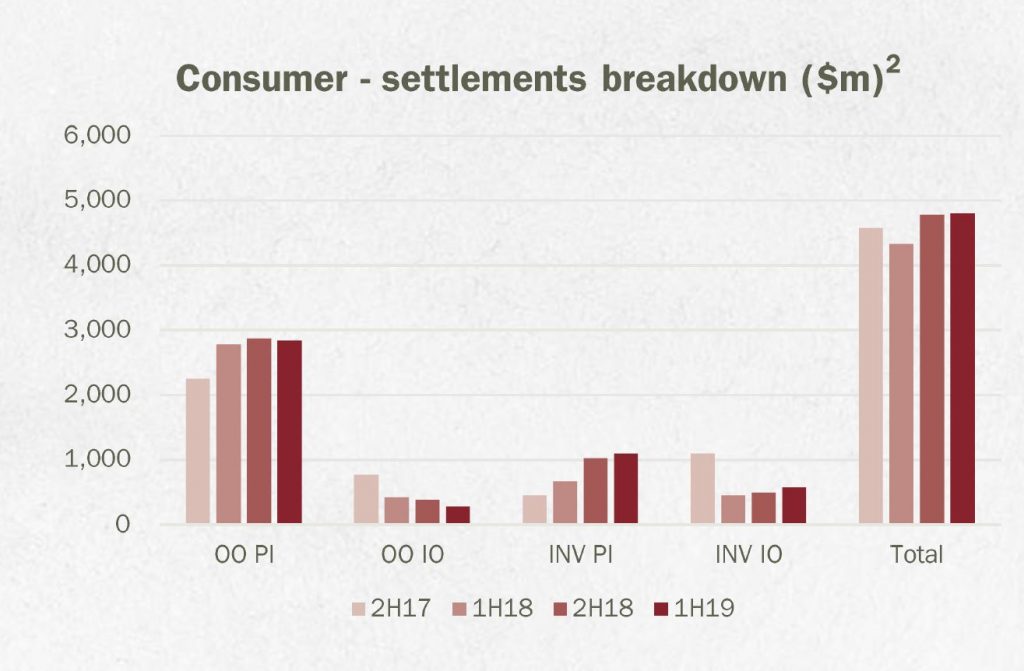

Mortgage book growth was 2.7%, compared with system growth of 3.3% with a portfolio of $23.1 billion. They saw more growth in investor loans than owner occupied loans.

