Troubled wealth giant AMP has admitted it faces a long hard road to recovery. With an increasingly vigilant regulator, conduct remains its greatest risk, via InvestorDaily.

In

its annual report, released on Wednesday (20 March), AMP’s new chief

executive officer, Francesco De Ferrari, told shareholders that 2019

will be a transitional year for the company as it completes the sale of

its wealth protection business and continues work on its hefty

remediation program.

AMP’s 2018 results included a provision of

$430 million (post-tax) for potential advice remediation, inclusive of

program costs, in relation to ASIC reports 499 and 515, which require an

industrywide ‘look back’ of advice provided from 1 July 2008 and 1

January 2009, respectively.

“Our first priority is the separation

of our wealth protection and mature businesses, which will help simplify

and create the basis for a more agile AMP,” Mr De Ferrari said.

“Our

second priority is the delivery of our advice remediation program to

compensate impacted clients. We are focused on doing this as quickly as

possible. Lastly, AMP is focused on getting our risk, governance and

control settings right. This includes placing ethics and risk at the

core of our culture.”

Following the sale of the wealth protection and

mature businesses, AMP will have four core operating businesses – wealth

management in Australia and New Zealand, AMP Bank and AMP Capital.

“Our

wealth management business in Australia has foundational assets and

strong market positions. However, the business model is challenged and

we need to reshape it for the future,” the CEO said. What shape the new

AMP wealth business takes remains to be seen.

“In New Zealand,

our wealth management business continues to deliver resilient earnings

for the group. Our opportunity is to become an advice-led wealth

management business,” Mr De Ferrari said.

AMP Capital has a

strong growth trajectory, particularly internationally. AMP Bank has

performed well and can be further leveraged as part of our wealth

management offer.

In its director’s report, AMP provided extensive

commentary on the key risks to the company, which has faced significant

challenges throughout 2018.

“Given the nature of our business

environment, we continue to face challenges that could have an adverse

impact on the delivery of our strategy,” the company said, adding that

the most significant business challenges include business, employee and

business partner conduct.

“The conduct of financial institutions

is an area of significant focus. There is a risk that business practices

and management, staff or business partner behaviours may not deliver

the outcomes desired by AMP or meet the expectations of regulators and

customers” the company said.

“An actual or perceived shortcoming

in conduct by AMP or its business partners may undermine our reputation

and draw increased attention from regulators. Our code of conduct

outlines AMP’s expectations in relation to minimum standards of

behaviour and decision-making, including how we treat our employees,

customers, business partners and shareholders.”

We often get questions about how to navigate the current choppy financial waters. DFA does not provide financial advice, but we do invite people with different views to share them with our community.

To that end, on Monday March 25th at 12pm AEDT (Sydney) I will discussing the current state of play with Harry Dent.

Note that we are not being paid to send this invite, nor for our time. This is not a sponsored promotion. It is being offered as a service to our community.

During this one-off LIVE broadcast, you will discover:

Harry Dent’s latest research and what it reveals about our economic future, and why it’s SHOCKING!

Harry Dent’s 2 major predictions that could begin to take place as early as the next few months

How to shield yourself from financially devastating stock market and real estate losses by preparing before the carnage begins, so you can feel safe knowing your future

How to profit from specific “decline-related” investments year after year, over the next several years, so you won’t just survive a market crash, you’ll prosper from it…

How to create a “legacy of wealth” by snapping up nearly every investment you can think of, at fire sale prices, allowing you to make more money by spending less…

How to set yourself up for the next long-term “boom cycle”

I discuss the new Senate Inquiry into Banking Separation with Robbie Barwick from the CEC.

With three weeks before the closing date for submissions, now is the time to make that submission – we have the opportunity to drive much needed reform into the banking system.

