The Fed held their rate again, but noted that inflation is still below its target range and uncertainties have increased. The patient wording from previous releases is missing, which may suggest a rate cut sooner than later. Their massive market operations continue.

“Effective June 20, 2019, the Federal Open Market Committee directs

the Desk to undertake open market operations as necessary to maintain

the federal funds rate in a target range of 2-1/4 to 2-1/2 percent,

including overnight reverse repurchase operations (and reverse

repurchase operations with maturities of more than one day when

necessary to accommodate weekend, holiday, or similar trading

conventions) at an offering rate of 2.25 percent, in amounts limited

only by the value of Treasury securities held outright in the System

Open Market Account that are available for such operations and by a

per-counterparty limit of $30 billion per day.

The Committee directs the Desk to continue rolling over at auction

the amount of principal payments from the Federal Reserve’s holdings of

Treasury securities maturing during each calendar month that exceeds $15

billion, and to continue reinvesting in agency mortgage-backed

securities the amount of principal payments from the Federal Reserve’s

holdings of agency debt and agency mortgage-backed securities received

during each calendar month that exceeds $20 billion. Small deviations

from these amounts for operational reasons are acceptable.

The Committee also directs the Desk to engage in dollar roll and

coupon swap transactions as necessary to facilitate settlement of the

Federal Reserve’s agency mortgage-backed securities transactions.”

Here is their statement.

Information received since the Federal Open Market Committee met in May indicates that the labor market remains strong and that economic activity is rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although growth of household spending appears to have picked up from earlier in the year, indicators of business fixed investment have been soft. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation have declined; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster

maximum employment and price stability. In support of these goals, the

Committee decided to maintain the target range for the federal funds

rate at 2-1/4 to 2-1/2 percent. The Committee continues to view

sustained expansion of economic activity, strong labor market

conditions, and inflation near the Committee’s symmetric 2 percent

objective as the most likely outcomes, but uncertainties about this

outlook have increased. In light of these uncertainties and muted

inflation pressures, the Committee will closely monitor the implications

of incoming information for the economic outlook and will act as

appropriate to sustain the expansion, with a strong labor market and

inflation near its symmetric 2 percent objective.

In determining the timing and size of future adjustments to the

target range for the federal funds rate, the Committee will assess

realized and expected economic conditions relative to its maximum

employment objective and its symmetric 2 percent inflation objective.

This assessment will take into account a wide range of information,

including measures of labor market conditions, indicators of inflation

pressures and inflation expectations, and readings on financial and

international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; Richard H. Clarida; Charles L. Evans; Esther L. George; Randal K. Quarles; and Eric S. Rosengren. Voting against the action was James Bullard, who preferred at this meeting to lower the target range for the federal funds rate by 25 basis points.

We ran our regular live Q&A event last night, and had the biggest audience ever (thanks to all those who took part).

During the show we discussed the latest data from the RBA, ABS and Moody’s, and our updated scenarios. In the current “risk-on” environment, and with the RBA’s pivot to lower rates, QE and lifting the money supply incorporated into our modelling, plus the heightened international risk profiles; there are some big changes to our scenarios.

Given the RBA (and the FED) have flipped to more QE, the future could play out a number of ways over the next 2-3 years. Indeed, if the RBA does get unemployment down to 4.5%, it is possible home prices will be higher by then.

We are expecting a small bounce, but then further falls in home prices as the broader economy weakens, and the risks from an international crisis rise further. But remember average rises or falls mask significant variations. We discuss specific examples on the show where prices have already dropped more than 30%.

You can watch the edited version of the show and our rationale for the scenario revision.

Alternatively, the original stream, including the live chat replay is available.

And we also included a view behind the scenes during the session.

The RBA’s Jonathan Kearns, Head of Financial Stability Department spoke to the Property Council. He said that the share of banks’ housing loans in arrears is now back around the level reached in 2010, the highest it has been for many years. But arrears are still well below the level reached in the early 1990s recession. But… we are NOT in recession….??? He concludes that housing arrears have risen but by no means to a level that poses a risk to financial stability. But as he says, mortgage arrears can be associated with significant personal trauma for borrowers.

I want to address an important issue for the property industry – the rising rate of housing loan arrears (Graph 1). Why is it that an increasing share of housing borrowers are behind in their mortgage repayments? Mortgage arrears can be associated with significant personal trauma for borrowers. They also point to a rising risk to the financial system as housing loans are 40 per cent of banks’ assets. If the value of the property backing the loan exceeds the value of the loan then arrears won’t have a big impact on banks’ profits or capital. But with falling housing prices the potential for banks to experience losses increases. So, on several fronts, this is an important issue.

Graph 1

There are many reasons why borrowers fall into arrears, almost all of which involve a fall in income or

rise in expenses – or both. Some borrowers experience personal misfortune, such as ill health or

a relationship breakdown, which is unrelated to economic conditions or the quality of their loan. And

even in good times, some people become unemployed. So there will always be some borrowers who fall into

arrears.

However, it is weak economic conditions that drive cyclical upswings in arrears. In particular,

borrowers can struggle to make their payments if their income falls. Weak conditions in housing markets

make it hard for borrowers to get out of arrears by selling their property. Conversely, large increases

in interest rates, say to slow an overheating economy, can also contribute to rising arrears.

Banks’ lending standards also play a role in arrears. And it is important to note that economic

conditions and lending standards interact. Poorer quality loans might continue to perform well in good

economic conditions, and only fall into arrears with an economic downturn. In contrast, good quality

loans will be more resilient in a downturn.

Because of the interaction between the various drivers of arrears, we often cannot point to a single

cause of rising arrears. Today I want to discuss the ways in which economic conditions and lending

standards are pushing arrears rates higher.

How High Are Arrears?