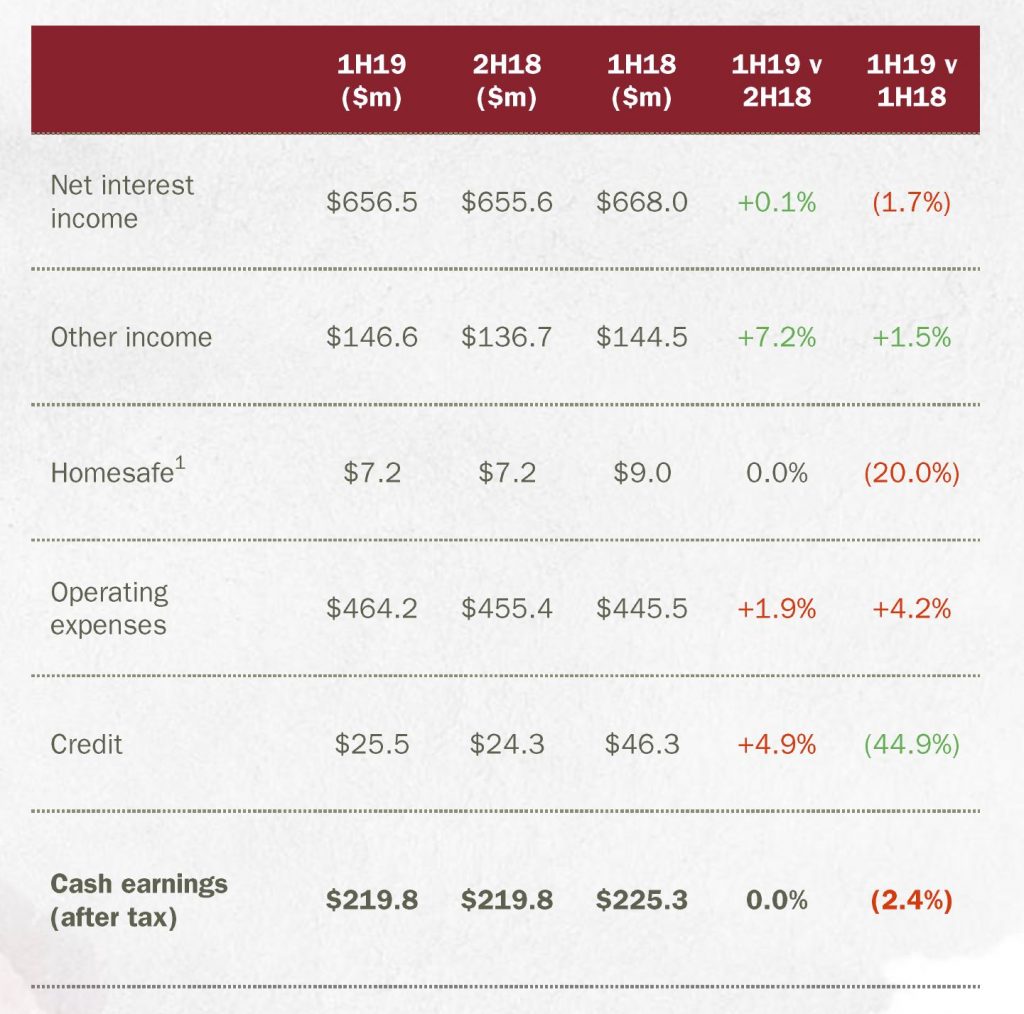

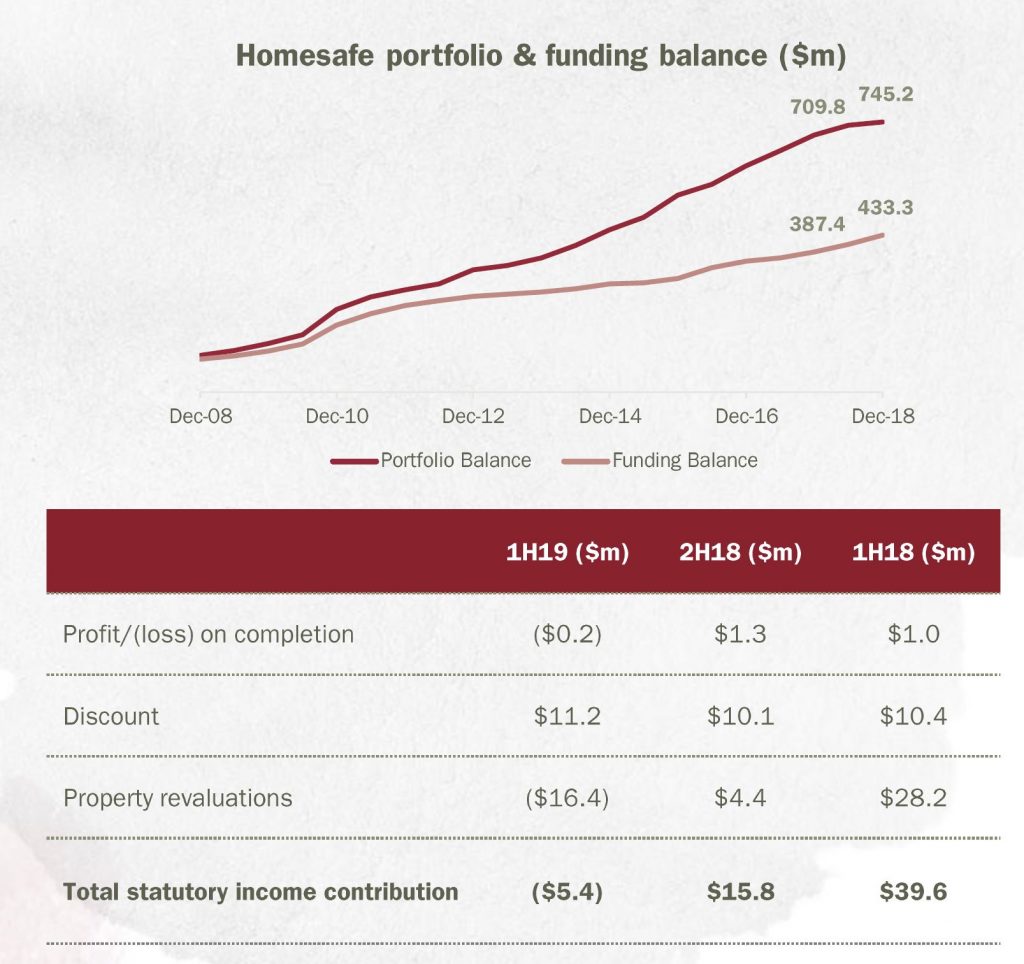

Earnings were support by other income (card activity and commissions on managed funds plus FX transactions), but net interest income was flat and Homesafe reflects changes to its accounting treatment.