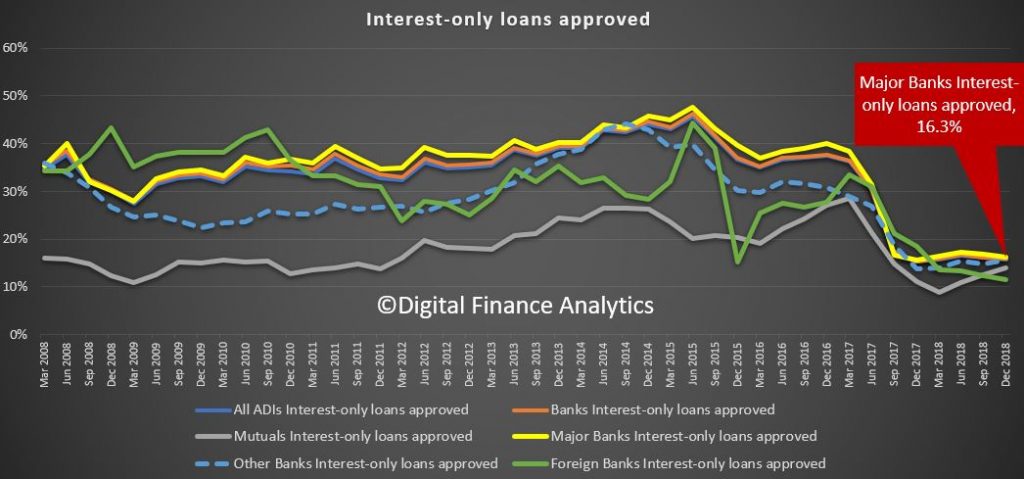

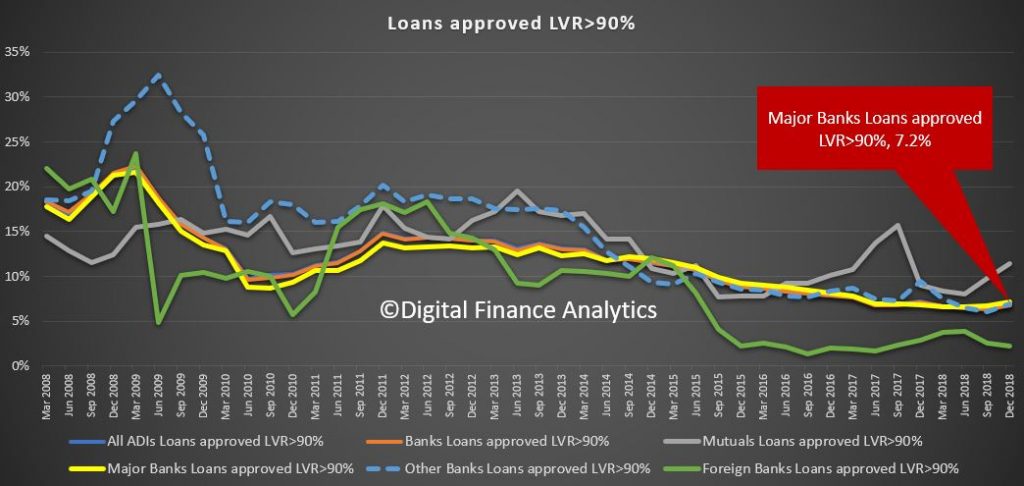

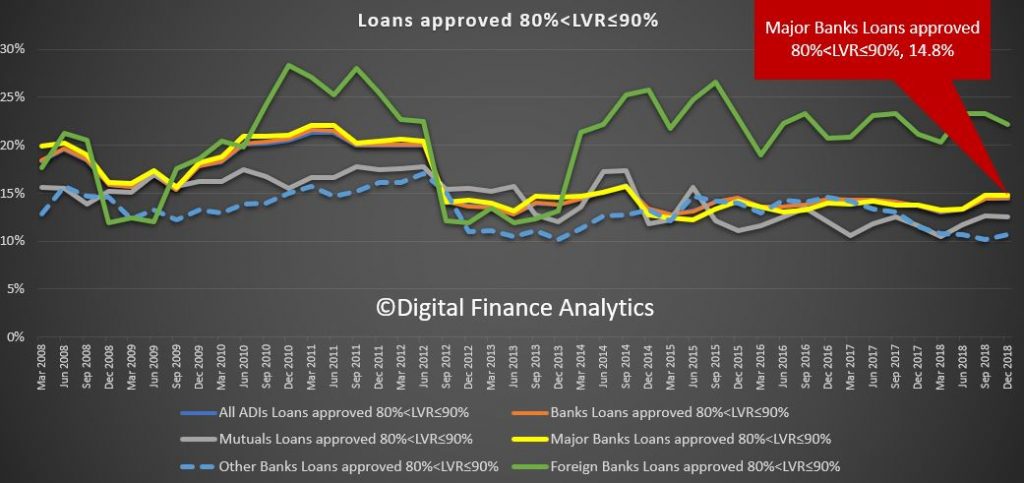

APRA released the latest quarterly property exposures data today to December 2018. The new loans flow data shows that owner occupied lending is still running at a pretty good clip, while new investor loans are sliding – and the share of all loans interest only, have dropped considerably.

The mapping between investment loans and interest only loans is probably more than coincidence, as we know the bulk of IO loans are for investors, but APRA does not [conveniently?] split them apart.

We can look at IO loan approvals by lender type. Major banks had 16.3% of their loans interest only, well down from their peak of 40%.

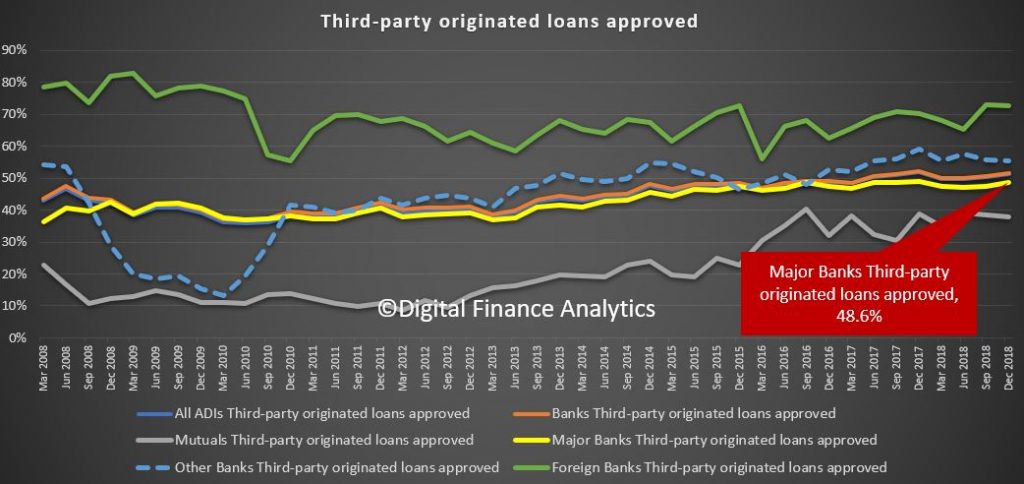

Mortgage brokers are still originating a significant share of new loans (even if volumes are lower). Foreign banks have the largest share via brokers, the majors are at 48.6%.

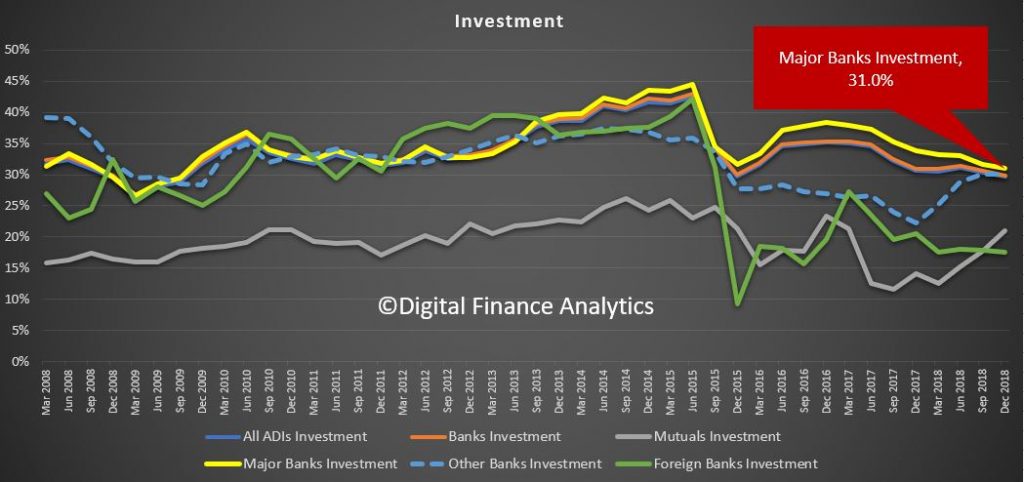

The proportion of investor loans being written has fallen, with major banks writing about 31% for investment purposes. Still a big number!