But first, it’s worth pausing to compare some benchmarks for the level of arrears. The share of

banks’ housing loans in arrears is now back around the level reached in 2010, the highest it has

been for many years. But arrears are still well below the level reached in the early 1990s

recession.[1]

While the increase in arrears and its level is notable, the rate of arrears in Australia is still

relatively low internationally, and in an absolute sense. The available data indicate that arrears are

lower in Australia than in many other advanced economies (Graph 2). Indeed, another way to look at

the arrears rate in Australia is to note that over 99 per cent of housing loans are on, or

ahead of, schedule. Making loans involves risk, and banks are used to managing this risk. If the arrears

rate was persistently very low, that would suggest that lenders were being too cautious in lending. In

that world, some people who could almost certainly repay a loan would struggle to get one.

Graph 2

Borrower Income

So what drives arrears? Income is a major determinant of whether borrowers can meet their repayments.

Strong employment growth for a number of years now has seen the unemployment rate decline. On the

surface, this makes it surprising that rates of arrears have been rising. But the relationship between

unemployment, income and arrears isn’t straightforward.

One factor at play is that, while the unemployment rate has declined nationally, this hasn’t

been the case everywhere. What we can see across Australia is there is a clear pattern of more loans

going into arrears in locations where the unemployment rate is higher (Graph 3). Notably the

unemployment rate has increased and income growth slowed in Western Australia and parts of Queensland

with the end of the mining boom. These areas have seen larger increases in arrears. In Western Australia

the arrears rate is now around double the rate in the rest of the country. But the flow of loans into

arrears in these regions is more than would be suggested by the unemployment rate alone.

Graph 3

Indeed, rising unemployment in some areas can’t be the whole story. As I said, the national

unemployment rate has declined in recent years. So, when it comes to arrears, falling unemployment in

some regions has not compensated for rising unemployment in others. One explanation is that it can

matter who becomes unemployed and who gains a job. People aged in their thirties and forties are more

likely to have a mortgage, particularly if they have good employment prospects. So, if more of them

become unemployed, arrears rates will rise. Conversely, if it is older or younger workers who get a job,

but don’t have a mortgage, or second income earners in households already comfortably making

their repayments, this won’t lead to a decline in arrears rates.

The length of unemployment can also influence arrears. Around two-thirds of borrowers have accumulated

buffers of prepayments of their mortgage, and some others have other assets outside of their property.

Households with financial buffers can withstand some period of unemployment, but if that extends too

long and depletes their savings, they risk falling into arrears.

There are several other reasons why focusing on unemployment doesn’t tell the full story. It

isn’t that all borrowers either receive income or don’t. Often borrowers may lose some of

their income, say because of reduced work hours, a smaller bonus or because tenants move out of their

investment property. When they don’t have a large income or savings buffer, even small income

falls or an unexpected increase in expenditure can put borrowers into arrears. Indeed in Western

Australia where arrears have increased most, rental property vacancy rates have been high, reducing the

income of landlords.

The rate of growth of income can play a role too. When nominal income is rising strongly, over time,

mortgage payments take up a declining share of a borrower’s income. As their mortgage ages and

their income rises, borrowers are better placed to withstand a fall in their income or rise in expenses.

Over the past five years, nominal income growth has been around half its longer-run average.[2] So, rising

income hasn’t been able to compensate for other factors that might cause households to struggle

to make their mortgage repayments.

Housing Prices

Another recent feature of arrears is that, on average, mortgages are staying in arrears for longer.

There are several possible explanations for this. Mortgages can leave arrears because the lender takes

possession of the property and sells it. However, the number of repossessed mortgaged properties is very

small and if anything has risen slightly, so this can’t explain longer loan arrears.

Alternatively, borrowers can leave arrears by selling their property and repaying the loan.[3] In a strong

housing market it is easy for borrowers struggling to make repayments, or already in arrears, to sell

their property. In a strong housing market, it doesn’t take long to sell a property at an

attractive price. The owner is also likely to have had several years of price growth, increasing their

equity. So if they sell they are better placed to pay off their mortgage and still have some of their

savings.

But nationally prices have fallen 8 per cent from their peak, auction clearance rates and

volumes have declined, and properties are taking longer to sell. In this environment, borrowers who fall

into arrears find it harder to sell their property and repay their loan (Graph 4). Indeed, across

the country, we see there is a strong relationship between recent housing price growth and the rate at

which borrowers are leaving arrears. In those locations where housing price growth has been weaker, a

smaller share of borrowers transition out of arrears.

Graph 4

Other Economic Factors

The weaker housing market has also seen housing credit growth slow. Because loans tend to take some

time to go into arrears, this has the effect of reducing the number of new loans that have repayments on

schedule, and so increases the overall arrears rate. But our estimates suggest that slower credit growth

accounts for less than one-tenth of the increase in the arrears rate since early 2016.

Another driver of arrears can be changes in interest rates. In the period before the GFC, arrears rates

were rising despite strong economic conditions, in part because of large increases in mortgage interest

rates. However, in recent years, interest rates on outstanding mortgages have been declining and so

average mortgage interest rates have not contributed to the generalised increase in arrears.

Lending Standards

Lending standards are also an important driver of arrears rates. Weaker lending standards mean that

borrowers can get larger loans and more borrowers get loans with potentially riskier characteristics,

such as interest only periods. For a borrower, the larger their required loan repayments relative to

their available income, the slower they will be able to build up a buffer, and so the more likely they

are to fall into arrears if their income falls or expenses rise. With weaker lending standards, more

loans will be made to borrowers who are likely to experience difficulty repaying their loan, say because

their income is less stable. For these reasons, weaker lending standards can lead to higher rates of

arrears.

In Australia there has been a significant tightening of housing lending standards by the regulators of

banks and other lenders, in earnest from around 2014. Regulators took these actions amid concerns that

strong housing market conditions and strong competition by lenders had seen lending standards erode. The

actions taken by the Australian Prudential Regulation Authority (APRA) included that banks apply more

stringent interest rate buffers to maximum loan size calculations, increase their scrutiny of

borrowers’ income and expenses, and reduce their share of lending with high loan-to-valuation

ratios (LVRs). Complementing this, the Australian Securities and Investments Commission (ASIC) increased

their focus on lenders’ compliance with responsible lending obligations, particularly in the area

of interest-only lending.[4] These actions were designed to ensure that lenders only extend as much debt to

borrowers as they will be able to repay, including a buffer.