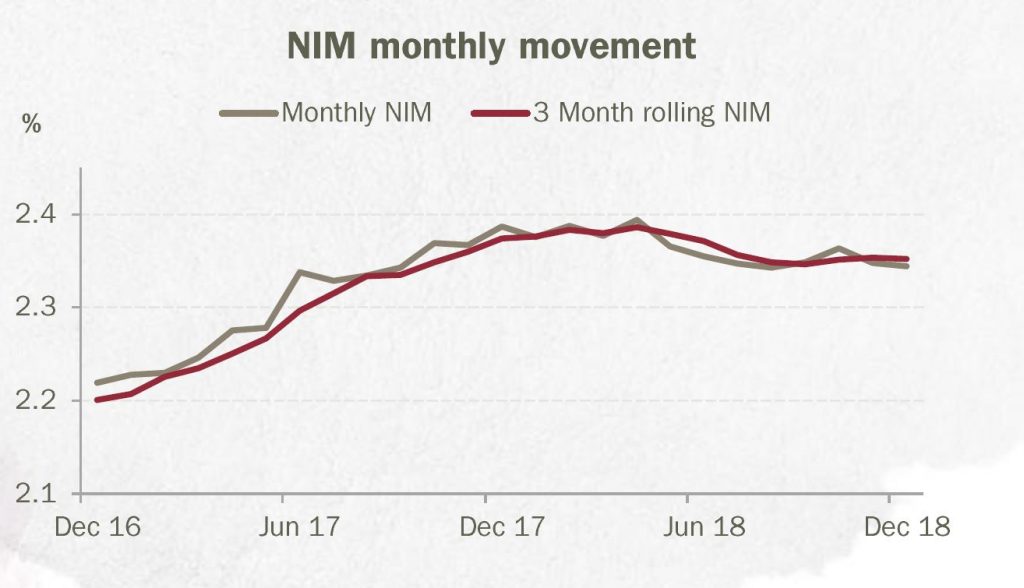

Net interest margin was down 2 basis points reflecting discounting for new loans, higher funding costs and deposit repricing.

The exit margin was 2.34% and will remain under pressure ahead.

Homesafe contribution was subject to a review of their portfolio valuation methodology, as a result they removed the overlay and revised down valuation growth rates to 0% in year 1, 3% year 2 and 4% year 3 and beyond. The result was a $1.9m change to the valuation. Essentially, they tweaked the property valuations lower (from 6% growth) but then changed the discount rate to mask the effect. A little sneaky! We said last year their home price projections were heroic… but there is still more downside risk here in our view.

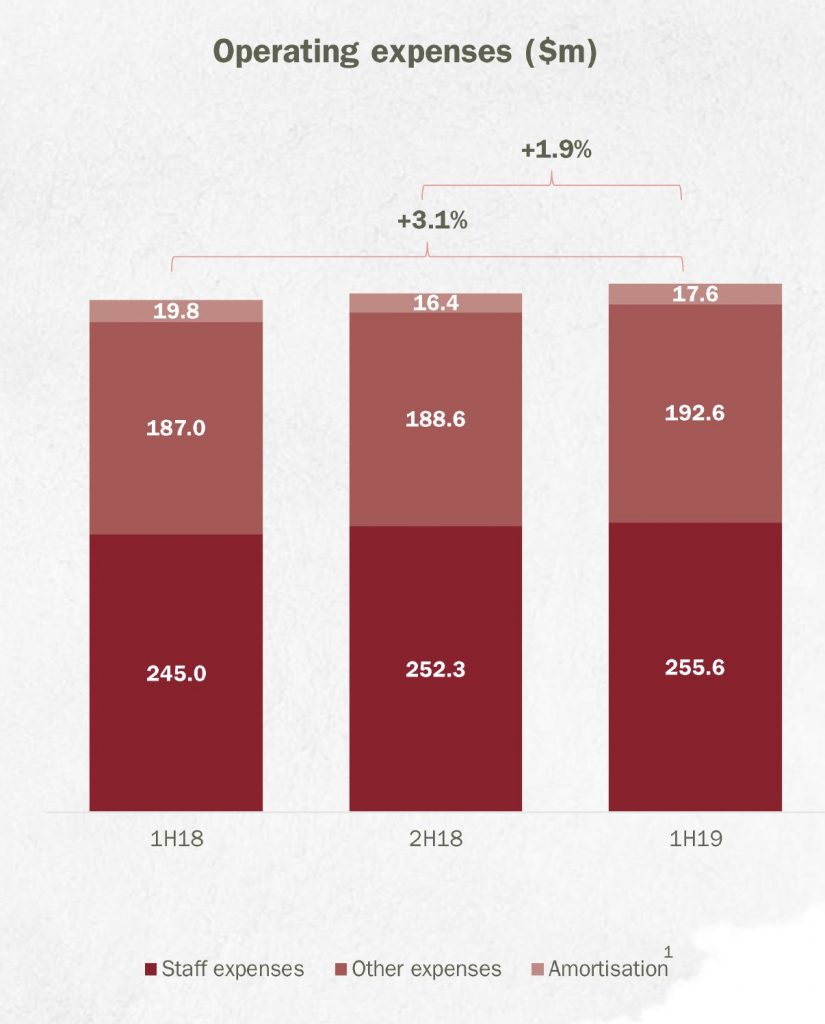

Their costs were higher, up 30 basis points to a cost income ratio of 57.3%, including higher staff costs, technology and legal and compliance.