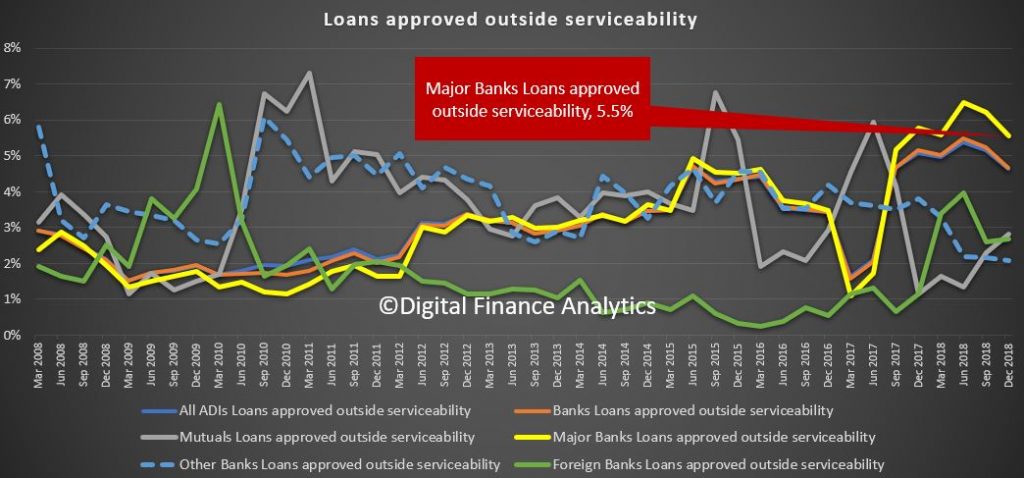

Loans outside serviceability are still high, reflecting tighter standards. Major banks are at 5.5% outside serviceability, down a little from past couple of quarters, but still a significant issue. Tighten the rules, then break the rules!

Finally, we can look at high LVR lending, important seeing as in some areas of Sydney prices are now down more then 20%. Over 90% LVR loans are still being written – 7.2% of all loans by major banks (so if prices fall another 10% ALL of these will be in negative equity. Also the trend is higher, especially for mutuals.

And the 80-90% LVRs are at 14.8% of all new loans from the major banks. Foreign banks are higher.

So a further fall of 20% would put more than 22% of new loans underwater.

These results suggest the banks are still lending excessively in the current environment. Expect more trouble ahead.

Just before the GFC hit, the then Chair of the Fed reassured that everything was going to be fine.

The subprime mess is grave but largely contained, said Federal Reserve Chairman Ben Bernanke Thursday, in a speech before the Federal Reserve Bank of Chicago. While rising delinquencies and foreclosures will continue to weigh heavily on the housing market this year, it will not cripple the U.S. economy, he said. The speech was the Chairmans most comprehensive on the subprime mortgage issue to date.

It of course was not. We are still reaping the QE whirlwind.

So, today, RBA Assistant Governor (Financial System) Michele Bullock spoke in Perth “Property, Debt and Financial Stability”. In Perth, of all places where prices have been falling for many years!

She concludes that “vulnerabilities from the level of household debt, the apartment development cycle and the level of non-residential commercial property valuations continue to present risks for financial stability. While so far, the financial sector has remained resilient, we continue to monitor developments in household debt and in property markets for signs that these might have more broad ranging effects on the financial system”.

As Assistant Governor (Financial System) I oversee the Bank’s work on financial stability.

But what is financial stability and what is the Reserve Bank’s role in it?

The wellbeing of households and businesses in Australia depends on growth in the Australian

economy. And a crucial facilitator of sustained growth is credit – flows of funds from

people who are saving to people who are investing. Credit provides households and businesses

with the ability to borrow on the back of future expected income to finance large outlays, for

example, the purchase of a home or equipment to establish or grow a business. A strong and

stable financial system is important for this flow of funds.

There is no universal definition of financial stability but one way to think about it is to

consider what is meant by financial instability. My colleague Luci Ellis suggested

that this is best thought of as a disruption in the financial sector so severe that it

materially harms the real economy.[1]

This leaves unsaid where the disruption might come from, but we would all recognise the outcomes

of financial stability when we see it. For example, while Australia was spared the worst impact

of the global financial crisis, internationally it demonstrated the impact that financial

instability can have on growth and hence the wellbeing of households and businesses in the

economy.

Most of you will know about the Reserve Bank’s role in conducting monetary policy. But

another key role of the Reserve Bank that you might be less familiar with is promoting financial

stability. In this area, we share responsibility with the Australian Prudential Regulation

Authority (APRA). But it is APRA that has responsibility for the stability of individual

financial institutions and the tools that go along with that. So how does the Bank contribute to

financial stability?[2]

There are a number of things we do. We undertake analysis of the economy and the financial system

through the lens of financial stability, looking for financial vulnerabilities that could result

in substantial negative impacts on the economy, or economic vulnerabilities that could result in

risks to financial stability. We work with other regulators to identify signs of increasing

risks in the financial system and measures to address these risks. Where appropriate, we provide

advice to government on the potential implications for financial stability of policies. And we

talk about the risks we are seeing to help inform other regulators, participants in the

financial system, businesses and the general public of the potential risks that might have an

impact on the economy.

This last action – communicating the risks – is the key purpose of our six-monthly

Financial Stability Review (the Review). While any individual

financial institution, business or household might think the risks they are taking on are

appropriate, they may not be adequately taking into account the risks that are arising at a

systemic level from everyone’s actions. The Review attempts to bring this

system-wide view.

Our most recent Review was published in October last year and we are currently in

the process of drafting the next one, which will come out in April. So, for the remainder of my

talk, I am going to cover some of the key risks that we see at the moment. Given the audience, I

am going to focus on risks related to residential and commercial property. First, I will give an

update on recent developments in these areas. Then I will talk a little about recent concerns

around tighter lending standards. And I will finish up with a few observations on the property

market in Western Australia.

Household Debt

Six months ago in the Review, we noted that global economic and financial conditions

were generally positive and that the Australian economy was improving. At the same time, housing

prices were declining. In this context, we highlighted a number of vulnerabilities –

issues that, were a shock to occur or economic conditions take a turn for the worse, could

manifest in a threat to financial stability. At that time, we highlighted two domestic

vulnerabilities that are relevant to my talk today – the level of household debt, and the

slowdown in housing and credit markets. Six months on, these vulnerabilities remain. If

anything, they are a little more heightened.