Tighter lending standards should lead to lower arrears but this can take time to show up. Typically

borrowers’ financial pressures build over time and so average arrears rates increase with time

since loan origination, that is with ‘loan seasoning’.[5] For example, a three-year old loan is

four times more likely to go into arrears than a one-year old loan. Another challenge of assessing the

impact of lending standards on arrears is that different cohorts of loans experience common

macroeconomic conditions at different times in their seasoning. If there is a sharp increase in

unemployment in a given year, the cohort of loans originated one year earlier experience this with only

12 months of seasoning, while the cohort originated three years earlier experience it with 36 months of

seasoning. This suggests that more recent loans would likely have a larger increase in arrears in

response to rising unemployment.

Using the Reserve Bank’s Securitisation Dataset we find evidence consistent with more recent

cohorts of loans having lower arrears rates than earlier cohorts. Specifically, those loans originated

in the past few years have an arrears rate that is up to one-quarter of a percentage point lower than

loans originated prior to 2014 (controlling for seasoning and common time effects such as the state of

the economy) (Graph 5).[6] The lower arrears rates for more recent loans suggests these tighter lending

standards have been effective.

Graph 5

However, in other ways, measures taken to improve lending standards may actually temporarily increase

arrears rates. One measure addressed the large and increasing share of loans that were interest only,

meaning the borrower was not required to make regular principal payments and so the loan size did not

necessarily decline over time. In 2017, APRA imposed a 30 per cent benchmark for the maximum

share of lenders’ new loans that could be interest only. That benchmark has since been removed.

But, recognising the greater risk of interest-only lending, banks continue to charge higher interest

rates for these loans and more carefully scrutinise their suitability for borrowers. As a result, some

borrowers who may have anticipated being able to roll over an interest-only period are finding they

cannot. Some are then facing temporary difficulty servicing the higher principal and interest (P&I)

payments at the end of the interest-only period. However, most borrowers in this position get their

repayments back on track within a year.

Tighter lending standards have made it more difficult for some borrowers to refinance their loan. In

general, a borrower who, say, experienced a decline in their income may be able to reduce their

repayments by refinancing with a loan that is at a lower interest rate or has a longer term and so lower

repayments. But borrowers who are financially stretched are more likely to be constrained by tighter

borrowing restrictions. If they can’t refinance and struggle to make their existing repayments,

they are more likely to fall into arrears.

There have also been some reports that banks have been displaying greater forbearance, that is,

allowing loans to stay in arrears for longer. Supposedly, this is in response to a recognition of, and

attention on, some past poor lending decisions. However, it seems unlikely that this could explain a

significant part of the increase in aggregate arrears. In an environment of falling housing prices,

allowing a borrower to remain in arrears for longer would increase the loss that the borrower, and so

the lender, is exposed to. This wouldn’t seem to be operating in the best interests of the

borrower, or for that matter even the lender.

Conclusion

Summing up, housing arrears have risen but by no means to a level that poses a risk to financial

stability. Several factors have been interacting to drive the rise in housing arrears. Economic

conditions are undoubtedly part of the story. Weak income growth, housing price falls and rising

unemployment in some areas have all contributed. But they have not acted alone, interacting with

earlier weaker lending standards, and the more recent tightening in lending standards. To the

extent that we can point to drivers of the rise in arrears, while the economic outlook remains

reasonable and household income growth is expected to pick up, the influence of at least some

other drivers may not reverse course sharply in the near future, and so the arrears rate could

continue to edge higher for a bit longer. But with overall strong lending standards, so long as

unemployment remains low, arrears rates should not rise to levels that pose a risk to the

financial system or cause great harm to the household sector.

The RBA released their minutes today which clearly signals further rate cuts ahead as they drive toward to goal of 4.5% unemployment – the latest magic figure when wages will start to rise. Savers be dammed, to try and get household spending up.

International Economic Conditions

Members commenced their discussion by noting that the data on the global economy released since the

previous meeting had been mixed. GDP growth outcomes for the March quarter in some economies had been

slightly stronger than the second half of 2018, while labour markets had remained tight. However, global

trade and conditions in the global manufacturing sector had remained weak. New export orders had been

little changed at subdued levels and growth in industrial production had slowed in many economies,

including those economies in east Asia that are closely integrated with global supply chains.

The US–China trade dispute had escalated in May, intensifying the downside risk posed to the

global economic outlook from this source. The United States had proceeded to increase tariffs from

10 per cent to 25 per cent on US$200 billion of imports from China, and China had

responded by announcing that tariffs would increase by 5–25 per cent on

US$60 billion of US imports from 1 June 2019. In the days leading up to the meeting, the

US administration had also announced tariff measures affecting Mexico and India.

In the major advanced economies, GDP growth for the March quarter had been somewhat stronger than in

the second half of 2018. However, in both Japan and the United States the contribution from domestic

demand had declined, and investment intentions in Japan pointed to only moderate investment growth over

the period to early 2020. Nevertheless, labour markets in the advanced economies had remained tight. As

a result, wages growth had continued to increase, reaching around the highest rates recorded during the

current expansion in the three major advanced economies. Moreover, firms’ employment intentions

had remained positive at high levels and firms had continued to report widespread difficulties in

filling jobs.

Inflation had remained subdued globally despite tight labour markets and rising wages growth in many

advanced economies. Core inflation had been below target in the three major advanced economies,

following the decline in core inflation in the United States in recent months. Members noted that

temporary factors had been contributing to the decline in the US core inflation measure, with the

trimmed mean underlying inflation measure close to 2 per cent over recent months.