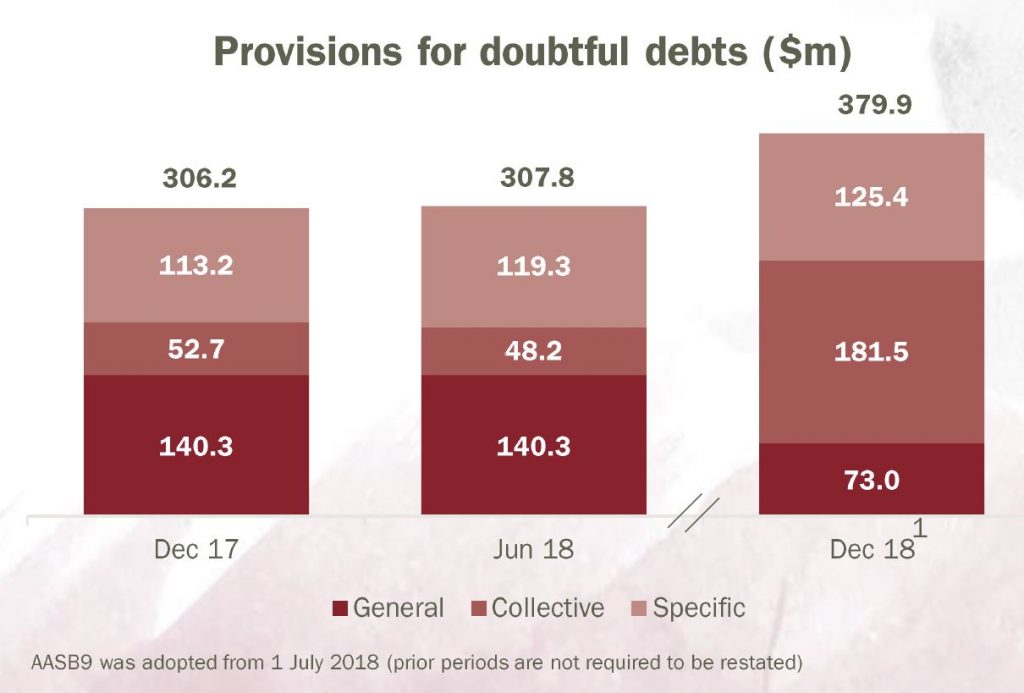

Along with the other banks, they continue to adjust their provisions to AASB9 which has lifted the collective provisions. It stands at 8 basis points, below the long term average.

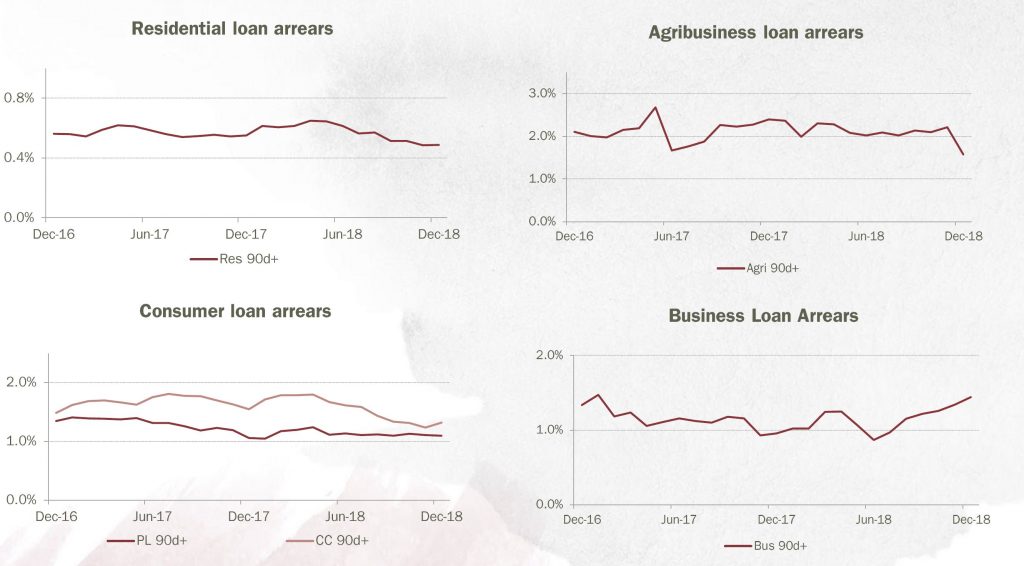

Arrears appears well contained at the moment. There was a small spike in 90 days plus credit card arrears, and business loans. Note though these figures EXCLUDE impaired loans over 90 days.