The Bank has highlighted the issue of household debt as a potential threat to financial stability

many times over the past few years. Although it does not capture all the important information

about household indebtedness, the ratio of household debt to disposable income is one summary

indicator. This ratio is historically high (Graph 1). The household debt-to-income ratio rose

from around 70 per cent at the beginning of the 1990s to around 160 per cent

at the time of the GFC. The ratio steadied for a few years before starting to rise again around

2013 (around the same time that housing price growth began to accelerate) and is now around 190 per cent.

Graph 1

I have talked previously about some of the reasons why the debt-to-income ratio has risen so much

over the past few decades.[3]

In particular, a structural decline in the level of nominal interest rates and deregulation have

eased credit constraints and increased loan serviceability. And as households have been able to

borrow more, they have been able to pay more for housing. One important driver of high household

debt in Australia is, therefore, housing. There is very little debt related to non-housing loans

such as credit cards or car loans.

Just as housing costs have been an important driver of household debt, so has the ability to

borrow more influenced the price of housing. Over the past decade, housing prices in many parts

of Australia have risen but the rise has been particularly sharp in Sydney and Melbourne, which

account for around 40 per cent of the housing stock (Graph 2). More recently, housing

prices have fallen. Since the peak in mid 2017, housing prices Australia-wide have declined by

around 7 per cent. The falls in Sydney and Melbourne have been larger. The question we

are asking ourselves is, given the high levels of debt and falling housing prices, are there any

significant implications for financial stability?

Graph 2

The answer would be no at this stage – the impacts are not large enough to result in

widespread problems in the financial sector. This is not to downplay the financial stress that

some households are experiencing. But most of the debt remains well secured against property,

even with the decline in housing prices. Total repayments as a share of income remain steady and

a large number of indebted households have built up substantial prepayments over the past few

years. Broadly, the debt is held by households that can afford to service it. Arrears rates,

while increasing a bit over the past few years, remain low. Banks are well capitalised and work

over recent years to improve lending standards has made household and bank balance sheets more

resilient. Loans at high loan-to-valuation (LVR) ratios and interest-only loans are less common

than they were and most households have not been borrowing the maximum amount available.

Apartment Development

One area that we have focused on in recent years in our analysis of financial stability risks is

apartment development. There has been a substantial increase in apartment construction since the

start of the decade in the largest Australian capital cities (Graph 3). In Sydney there have

been more than 80,000 apartments completed over the past few years adding roughly 5 per cent

to housing stock in Sydney. Melbourne and Brisbane have also seen relatively large additions to

the supply of apartments and, while the number of apartments being built in Perth has been small

by comparison, this has been in the context of a fairly small apartment stock.

Graph 3

Our main concern with this from a financial stability perspective is the potential for this large

influx of supply to exacerbate declines in housing prices and so adversely impact households’

and developers’ financial positions. By its nature, high-density development can tend to

exacerbate price cycles. Large apartment developments have longer planning and development

processes than detached housing. Purchasing the land, designing the development, getting

approvals through relevant government bodies and then actual construction of the apartment block

all take time. In a climate of rapidly rising prices, developers are willing to pay high prices

for land on which to build apartments. Households, including investors, are willing to purchase

apartments off the plan, confident that the apartment will be worth more than they paid for it

when it is finally completed. This continues as long as prices are rising. This large increase

in supply, however, ultimately sows the seeds of a decline in prices which, if large enough,

results in development becoming unattractive, new supply falling and the cycle starting again.

This presents two risks. The first is to household balance sheets. A decline in apartment prices

could negatively impact households that purchased off the plan and are yet to settle. They might

find themselves in a situation where the value of the apartment in the current environment is

less than they contracted to pay for it. And as market pricing falls, lenders will revise their

valuations down and so will be willing to lend less. Households will therefore have to

contribute more funds, either from their own savings or loans from other sources.

The second risk is to developers who are delivering completed apartments into the cooling market.

If people who had pre-purchased are having difficulty getting finance, or decide it is not worth

going ahead with the purchase, there would be increasing settlement failures. Developers would

be left holding completed apartments, reducing their cash flow and their ability to service

their loans, and impacting banks’ balance sheets.

Currently, the risks here appear to be elevated but contained. The apartment market is quite soft

in Sydney; apartment prices have declined since their peak, rental vacancies have risen and

rents are falling (Graph 4). In Melbourne and Brisbane, however, apartment prices have so far

held up. Liaison suggests that settlement failures have not increased much and, to the extent

that they have, some developers are in a position where they can choose to hold and rent unsold

apartments. Further tightening in lending standards might, however, impact both purchasers of

new apartments and developers – I will return to this in a minute.

Graph 4

Commercial Property

A final area worth touching on is non-residential commercial property.

Commercial property valuations have, like housing, risen substantially over the past decade, and

much more than rents so that yields on commercial property have fallen to very low levels

historically (Graph 5). This is particularly the case for office and industrial property. One

reason for this is that yields, although they have been historically low in Australia, are high

relative to overseas and to returns on other assets. Furthermore, some markets, such as the

Sydney and Melbourne office property markets, are experiencing strong tenant demand and vacancy

rates are low. But the rapid increase in commercial property prices over the past decade does

pose risks. If transaction prices and valuations were to fall sharply, for example, in response

to a change in risk preferences, highly leveraged borrowers could be vulnerable to breaching

their LVR covenants on bank debt. This could trigger property sales and further price falls,

exacerbating the cycle.

Graph 5

Lending Standards

With that background, I want to turn to an issue that has attracted a fair bit of attention in

recent months – the role that tightening lending standards might have played in the

downturn in credit and the housing market. We published a special chapter in the October 2018

Review on this issue and the Deputy Governor discussed it in a speech in November

last year so I will only cover it briefly here.[4]

Lending standards have been tightening since late 2014, well before housing prices in the eastern

states started to turn down. The initial tightening occurred in December 2014 in response to

very fast growth in lending to housing investors and an assessment by APRA that banks’

lending practices could be improved. APRA required banks to tighten their lending practices in a

number of areas, including interest rate buffers, verification of borrower income and expenses,

and high LVR lending. The measure that got the most attention at that time, however, was

the ‘investor lending benchmark’ in which APRA indicated that supervisors would be

paying particular attention to any institutions with annual investor credit growth exceeding 10 per cent.

The idea was that it would be temporary while APRA worked with the banks on addressing lending

standards.