In China, indicators of activity had moderated in April. The moderation had partly reversed the

unusually strong results in March, which had included activity brought forward ahead of tax changes that

came into effect on 1 April 2019. Growth in fixed asset investment had slowed in April, driven by a

sharp fall in manufacturing investment, while infrastructure investment had been supported by increased

government spending. Industrial production had slowed across a wide range of products in April, although

production of construction-related materials – such as steel, plate glass and cement – had

remained strong.

Elsewhere in east Asia, growth had slowed further in the March quarter, mainly because of weaker growth

in exports and investment. Growth in India had been at the lower end of the range of recent experience,

with members noting that the recent tariff announcements by the US administration could adversely affect

Indian exports of goods.

Commodity price movements had been mixed since the previous meeting. Iron ore and rural prices had

increased. The increase in iron ore prices had been underpinned by supply constraints, strong demand

from China and an increase in steel production. On the other hand, the prices of coal, oil and base

metals had declined. Members noted that the decline in oil prices had mainly reflected renewed concerns

around the outlook for global oil demand.

Domestic Economic Conditions

Members noted that national accounts data for GDP growth in the March quarter would be released the day

after the meeting. GDP growth was expected to have been a little firmer than in the preceding two

quarters, supported by growth in exports, non-mining business investment and public spending. Growth in

consumption, however, was expected to continue to be sluggish and dwelling investment was expected to

have declined further in the March quarter.

Information received for the June quarter and indicators of future economic activity had been mixed.

Business conditions and consumer sentiment had been broadly stable at or slightly above average levels.

Information from the ABS capital expenditure survey and the Bank’s business liaison contacts

suggested that mining investment was close to its trough, while the available information pointed to

ongoing modest growth in non-residential building investment. Members noted that the low- and

middle-income tax offset, including the increase announced in the Australian Government Budget for

2019/20, would boost household disposable income and could support household

consumption in the second half of 2019.

Members also discussed the distributional implications of low interest rates on household incomes. Lower interest rates lead to a decline in the interest that households pay on their debt, but also lead to a decline in the interest income that households receive from interest-bearing assets, such as term deposits. As such, changes in interest rates have different effects on different groups of households. In particular, members recognised that many older Australians rely on interest income, which would decline with lower interest rates. The overall net effect of lower interest rates was nevertheless expected to boost aggregate household disposable income and thus spending capacity.

Conditions in established housing markets had remained weak. Housing prices had continued to decline in

Sydney and Melbourne during May, although the pace of decline had eased from earlier in the year.

Housing prices had continued to decline markedly in Perth. Members noted that the housing market was

likely to be affected by the removal of uncertainty around possible changes to taxation arrangements

relating to housing. They also considered the effects of the Australian Prudential Regulation

Authority’s (APRA’s) proposal to amend its requirement for banks to determine the

borrowing capacity of loan applicants using a specified minimum interest rate. While it remained too

early to determine the overall effects, auction clearance rates had increased noticeably in Sydney the

weekend following these developments. Building approvals had declined further in April, however, to be

more than 20 per cent lower over the preceding 12 months. This suggested that, even if

there were a marked turnaround in housing sentiment, given the lags involved it would take some time for

this to translate into higher residential construction activity.

Several key domestic data series relating to the labour market had been released over the previous

month. The wage price index had increased by 0.5 per cent in the March quarter to be

2.3 per cent higher over the year. While wages growth had been higher than a year earlier in

most industries and states, the low rate of wages growth provided further evidence of spare capacity in

the labour market. Wages growth in the private sector had been unchanged in the March quarter, and had

increased to 2.4 per cent over the year (2.7 per cent including bonuses). The Fair

Work Commission had recently granted a 3.0 per cent increase in the national minimum and award

classification wages, which would take effect from 1 July 2019. Members noted that this decision

directly affected the wages of around one-fifth of workers in Australia. Public sector wages growth had

been little changed in recent years because of caps on salary increases for public sector employees.

Members also noted that an increasing proportion of business liaison contacts were expecting wages

growth to be stable in the year ahead, although the proportion of contacts expecting wages growth to

decline had continued to fall.

The data on conditions in the labour market in April had been mixed. The unemployment rate had

increased to 5.2 per cent in April from (an upwardly revised) 5.1 per cent in March.

This followed a six-month period during which the unemployment rate had remained at around

5 per cent. The increase in the unemployment rate had been accompanied by an increase in the

participation rate to its highest level on record. The underemployment rate had also increased in April.

While the unemployment rate in both New South Wales and Victoria remained historically low, in both

states it had increased since the beginning of 2019. Employment growth nationwide had moderated in 2019,

but had remained above growth in the working-age population. Employment growth had been robust in most

states in preceding months; the exceptions were Western Australia and Tasmania, where the level of

employment had been roughly unchanged since mid 2018.

Forward-looking indicators of labour demand pointed to a moderation in employment growth in the near

term, to around the rate of growth in the working-age population. Measures of job advertisements had

declined over recent months. Employment intentions reported by the Bank’s business liaison

contacts had been lower than in mid 2018, but these intentions were still generally positive.

Members had a detailed discussion of spare capacity in the labour market. Although difficult to measure

directly, the extent of spare capacity in the labour market is an important factor that affects wages

growth and price inflation. On a number of measures, it was apparent that the labour market still had

significant spare capacity. The main approach to measuring spare capacity is to compare the current

unemployment rate with an estimate of the unemployment rate associated with full employment, which is

the rate of unemployment consistent with stable inflation. The Bank’s estimate of this

unemployment rate had declined gradually over recent years, to be around 4½ per cent

currently.

Members noted the significant uncertainty around modelled estimates of the unemployment rate consistent

with full employment. They also discussed other measures of spare capacity, including underemployment of

part-time workers, recognising that the supply side of the labour market had been quite flexible. Strong

employment growth over recent years had encouraged more people to join the labour force, allowing the

economy to absorb increased activity without generating inflationary pressure. Notwithstanding the

uncertainties involved, members revised their assessment of labour market capacity, acknowledging the

accumulation of evidence that there was now more capacity for the labour market to absorb additional

labour demand before inflation concerns would emerge.