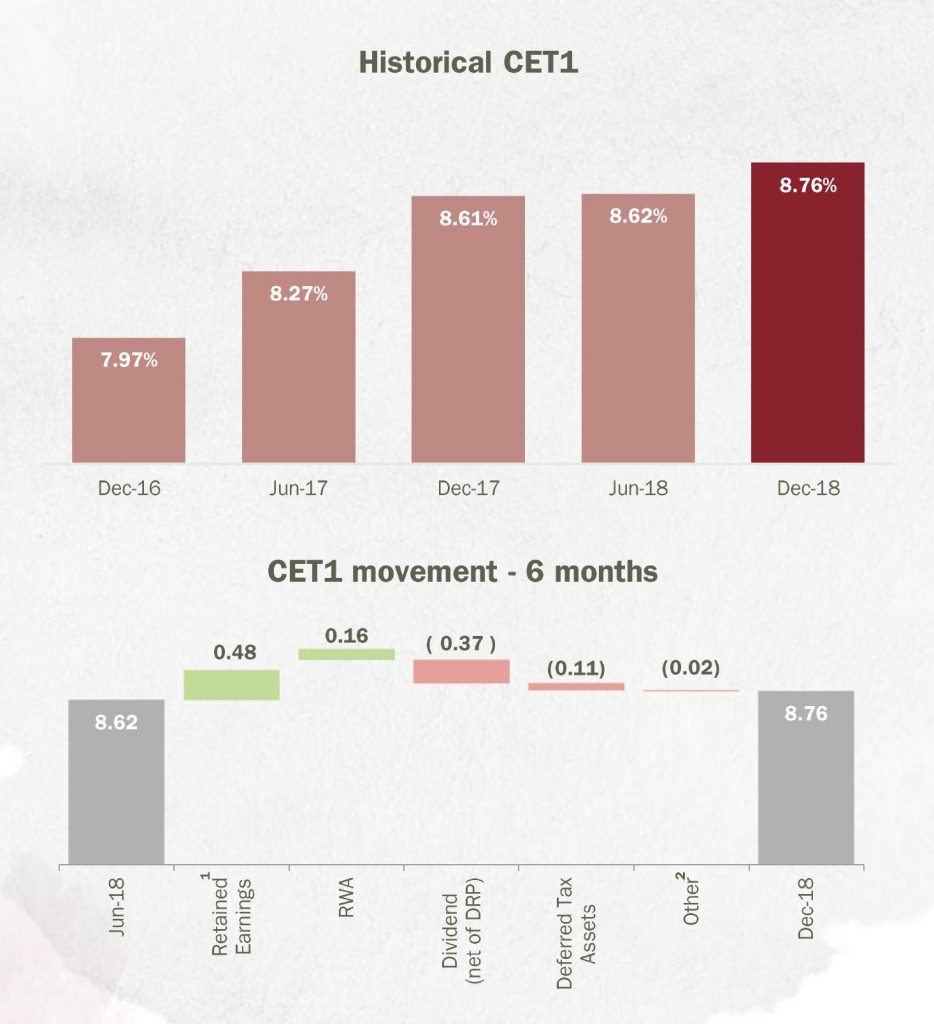

Capital position is 8.76% CET1, up 14 basis points. They are still working on advanced APRA accreditation (though the benefit looks increasing questionable in my view given APRA’s moves to lift the advanced ratios, relative to standard approaches.

Funding from deposits increased to 82.4% but they noted that higher BBSW impacted the cost of wholesale and securitisation funding.

So to conclude, we wonder about ongoing margin compression and the slowing housing sector and mortgage growth. Their cost base appears to contain significant fixed elements, which means they may have ongoing cost ratio issues. The benefit of advanced capital accreditation may be lower as APRA turns the screws. A tricky time for a player which gets the consumer, but has difficulty in competing in the current environment.