The benchmark and the tightening of standards didn’t have an immediate impact on the pace of

investor lending. It didn’t really start to bite until the middle of 2015 when banks

introduced higher interest rates for loans to investors. And at that point, growth in lending to

investors slowed sharply (Graph 6).

Graph 6

Once things settled down, however, and banks were comfortable that they were well below the

benchmark, the growth in lending to investors started to pick up again. Then, in March 2017,

APRA introduced restrictions on the share of new interest-only lending as part of its broader

suite of measures to strengthen lending practices. As part of this, APRA reinforced its investor

benchmark. While the interest-only measure was focused on reducing the volume of higher-risk

lending rather than lending to a particular type of borrower, there was a noticeable impact on

the growth in lending to housing investors since interest-only loans tend to be the product of

choice for many investors.

Both the investor lending benchmark and the interest-only lending benchmark have been removed for

banks that have provided assurances on their lending policies and practices to APRA. But the

improvements in lending practices implemented by the banks over the past few years have resulted

in credit conditions being tighter than they were a few years ago. Application processes have

been taking a bit longer as lenders are being more diligent about verifying borrower income and

expenses, borrowers are generally being offered smaller maximum loans and some borrowers are

finding it more difficult to obtain a loan. Banks are more closely adhering to their lending

policies, resulting in fewer exceptions being granted and there are fewer high LVR and

interest-only loans being approved.

There have been some concerns expressed that these developments have been a key reason for the

slowing in credit growth over the past year. Coupled with possibly some increased risk aversion

of front-line lending staff in the wake of the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry, the concern is that this has been impacting

housing credit growth and, by extension, housing prices. As concluded in the Banks’ February

Statement on Monetary Policy, and noted by the Governor in a recent speech, tighter

credit conditions do not appear to be the main reason for declining housing credit growth.[5] The evidence

points towards declining demand for housing credit as being a more important factor.

Nevertheless, it is possible that tighter lending standards could be impacting developers of

apartments. This could be direct, reflecting banks’ desire to reduce their exposure to the

property market, particularly high-density development. But it could also be indirect by banks

tightening their lending standards for purchases of new apartments, hence impacting pre-sales

for developers and their ability to obtain finance. The Deputy Governor noted this in a speech

in November 2018 and concluded that this was of potentially higher risk to the economy than

household lending standards.

From a financial stability perspective, prudent lending standards are a good thing. They ensure

that households and banks are resilient to changes in circumstances. But there needs to be a

balance. The regulators are not proposing any further tightening in lending standards. And the

appropriate amount of credit risk is not zero – banks need to continue to lend and that

will inevitably involve some credit losses.

Western Australia

Finally, I want to turn my focus to developments in Western

Australia. As you will have seen from some of my earlier graphs, the Western Australian

circumstances are somewhat different to those of the eastern capital cities. There are two

aspects I would like to focus on – household resilience and the commercial property

sector.

Housing prices in Perth have been declining for some years (Graph 7). The peak in housing prices

in Perth was in the middle of 2014. This followed a period of strong housing price growth as the

population of Western Australia increased strongly during the mining investment boom and housing

construction took longer to ramp up. When housing construction did respond, however, population

growth had slowed markedly and housing prices started to fall. Median housing prices have fallen

by around 12 per cent since 2014.

Graph 7

This has clearly been a difficult time for many homeowners in Western Australia. There are some

households that are having difficulty meeting repayments, as evidenced by a rising arrears rate

in Western Australia (Graph 8). At this stage, however, the losses are not large enough to

threaten the stability of the financial sector. We nevertheless continue to monitor the

situation for any potential systemic impacts.

Graph 8

Finally, office property in Western Australia has also been experiencing oversupply. Valuations

have fallen over the past decade (Graph 9). Rents have also fallen reflecting a sharp increase

in office vacancy rates in Perth’s CBD over the past few years (Graph 10). This makes for a

challenging environment for owners of these buildings, particularly for owners of older or lower

quality office buildings as tenants have taken the opportunity to move into newer buildings as

rents have come down. But again, while a difficult time for developers and owners of office

buildings, the financial stability implications seem limited.

Graph 9

Graph 10

Conclusion

Vulnerabilities from the level of household debt, the apartment development cycle and the level

of non-residential commercial property valuations continue to present risks for financial

stability. While so far, the financial sector has remained resilient, we continue to monitor

developments in household debt and in property markets for signs that these might have more

broad ranging effects on the financial system.

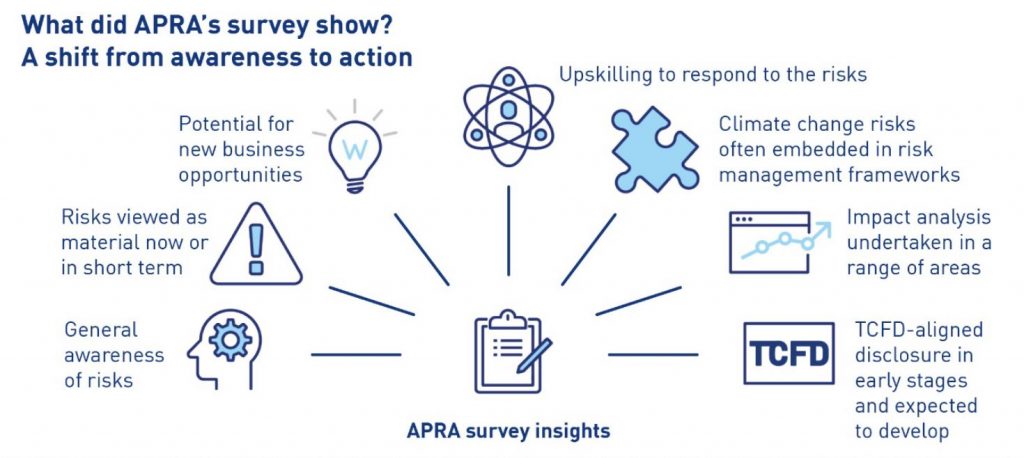

The Australian Prudential Regulation Authority (APRA) will increase its scrutiny of how banks, insurers and superannuation trustees are managing the financial risks of climate change to their businesses.

APRA surveyed 38 large banks, insurers and superannuation trustees last year to assess their views and practices related to climate-related financial risks. The survey found a substantial majority of regulated entities were taking steps to increase their understanding of the threat, including all of the banks, general insurers and superannuation trustees surveyed.