Financial Markets

Members commenced their discussion of financial market developments by noting that escalating trade

disputes had led to a rise in volatility in global financial markets over preceding weeks, most notably

in equity markets. Nevertheless, with central banks expected to maintain expansionary policy settings

and risk premiums generally low, global financial conditions remained accommodative.

The escalation in the trade dispute between the United States and China had resulted in declines in

global equity markets. The fall in equity prices had been particularly sharp in China, but substantial

declines had also been seen in the United States as well as in a range of other advanced economies.

Members observed that the declines in equity prices had been largest for sectors more directly exposed

to the announced and prospective tariff changes and/or deriving a larger share of revenue from

international trade.

By contrast, Australian equity prices were little changed at close to their highest level in a decade.

Members noted that a sharp increase in Australian banks’ share prices, following the federal

election, had partly offset a recent decline in resource stocks in the context of escalating trade

tensions.

Members noted that there had been only a modest tightening in financial conditions in emerging markets,

including in Mexico, where trade tensions with the United States had recently resurfaced. Equity prices

had declined and sovereign credit spreads had widened somewhat, and there had been modest outflows from

bond and equity funds in emerging markets. Currencies of emerging market economies had also generally

depreciated a little, although there had mostly been little change in yields on government bonds

denominated in local currencies.

In the advanced economies, there had been some widening in yield spreads between corporate and

sovereign debt, particularly for corporations rated below investment grade. Members observed that

financing costs for corporations remained low nonetheless, with government bond yields having declined

further over the preceding month, in some cases to historic lows. This had partly reflected a shift down

in market participants’ expectations of future policy interest rates in several advanced

economies, including Australia, in an environment of ongoing trade tensions and subdued inflation. In

the cases of the United States, Canada and New Zealand, members noted that market pricing implied a

lowering of policy rates in the period ahead, although central banks in these economies had not

indicated that a near-term change in policy rates was in prospect.

Volatility in foreign exchange markets had generally remained low, although the Japanese yen had

appreciated over recent weeks, as tends to be the case in periods of increased uncertainty. There had

been a moderate depreciation of the Chinese renminbi over the preceding month.

Members noted that the Australian dollar had depreciated a little over preceding months, remaining

around the lower end of its narrow range of the preceding few years. Members also noted that while the

strength in commodity prices had supported the exchange rate, the decline in Australian government bond

yields relative to those in the major markets over 2019 had worked in the opposite direction. Long-term

government bond yields in Australia remained noticeably below those in the United States, although this

gap had narrowed a little recently as market participants’ expectations for the future path of

the US federal funds rate were revised sharply lower.

Housing credit growth had stabilised in recent months, having slowed substantially over the preceding

year. Growth in housing lending to owner-occupiers was running at around 4½ per cent in

six-month-ended annualised terms, while the rate of growth in housing lending to investors had been

close to zero since early 2019. Although standard variable reference rates for housing loans had

increased since mid 2018, the average rate paid on outstanding loans had been little changed since

then, as banks had continued to compete for new borrowers by offering materially lower rates on new

loans. Borrowers shifting from interest-only to principal-and-interest loans had also put downward

pressure on average outstanding mortgage rates.

Members were briefed on the changes proposed by APRA to its requirement that banks determine the

borrowing capacity of loan applicants using a specified minimum interest rate. Members observed that the

proposed changes would be likely to result in a modest increase in borrowing capacity for those with

lower interest rate loans, typically owner-occupiers and borrowers with principal-and-interest loans.

However, some borrowers facing higher-than-average interest rates would not see an increase in their

borrowing capacity. Members observed that such a change to serviceability assessments would mean that

any reduction in actual interest rates paid would increase households’ borrowing capacity a

little. This would be in addition to the positive effect on the cash flow of the household sector

overall.

The pace of growth in business lending had slowed in recent months, with lending to large businesses

continuing to be the sole source of growth. Lending to small businesses had declined over the preceding

year. Members noted that the stricter verification of income and expenses required for consumer lending

was also being applied to many small businesses.

Members noted that financing conditions for both financial and non-financial corporations were highly

favourable, with Australian bond yields at historic lows. Yields on residential mortgage-backed

securities were also at low levels, having declined in line with the one-month bank bill swap rate

(BBSW), which is the reference rate for these securities. Members observed that the increase in BBSW and

other short-term money market rates in 2018 had been fully unwound. As a result, the major banks’

debt funding costs were now at a historic low. The major banks’ retail deposit rates were also

historically low, with deposit rates having continued to edge lower. The average interest rate paid on

retail deposits by banks was slightly below the cash rate, although only a small share of deposits by

value received a rate below 0.5 per cent (predominantly deposits on transaction

accounts).

Financial market pricing implied that the cash rate target was expected to be lowered by 25 basis

points at the present meeting, with a further 25 basis point reduction expected later in the

year.

Considerations for Monetary Policy

In considering the stance of monetary policy, members observed that the outlook for the global economy

remained reasonable, although the risks from the international trade disputes had increased. Members

noted that the associated uncertainty had been affecting investment intentions in a number of economies

and that international trade remained weak. At the same time, the Chinese authorities had continued to

provide targeted stimulus to support economic growth, and global financial conditions remained very

accommodative. In most advanced economies, labour markets had remained tight and wages growth had picked

up, while inflation had remained subdued.

Members observed that the outlook for the Australian economy also remained reasonable, with the

sustained low level of interest rates continuing to support economic activity. A pick-up in growth in

household disposable income, continued investment in infrastructure and a renewed expansion in the

resources sector were expected to contribute to growth in output over coming years. The unemployment

rate was expected to decline a little towards the end of the forecast period, and underlying inflation

was expected to pick up gradually, to be at the lower end of the target range in the next couple of

years. Members noted that this outlook was based on the usual technical assumption that the cash rate

followed the path implied by market pricing, which suggested interest rates would be lower in the period

ahead.