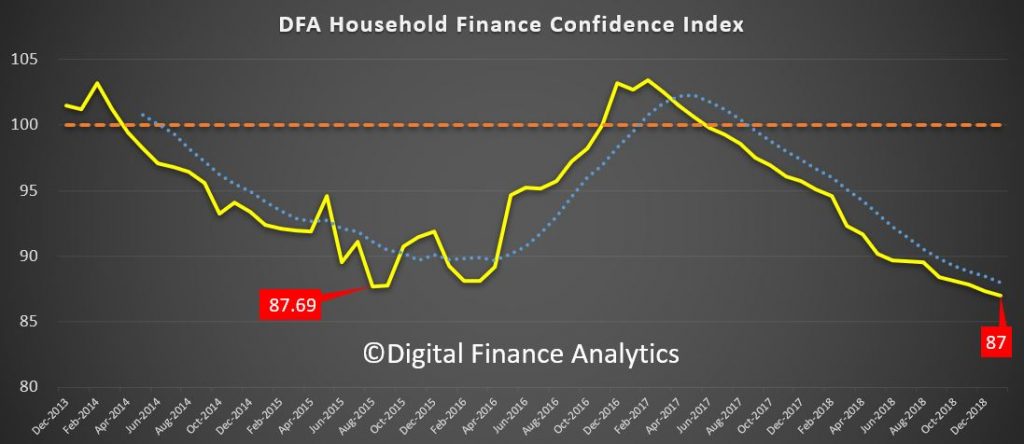

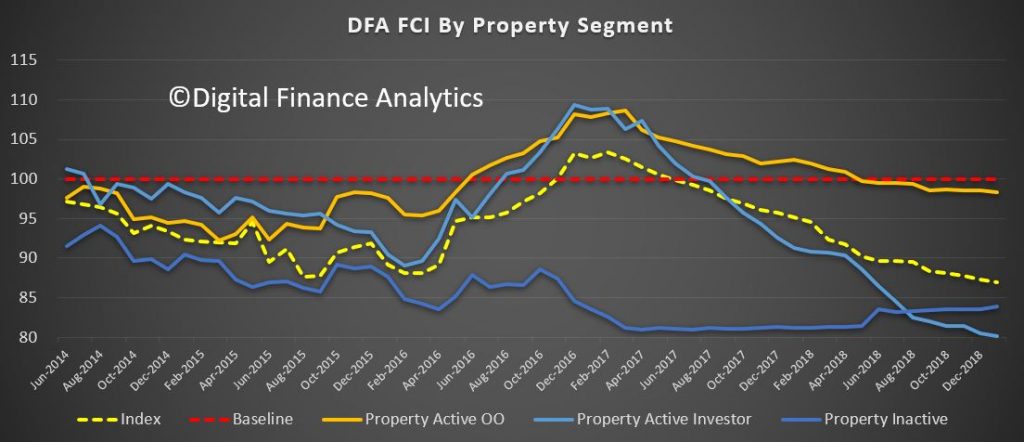

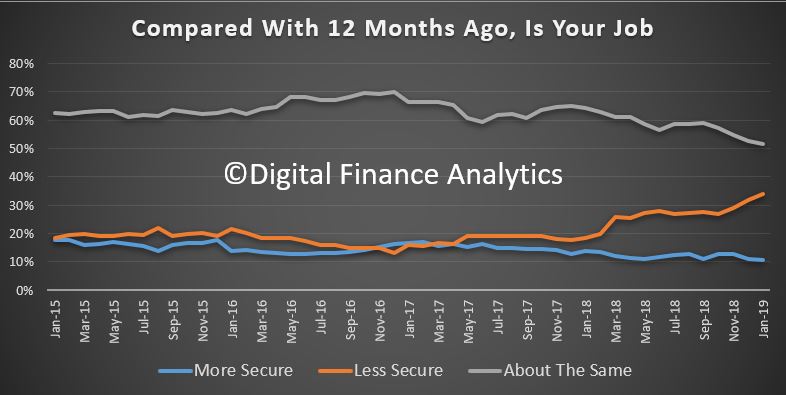

This is starting to look serious as the latest DFA household financial confidence index results for January 2019 reveals a further decline in levels of confidence.

The index fell to 87 in January, down from 87.3 in December, the lowest its been since the survey commenced, well below the neutral setting of 100.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

Looking at the results by property segments, we see a fall in confidence among property investors, as home prices and rental yields continue to fall, and reflecting concerns about potential changes to negative gearing and capital gains ahead. That said, purchase interest has risen a little. We will discuss this later.

Owner occupied borrowers are also feeling the heat, reflecting some mortgage price pain, as well as the basic affordability issues. Those renting however are a little more positive relatively speaking, thanks to rents being lower now and a greater choice of property for rent being available, especially in Sydney. Overall investors are the least confident now, a considerable switch from a year or so ago!

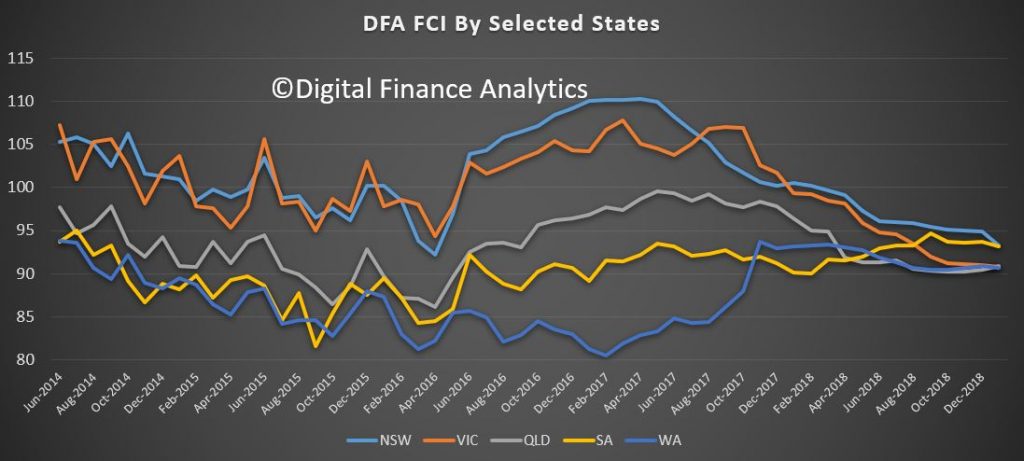

Cutting the data by states, we see that the bunching continues as property price falls in Sydney and Melbourne erode confidence there, relative to the other states. The most significant fall was in NSW, as home prices fall – and the fall out from Opal Tower had an impact more broadly on new purchases, and off the plan commitments.

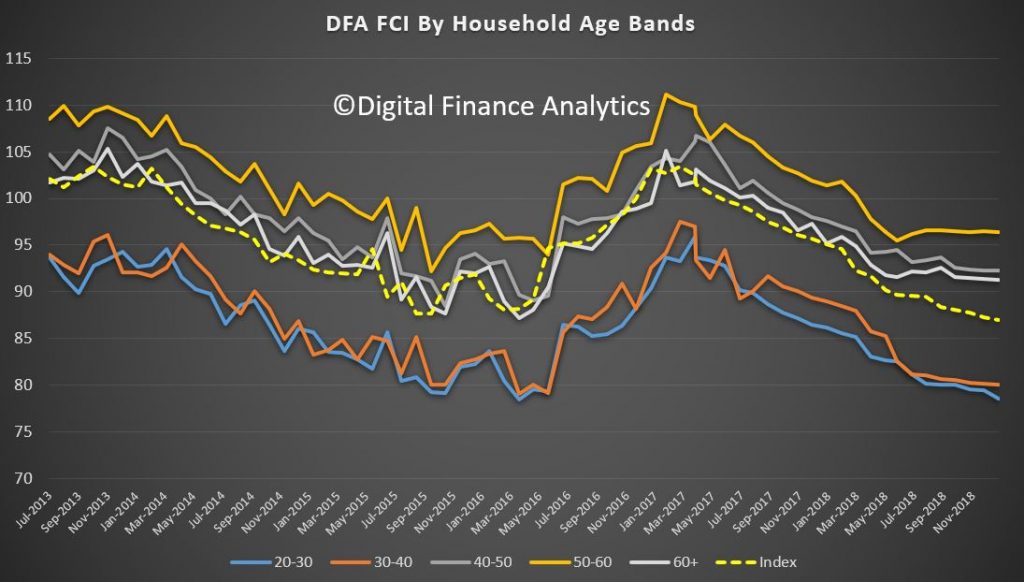

Across the age ranges we continue to see weakness, with younger households more exposed, although those older households with share market investments saw a rebound in January, which boosted their confidence a little.