Other key findings were:

A third of respondents believed climate change was a material financial risk to their businesses now and a further half thought it would be in future;

A majority of banks considered climate-related financial risks as part of their risk management frameworks; and

Reputational damage, flooding, regulatory changes and cyclones were nominated as the top climate-related financial risks.

Respondents also described

the strategic opportunities they had identified from the transition to a low

carbon economy, including developing innovative products and services, and

meeting the growing demand for green investment opportunities.

APRA Executive Board Member Geoff Summerhayes said APRA had a responsibility to

ensure financial institutions were alert to issues that could impact their

ability to fulfil promises to customers.

“The world is rapidly transitioning to a low carbon economy, driven principally

by the decisions of governments, business leaders, investors and consumers.

Companies that fail to respond to these forces risk being left behind.

“Gaining an understanding of the risks is an important first step for entities,

but APRA wants to see continuous improvement in how organisations disclose and

manage these risks over coming years.

“APRA expects that climate risks be assessed within existing prudential risk

management standards CPS 220 and SPS 220, and supervisors will be factoring

this into their ongoing supervisory activities,” Mr Summerhayes said.

Today’s Information Paper also contains a stocktake of actions and initiatives

underway in Australia and internationally in response to growing awareness of

the physical, transitional and liability risks of climate change.

“APRA’s views on the economic risks of climate change, recently echoed by the

Reserve Bank of Australia, are consistent with those of financial regulators

internationally. These risks are material, foreseeable and actionable now.

Uncertainty over long-term impacts or policy direction is not an excuse for

doing nothing,” said Mr Summerhayes, who is also Chair of UN Environment’s Sustainable Insurance Forum.

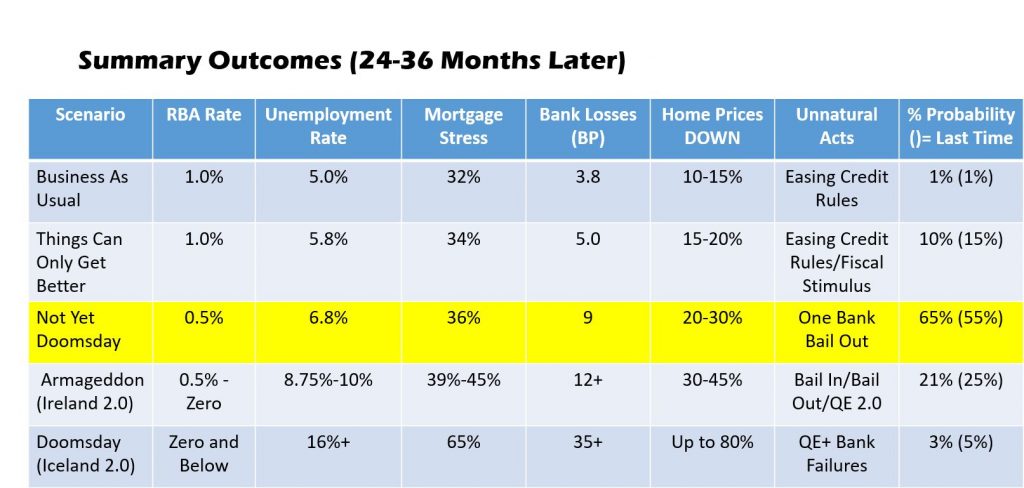

We have updated our home price and mortgage risk scenarios, based on our household surveys, and other data sources. While the risk from a global financial crisis is being pushed out temporally, as central banks do QE again, the risks of a local property crash continue to play out as expected.

As price falls pass 20%, the second order impacts on the economy also play in. We think a 20-30% fall in property values in the major markets is all but baked in now, with the risk still on the downside. The next leading indicator will be an uptick in the unemployment rate (in about 6 months time?)

We discussed the rationale for this analysis, which is driven from our Core Market Model in our live stream last night. We also answer a range of questions from viewers.

You can watch the edited edition.

Or the original live event, including the pre-show, and chat replay.

The Council of Financial Regulators (the Council) is the coordinating body for Australia’s main financial regulatory agencies. There are four members: the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC), the Australian Treasury and the Reserve Bank of Australia (RBA). The Reserve Bank Governor chairs the Council and the RBA provides secretariat support.

It is a non-statutory body, without regulatory or policy decision-making powers. Those powers reside with its members. The Council’s objectives are to contribute to the efficiency and effectiveness of financial regulation, and to promote stability of the Australian financial system. The Council operates as a forum for cooperation and coordination among member agencies. It meets each quarter, or more often if required.

It has started releasing minutes of their meetings recently. Here is the latest, not that it tells us much…. more form than substance.

At its meeting on 15 March 2019, the Council of Financial Regulators (the Council) discussed systemic risks facing the Australian financial system, regulatory issues and developments relevant to its members. The main topics discussed included the following:

Financing conditions and the housing market. The Council discussed the slowdown in housing credit growth and the weaker conditions in the housing market. Members agreed the evidence from data and consultations with banks indicated that the slowing in credit largely reflects weaker demand, particularly from investors. There has also been some tightening of credit supply over the past year as lenders have applied their lending policies more stringently and undertaken more detailed scrutiny of borrowers’ expenses and other liabilities. There remains strong competition for borrowers of low credit risk.

Housing markets remain weak, particularly in Melbourne, Sydney and Perth. However to date the adjustment in housing prices and activity has been orderly and does not raise material financial stability concerns. Housing prices nationally have fallen by 6½ per cent over the past year, but this has followed a period of large price gains in some areas. Further, the improvement in banks’ lending standards – including a lower share of high loan-to-valuation ratio lending – means that households and lenders generally are less vulnerable to falling housing prices than in the past. Despite historically high household debt, signs of financial stress remain relatively contained given a strong labour market and low interest rates. The Council noted that while mortgage arrears rates remain low, they have reached a post-financial crisis high. This largely reflects regional conditions. Overall, the future paths of housing activity and prices remain uncertain. The Council agencies will be closely monitoring the extent of any further adjustments, and in particular the ongoing availability of credit.

Small business lending. Members observed that new lending to small businesses has slowed over the past year. For many small businesses, personal and business finances are intermingled. As a consequence, the higher standards that lenders apply to personal borrowing are affecting some small business loan applications. Further falls in housing prices could constrain small business borrowing, given that around half of loans to unincorporated businesses are secured by residential property. The Council will continue to monitor developments closely and stressed the importance of lenders supplying credit to small and medium-sized businesses.