The most recent data on labour market conditions had shown that, despite ongoing strong growth in

employment, the unemployment rate had not declined any further in the preceding six months and had edged

up in the most recent two months. Reasonably strong demand for labour had been met partly by a rise in

labour force participation. Members observed that this increased flexibility on the supply side of the

labour market, together with ongoing subdued growth in wages and inflation, suggested that spare

capacity was likely to remain in the labour market for some time. While wages growth had picked up from

a year earlier, it had remained subdued and recent data suggested the pick-up was only very gradual.

Together, these data suggested that the Australian economy could sustain a lower rate of unemployment

than previously estimated, while achieving inflation consistent with the target.

Members observed that underlying inflation had been below the 2–3 per cent target

range for three years and that the lower-than-expected March quarter inflation data – at

1½ per cent in underlying terms – had pointed to ongoing subdued inflationary

pressures. In part, this reflected continued slow growth in wages. Members also observed that

competition in retailing, very weak growth in rents in the context of the housing market adjustment and

government initiatives to reduce cost-of-living pressures had been dampening inflation pressures. These

factors were likely to continue for some time. Members recognised that Australia’s flexible

inflation targeting framework did not require inflation to be within the target range at all times,

which allows the Board to set monetary policy so as best to achieve the Bank’s broad objectives.

However, they also agreed that the inflation target plays an important role as a strong medium-term

anchor for inflation expectations, to help deliver low and stable inflation, which in turn supports

sustainable growth in employment and incomes.

In these circumstances, members agreed that further improvement in the labour market would be required

for wages growth and inflation to rise to levels consistent with the medium-term inflation target.

Moreover, while the Bank’s central forecast scenario for growth and inflation was unchanged, the

accumulation of data on inflation and labour market conditions over recent months had led members to

revise their assessment of the extent of inflationary pressure in the economy and, relatedly, the extent

of spare capacity in the Australian labour market.

Given these considerations, members considered the case for a reduction in the cash rate at the current

meeting. A lower level of interest rates would support growth in the economy, thereby reducing

unemployment and contributing to inflation rising to a level consistent with the target.

Members recognised that, in the current environment, the main channels through which lower interest

rates would support the economy were a lower value of the exchange rate, reduced borrowing rates for

businesses, and lower required interest payments on borrowing by households, freeing up cash for other

expenditure. Although households are net borrowers in aggregate, members recognised that there are many

individual households that are net savers and whose interest income would be reduced by lower interest

rates. Carefully considering these different effects, members judged that a lower level of interest

rates was likely to support growth in employment and incomes, and promote stronger overall economic

conditions.

Members also considered the risks associated with a lower level of interest rates in the period ahead.

Given the high level of household debt, the adjustment under way in housing markets and the tightening

in lending practices, members judged that a decline in interest rates was unlikely to encourage a

material pick-up in borrowing by households that would add to medium-term risks in the economy. Members

continued to recognise that there were risks to the forecasts for growth and inflation in both

directions. However, given the extent of spare capacity in the economy and the subdued inflationary

pressures, they judged there was a low likelihood of a decline in interest rates resulting in an

unexpectedly strong pick-up in inflation. Members also observed that a lower level of interest rates

would stimulate activity and thereby improve the resilience of the Australian economy to any future

adverse shocks.

Taking into account all the available information, the Board decided that it was appropriate to lower the cash rate by 25 basis points at this meeting. A lower level of the cash rate would assist in reducing spare capacity in the labour market, providing more Australians with jobs and greater confidence that inflation will return to be comfortably within the medium-term target range in the period ahead. Given the amount of spare capacity in the labour market and the economy more broadly, members agreed that it was more likely than not that a further easing in monetary policy would be appropriate in the period ahead. They also recognised, however, that lower interest rates were not the only policy option available to assist in lowering the rate of unemployment, consistent with the medium-term inflation target. Members agreed that, in assessing whether further monetary easing was appropriate, developments in the labour market would be particularly important.

The Decision

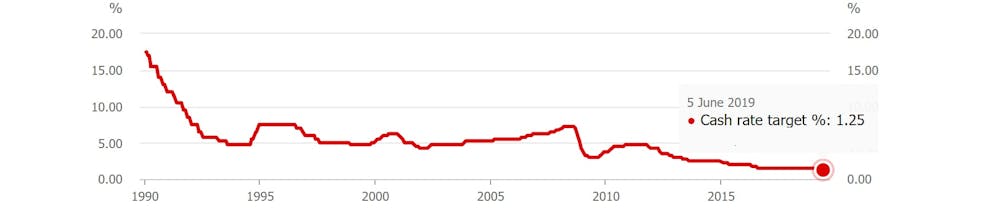

The Board decided to lower the cash rate by 25 basis points to 1.25 per cent, effective 5 June.