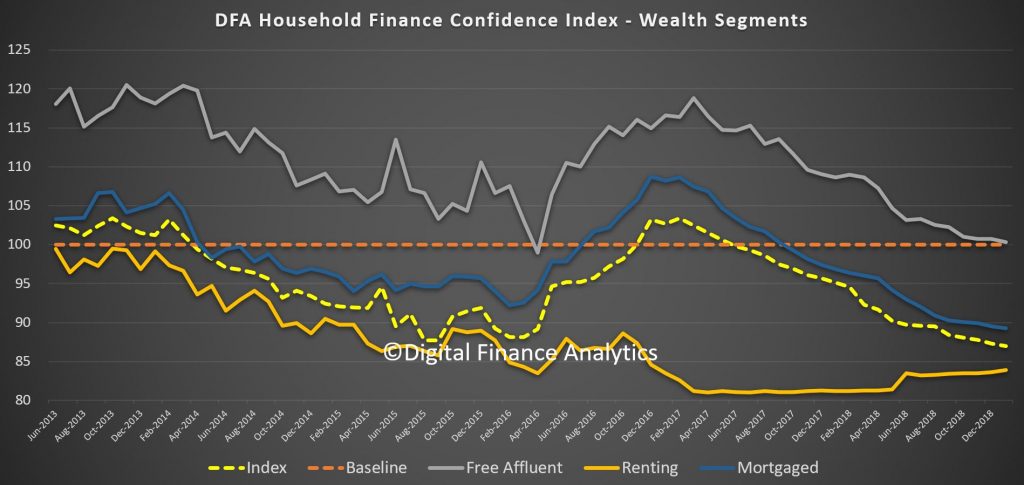

Turning to our wealth segments, we continue to see property owners without a mortgage the most confidence, though falling close to the long term neutral benchmark, while those with mortgages (either investor or owner occupied) continue to decline. Renters remain the least confident. This could become an important indicator in the run up to the next election, in that even those heartland voters supporting the incumbent Government are less positive than usual.

We can then examine the moving parts within the index. We start with job confidence. Those feeling more secure about their job prospects fell 2.19% to 10.57%, while those feeling less confident rose 4.84% to 33.85%. 51.68% saw no change, but that fell by 3.30%. There was a noticeable rise of concerns in the construction sector as building approval momentum falls.

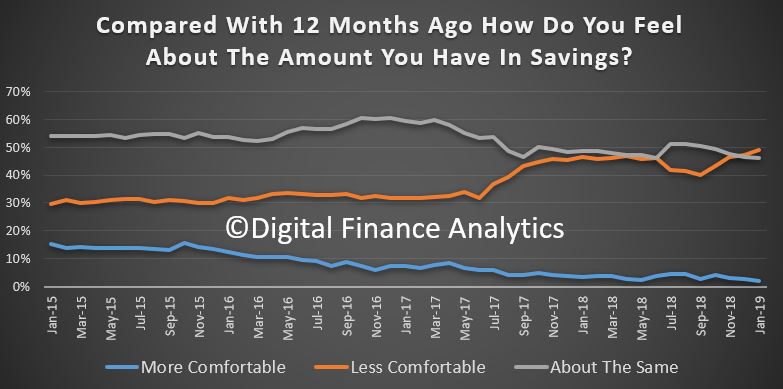

Savings rates continue to fall for many, and others are raiding what savings they have to maintain their lifestyles – something which of course cannot continue indefinably – one reason why the savings ratio continues to fall. June 1.98% of households were more comfortable than a year ago, down 1.28%, while 48.96% were less comfortable, a rise of 2.52%. 46.24% were about the same, down 1.56%.

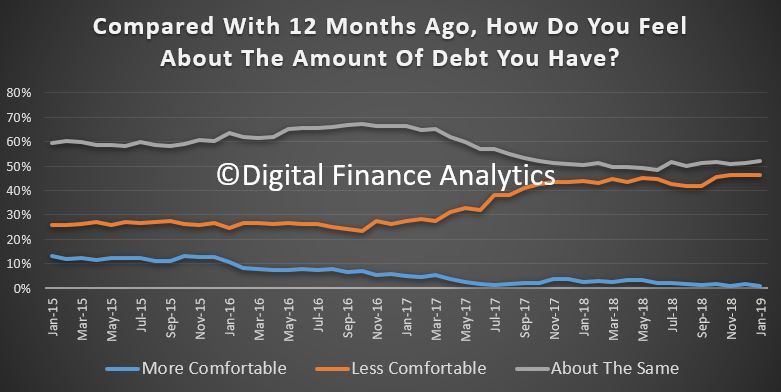

Turning to debt, 1.11% of households are more comfortable than a year ago, and 52% are about the same. 46% are less comfortable than a year back, thanks to rising rates, switches to interest and principal from interest only loans and problems in servicing the repayments. We also continue to see growth in quasi credit such as Afterpay, as well as other forms of short term credit. Household debt of course continues to rise faster than incomes or inflation.