Members discussed the definition of small business in the Banking Code of Practice (the Code). They noted that the changes to the Code already due to commence on 1 July 2019 are significant. Further, the effects of these changes and any response to them by lenders, including small to medium-sized lenders, is still to be gauged. In light of this and the tightening in credit conditions that has taken place, members supported maintaining the current borrowing threshold to define small businesses within the Code, with an independent review to be undertaken within 18 months of the Code’s commencement. This would allow time for sufficient information to be gathered on the effects of the initial changes and the potential effects of the changes in the small business definition recommended by the Royal Commission. At that point it would be appropriate to consider whether to increase the limit from $3 million to $5 million for all banks. Members expressed a view that a limit based on total credit exposures is more appropriate than one based on loan size. Council members noted that other Royal Commission recommendations relevant to the Banking Code are expected to be implemented in the near term.

Final Report of the Royal Commission. Members discussed the implementation of the recommendations of the Royal Commission. This included the matters on which the Government is taking early action and the broader planning to allow the full agenda to be implemented in a timely and efficient manner. It was noted that an Implementation Steering Committee is being established and will meet shortly. It will be composed of senior representatives from Treasury, APRA, ASIC, the Office of Parliamentary Counsel and other agencies as required.

Following a request by the Government, the Council and the Australian Competition and Consumer Commission will consider the commission structure for mortgage brokers in three years’ time, including the effects of changes already announced.

Prudential policy development in Australia and New Zealand. APRA provided an update on its consultation on increasing the loss-absorbing capacity of authorised deposit-taking institutions (ADIs) to support orderly resolution. Members reiterated their in-principle support for a framework that is not overly complex. Members also discussed the Reserve Bank of New Zealand’s recent proposal to significantly increase Tier 1 capital ratios for banks operating in New Zealand, including the implications for the Australian parent banks.

The Council also discussed the activities of some of its sub-groups:

Financial Market Infrastructure (FMI) Steering Committee (the Committee). The Committee provided an update on its recent work, which has included further consideration of the design of the proposed FMI resolution regime for Australia. A further round of public consultation is likely in mid-2019. The Committee has also been working with Treasury on legislative changes that would support both the Council’s policy framework for competition in the clearing and settlement of Australian cash equities and the application of the Council’s Regulatory Expectations for Conduct in Operating Cash Equity Clearing and Settlement Services in Australia to ASX’s CHESS replacement project.

Cyber security. The Council approved new terms of reference and a work plan for its Cyber Security Working Group. The Working Group helps to coordinate cyber-related work programs among Council member agencies. Member agencies have been considering measures to increase the resilience of the financial sector to a material cyber incident, including by issuing new standards and guidance.

APRA’s Pat Brennan, Executive General Manager, Policy and Advice Division spoke at the 2019 KangaNews Debt Capital Markets Summit, Sydney

Bank capital (and liquidity) is the core of financial resilience, hence capital ratios are key indicators of financial strength. Bank boards, investors and regulators pay very close attention to these, the headline ratios and the underlying drivers, for reasons that are very obvious to this audience.

Reflecting the importance of financial strength,

APRA is in the process of updating the entire prudential framework for

capital in the banking industry. This began in 2014 with the Financial

System Inquiry recommendation for APRA to set requirements such that

Australian bank capital ratios are “unquestionably strong”, and

substantial progress has been made against this objective. More recently

at the end of 2017, the Basel Committee on Banking Supervision

finalised most of the post-global financial crisis (GFC) reforms,

finishing off in January of this year with the release of the final

market risk capital framework. In 2018 APRA began the public

consultation process as we sought to synthesise these two key drivers,

as well as introducing a variety of features that are specific to the

Australian industry.

Today I will provide an update on APRA’s

approach to risk-based capital requirements, then loss-absorbing

capacity (LAC), and then provide an update on what policy developments

APRA is working on behind the capital headlines.

Risk-based capital

A 10-year post-GFC capital build is near completion with

unquestionably strong capital ratios already attained by most banks.

Stress tests undertaken by both APRA and the IMF in recent years have

also found banks remaining above regulatory minimum requirements in very

severe stress scenarios.

While the overall amount of capital

that needs to be held by Australian banks has already been set in the

unquestionably strong benchmarks announced in July 2017, the allocation

of the precise amount of capital attributable to each source of risk is

being worked through as part of the revisions to the capital framework.

In February last year, APRA released an initial discussion paper that

proposed a number of revisions to the credit risk, operational risk and

market risk frameworks, including the adoption of a capital floor, which

will limit the capital benefit banks that use the internal

ratings-based approach (IRB) can obtain relative to those that use the

standardised approaches. These proposals focus primarily on improving

the risk sensitivity of the capital framework.

In August last

year, APRA also released a discussion paper on improving the

transparency, comparability and flexibility of the capital framework in

areas where APRA’s methodology is more conservative than minimum

international requirements. The proposals in that paper complement the

revisions to the capital framework by seeking to ensure that the capital

strength of Australian banks is appropriately understood by market

participants.

APRA expects to soon release its response to

revised capital requirements for credit risk and operational risk. In

relation to the former, the next phase of consultation will focus on the

treatment of residential mortgages for all banks, and other amendments

to the standardised approach to credit risk. Later this year, APRA will

release its full response to the revised credit risk requirements for

the IRB approach and its response to improving transparency,

comparability and flexibility. The outcome of this may lead to

significant presentational and calculation changes to a number of

prudential standards, although these would not affect the quantum of

capital required.

This stream of work is a multi-year process and

is likely to involve further rounds of consultation and quantitative

impact studies to enable APRA to assess the impact and better calibrate

the proposed changes. Given the need for extensive consultation, the

revised prudential standards are likely to be finalised in late 2020,

and are intended to commence in early 2022, consistent with the

international timetable agreed at the Basel Committee.

Loss-absorbing capacity and recapitalisation

Our work on building loss-absorbing and recapitalisation capacity

to deal with a bank failure or near-failure has been moving on a very

different timeline to risk-based capital, and deliberately so. The 2014

Financial System Inquiry recommended introducing LAC requirements in

Australia (which was consistent with APRA’s intent), adding that

international practices were still emerging at that time, and APRA

should follow these developments.

In November last year, APRA released the discussion paper Increasing the loss-absorbing capacity of authorised deposit-taking institutions to support orderly resolution.