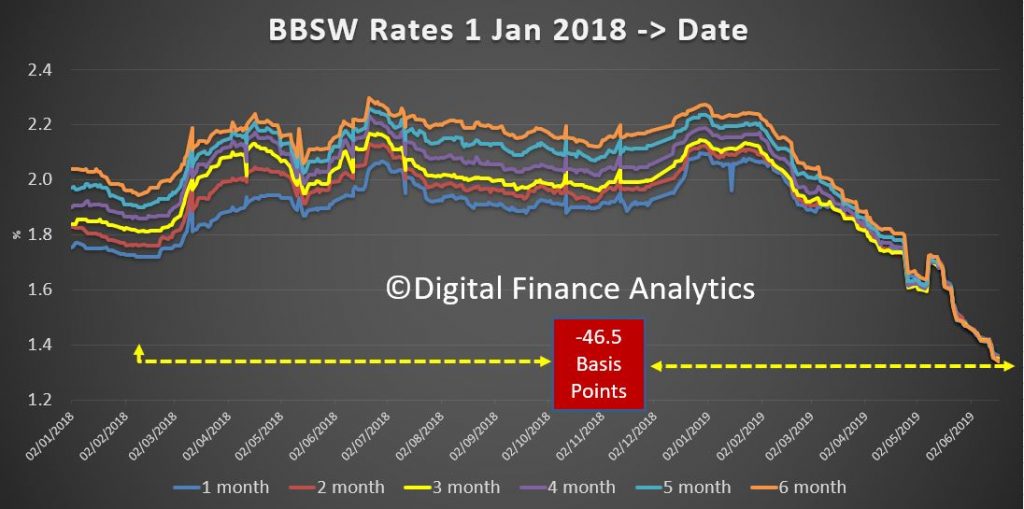

The Bank Bill Swap Rate continues to fall, reflecting lower rates here are overseas. This should give the banks more ability to pass on full rate cuts and protect their margins. Remember that a few months we were looking at significant positive swings, now we are ~46 basis points down compared with the low point past year.

Yes, deposit holds are seeing rates being chopped by 25 basis points or more, as banks seek to repair margins and compete for mortgage refinancing. The race towards zero continues….

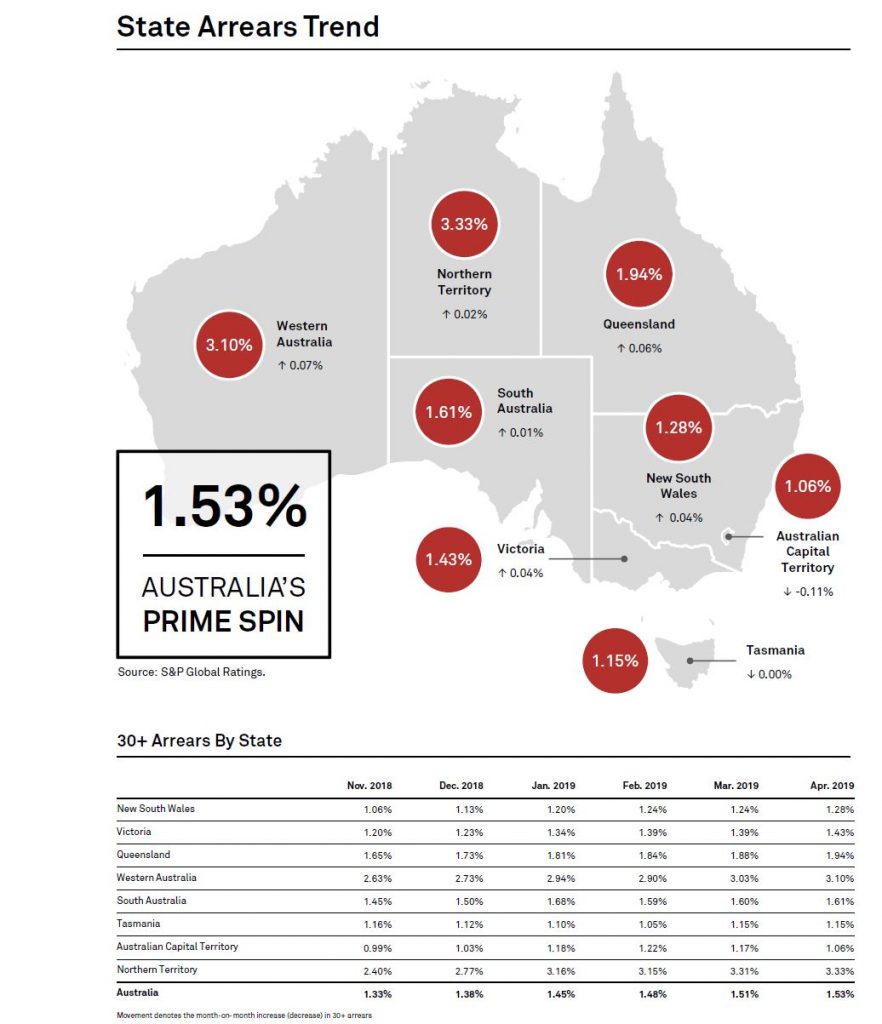

The S&P Spin Index for April shows a further rise in mortgage defaults, with WA and QLD leading the way. Only the ACT fell.

Now of course these are a myopic cross selection of loans, because they are those in the securitised pools. However, the rising trend continues.