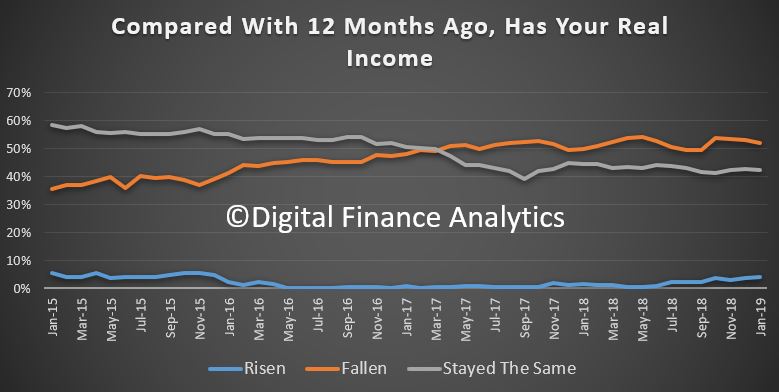

Income growth remains a real concern for many households (in real terms many have seen falls in recent years). 3.88% of households reported their real incomes had grown in the past year, 51.99% said incomes had fallen in real terms, and 42.5% said there had been no change. We continue to observe pressure on the income side of household balance sheets, despite the RBA’s expectation that wages will rise eventually. One bright spot was dividend payments which were higher, but this failed to offset the total picture.

One of the killer categories is the costs of living. Once again we think the CPI figures just do not reflect the lived experience of many households. 87.75% said their costs had risen over the past year, up 3.2%. This includes the old favorites, electricity, child care, health care, and household staples, despite a fall in costs of fuel at the bowser.

And finally, household net worth continues to take a dive thanks for falling home prices – this despite recent positive share price moves. Overall 32.18% of households sand their net worth had improved, down 1.82% from last month, 37.28% said their net worth had fallen, up 4.05% and 27.42% said there had been no change, down 2.52%.

One other interesting point which came out from the analysis is that potential property investors are more active now, thanks to the falls in asking prices, and importantly, the burning fuse with regards to ending negative gearing should Labor win the next election. Thus we have seen a rise in investors considering transacting. Some lenders are offering “special” fixed rate offers, in the light of APRA’s hands off approach, and of course Hayne did not do anything on responsible lending. The tighter underwriting standards are still in play of course – for now – but I would not bee surprise to see a kick up in new investor lending in the weeks ahead, despite the lower levels of financial confidence.

In summary then, interesting times as household finances are squeezed, yet the fixation on property for many Australians remains strong. There is still a belief that falls will be limited, and they will bounce back. We are not so sure!

We will update the index next month.

Treasurer Josh Frydenberg has offered support to Donald Trump’s pick for the World Bank Presidency.

David Malpass is currently Under Secretary of the United States Treasury with responsibility for International Affairs, and his previous experience includes being chief economist at Bear Stearns prior to their collapse.

Our Treasurers support is wrong headed.

No matter what the strengths of David Malpass, the next World Bank President should not be American.

After World War Two the victors designed many of our global institutions, including the World Bank, and the International Monetary Fund. Major global institutions were headquartered in Europe or the United States, and there was an agreement that the World Bank President would be a US citizen, while the IMF would be headed by a European.

This cosy arrangement was fine for most of the 20th century, but is at odds with our 21st century world.

It has been suggested that Trump would follow his usual negotiating tactics and withdraw support from the World Bank if the next chief is not American, which is presumably why some countries including Australia are likely to support Malpass.

The search for the US nomination was headed by Steven Mnuchin and Ivanka Trump, with Invanka Trump herself mentioned as a possible nomination.

Malpass may be a better candidate than the President’s daughter, but I doubt it.

Malpass has been a critic of World Bank lending to China and at Bear Stearns he ignored warning signs of crisis in 2007.

But it’s not so much Malpass’ dubious credibility that is the problem, but the idea that the President should always be American.

Important global institutions should be led by the best candidate. The views and expertise of emerging market candidates, particularly from larger economies such as China, India, Brazil, Nigeria and Indonesia should be taken more seriously.

In recent years the IMF would have been much better led by a non-European. The decision to bail out French and German banks at the expense of the Greek economy in 2012 was a poor decision made by the French head of the IMF.

The IMF rightly supported restructuring of banks and financial markets after the Asian Financial Crisis in 1997, but did not push for the same for European or US banks after 2008.

So what if Australia and other middle powers did not support Malpass’ nomination?

A US withdrawal from the World Bank would probably see its demise. But so what?

The World Bank has become relatively toothless.

Last year China lent more money to emerging market economies than the World Bank.

And this is the point. China needs to be brought into the World Bank and other institutions more fully, not sidelined.

Problems with governance and other issues with China’s Belt and Road initiative would be much better handled by a multilateral agency, whether that is a properly renewed World Bank or a new institution.

Author: Mark Crosby, Professor, Monash University

Joe and I discuss the latest data from New Zealand, and compare things with the Australian property story. Parallels abound!