In this paper we proposed increasing the Total Capital Requirement of

the major banks by between 4 and 5 per cent of risk-weighted assets,

with the expectation this would be mostly met through the increased

issuance of Tier 2 instruments. APRA intentionally proposed a simple

approach of using existing, well-understood capital instruments, given

they have been proven to work for their intended purpose – that is they

recapitalise a bank when needed.

Whilst APRA is still considering

submissions received and gathering additional information, and as such

we have not yet made any decisions on the proposals, I will offer a few

observations. The response we have received has been somewhat mixed. We

have been given clear feedback in a number of submissions that the

quantum of Tier 2 targeted, particularly at the higher end of the

calibration range consulted on, will test the likely bounds of investor

capacity. Submissions therefore challenged whether that calibration is

sustainable over time given debt markets will continue to experience

occasional periods of difficult issuance conditions. Some submissions

also questioned whether there are lower cost options to achieve the same

level of recapitalisation capacity, accepting these options are more

complex. On the other hand we have also received feedback from some

parties that using existing, proven capital instruments is a very good

idea.

In the debate about what is the best form of LAC, many

submissions concentrated on its form and understandably referred to the

variety of international approaches that have emerged. Submissions

offered informative perspectives on the relative merits of differing

forms of LAC from a capacity and efficiency perspective. Few, however,

reflected on the differing objectives and structures that have

influenced the divergence of international approaches.

Now is a good time to reflect that in many jurisdictions the chosen LAC approach was in direct response to their own, painful, lived experience through the GFC; with the reality of “Too Big to Fail” meaning authorities were faced with no choice but to bail-out troubled banks. In some jurisdictions this has led to a stated policy approach with the express, singular objective to never again require taxpayers to fund a bank bail-out. On the other hand, in other jurisdictions, including Australia, the objective is to protect the community from the potentially devastating broader impacts of financial crises. This is done firstly by reducing the probability of failure; and secondly by establishing sufficient recapitalisation capacity such that, should a failure or near-failure occur, the overall cost is minimised. This is consistent with the Financial System Inquiry recommendation that stated recapitalisation capacity should be “sufficient to facilitate the orderly resolution of Australian authorised deposit-taking institutions and minimise taxpayer support.”

These differing objectives guide

policy choices. Differing legislative and regulatory frameworks, and

institutional and corporate structures, around the globe also guide

choices and have played a role in influencing the divergence of

approaches adopted.

So for now we are thinking through options

and gathering additional information. APRA would still prefer a solution

that is on the side of simplicity, though at the same time we clearly

want to arrive at an approach that will work over time.

Whenever

APRA consults on a policy we undertake a genuine consultation process

and, for major policy such as this, it is an extensive process and all

submissions are carefully considered. In this case we have benefitted

from a high level of engagement with a broad range of stakeholders,

broader than is usually the case for APRA consultations, reflecting this

is new territory. At this point I cannot say when we will make public

our findings from the consultation, but given some years ago we

intentionally adopted the position of a follower of international

developments, we are now motivated to work through the considerations as

swiftly as possible.

Following finalisation of the LAC framework

APRA will build out other aspects of the prudential framework for

recovery and resolution.

And now, what is behind the headlines?

Without diminishing their importance, there is plenty that capital

ratios do not tell you. They don’t tell you how well a bank is run: if

its approach to risk management is sound, whether there is good

governance, and whether stakeholder interests are appropriately

balanced. Capital is no panacea as financial strength alone cannot

adequately mitigate against poor risk management or weak governance.

These are fundamental concerns for a prudential regulator. Capital

standards, including unquestionably strong benchmarks, are set on the

basis of at least sound risk management and governance being in place,

and so APRA has an ongoing supervisory and policy focus on non-financial

risks and drivers.

Cyber-risk, remuneration, accountability,

governance, risk management, recovery and resolution – these will

naturally become the greater part of APRA’s policy focus for the

forthcoming years. We are not lowering policy intensity on financial

risk and capital, but we are complementing and adding to this by

strengthening the prudential framework for non-financial risk.

Here is a quick overview of what to expect:

Late last year, APRA released the final version of Prudential Standard CPS 234 Information security,

which provides a clear set of requirements and expectations covering

information security, including cyber risk. We will very shortly be

supplementing this with a detailed practice guide.

In the next

quarter we will release for consultation an updated prudential standard

on remuneration. This follows the April 2018 Information Paper Remuneration practices at large financial institutions,

which reported on a thematic review APRA conducted where we found that

practices were not as robust as they should be. We have also learnt a

great deal from the CBA Prudential Inquiry and of course the Royal

Commission. The new standard will be stronger and be primarily focused

on outcomes. This will include that performance assessment must reflect

consideration of all relevant contributions to performance, including

risk management; banks will need to be transparent with APRA on how

remuneration decisions are made; and variable remuneration must be truly

variable in practice.

We will also have a significant focus on

governance and accountability. An extension of the Banking Executive

Accountability Regime (BEAR) to cover other prudentially regulated

industries has been a consideration since BEAR was first envisaged –

APRA has consistently supported this extension as the prudential

principles of BEAR apply equally across industries. Following the Royal

Commission, the BEAR extension will go even further, with a parallel

conduct accountability regime to be administered by ASIC. This is an

important development and APRA and ASIC will work closely to ensure the

parallel regimes work optimally. APRA will refresh its Governance and

Fit and Proper standards to not only more closely complement the

accountability regime, but to strengthen standards more generally; again

this will be in light of what we have learned through our supervisory

activity, through the CBA Prudential Inquiry and the findings of the

Royal Commission.

In the sphere of risk management, APRA will in the near future release for consultation a materially updated Prudential Standard APS 220 Credit Quality that

we will also rename to Credit Risk Management. Given credit is the most

material risk of the Australian banking sector we expect this will get

plenty of attention. On a slightly longer time frame, we are developing

an overarching operational risk standard and will consider changes to Prudential Standards CPS 220 Risk Management as our work of non-financial risk progresses.

In

conclusion, APRA has a comprehensive policy agenda both on bank capital

and non-financial risk. On the latter, this will draw on our

supervisory experience, the CBA prudential inquiry, the findings of the

Royal Commission and international developments. The Australian banking

system is well capitalised and APRA is supplementing that financial

strength by ensuring strong risk management and sound governance

practices are in place across the full spectrum of risks that banks

face.