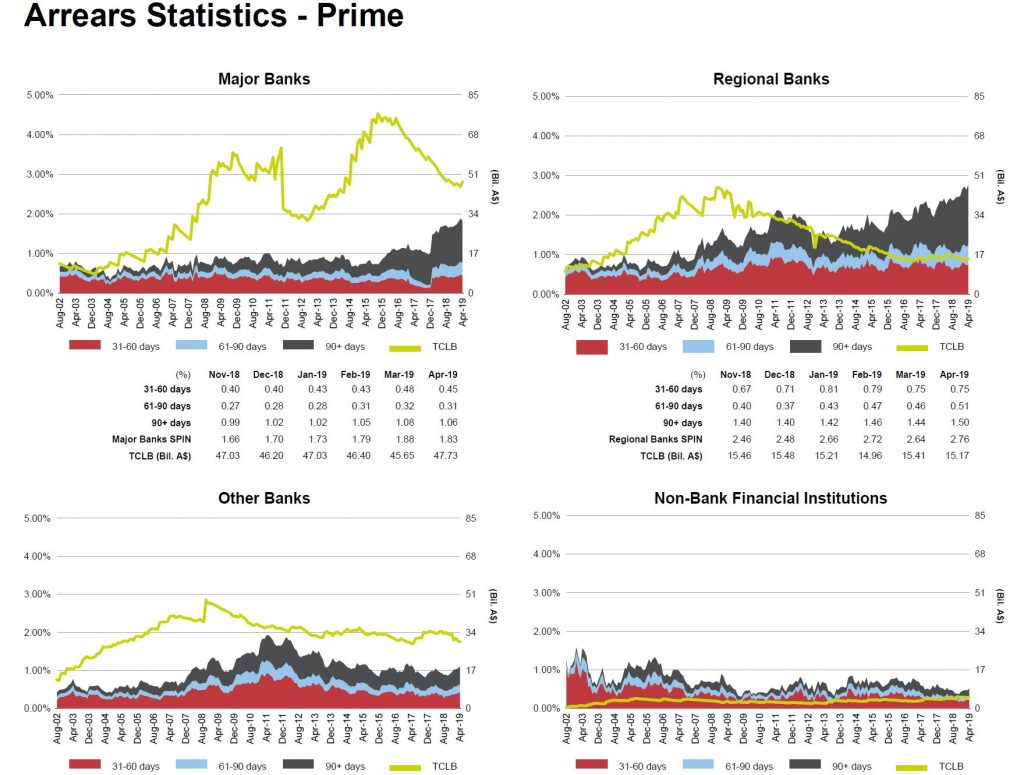

Within the mix, 90+ days arrears continue to climb especially among Regionals. It is worth reflecting that any upturn in the property market, to the extent it emerges, will have precisely NO effect on existing cash-strapped households, as the flat incomes, rising costs pincer movements continue to grip.

This was predictable, given the rising mortgage stress we have been detecting for some time. Of course the question becomes, will this lead to higher bank losses down the track?

With its official cash rate now expected to fall below 1% to a

new extraordinarily low close to zero, all sorts of people are saying

that the Reserve Bank is in danger of “running out of ammunition.” Ammunition might be needed if, as during the last financial crisis, it needs to cut rates by several percentage points.

This view assumes that when the cash rate hits zero there is nothing more the Reserve Bank can do.

The view is not only wrong, it is also dangerous, because if taken

seriously it would mean that all of the next rounds of stimulus would

have to be come from fiscal (spending and tax) policy, even though

fiscal policy is probably ineffective long-term, its effects being neutralised by a floating exchange rate.

The experience of the United States shows that Australia’s Reserve

Bank could quite easily take measures that would have the same effect as

cutting its cash rate a further 2.5 percentage points – that is: 2.5

percentage points below zero.

In a report released on Tuesday

by the University of Sydney’s United States Studies Centre, I document

the successes and failures of the US approach to so-called “quantitative

easing” (QE) between 2009 and 2014.

It demonstrates that it is always possible to change the instrument

of monetary policy from changes in the official interest rate to changes

in other interest rates by buying and holding other financial

instruments such as long-term government and corporate bonds.

The more aggressively the Reserve Bank buys those bonds from private

sector owners, the lower the long-term interest rates that are needed to

place bonds and the more former owners whose hands are filled with cash

that they have to make use of.

In the US the Federal Reserve also used “forward guidance”

about the likely future path of the US Federal funds rate to convince

markets the rate would be kept low for an extended period.

It is unclear which mechanism was the most powerful, or whether the

Fed even needed to buy bonds in order to make forward guidance work.

However in a stressed economic environment, it is worth trying both.

As it comes to be believed that interest rates will stay low for an

extended period, the exchange rate will fall, making it easier for

Australian corporates to borrow from overseas and to export and compete

with imports.

The consensus of the academic literature is that QE cut long-term

interest rates by around one percentage point and had economic effects

equivalent to cutting the US Federal fund rate by a further 2.5 percentage points after it approached zero.

QE need not have limits…

Based on US estimates, Australia’s Reserve Bank would need to

purchase assets equal to around 1.5% of Australia’s Gross Domestic

Product to achieve the equivalent of a 0.25 percentage point reduction

in the official cash rate. That’s around A$30 billion.

With over A$780 billion in long-term government (Commonwealth and

state) securities on issue, there’s enough to accommodate a very large

program of Reserve Bank buying, and the bank could also follow the

example of the Fed and expand the scope of purchases to include

non-government securities, including residential mortgage-backed

securities.

It could also learn from US mistakes. The Fed was slow to cut its

official interest rate to near zero and slow to embark on QE in the wake

of the 2008 financial crisis. Its first attempt was limited in size and

duration. Its success in using QE to stimulate the economy should be

viewed as the lower bound of what’s possible.

…even if it becomes less effective as it grows

It often suggested (although it is by no means certain)

that monetary policy becomes less effective when interest rates get

very low, but this isn’t necessarily an argument to use monetary policy

less. It could just as easily be an argument to use it more.

Because there is no in-principle limit to how much QE a central bank

can do, it is always possible to do more and succeed in lifting

inflation rate and spending.

Fiscal policy may well be even less effective. To the extent that it

succeeds, it is likely to push up the Australian dollar, making

Australian businesses less competitive.

US economist Scott Sumner believes the extra bang for the buck from government spending or tax cuts (known as the multiplier) is close to zero.

Reserve Bank Governor Philip Lowe this month appealed for help from the government itself, asking in particular for extra spending on infrastructure and measures to raise productivity growth.

He is correct in identifying the contribution other policies can make

to driving economic growth. No one seriously thinks Reserve Bank

monetary policy can or should substitute for productivity growth.

But it is a good, perhaps a very good, substitute for government spending that does not contribute to productivity growth.

Three myths about quantitative easing

In the paper I address several myths about QE. One is that it is

“printing money”. It no more prints money than does conventional

monetary policy. It pushes money into private sector hands by adjusting

interest rates, albeit a different set of rates.

Another myth is that it promotes inequality by helping the rich to get richer.

It is a widely believed myth. Former Coalition treasurer Joe Hockey told the British Institute of Economic Affairs in 2014 that:

Loose monetary policy actually helps the rich to get richer. Why?

Because we’ve seen rising asset values. Wealthier people hold the

assets.

But it widens inequality no more than conventional monetary policy,

and may not widen it at all if it is successful in maintaining

sustainable economic growth.

A third myth is that it leads to excessive inflation or socialism.

In the US it has in fact been associated with some of the lowest

inflation since the second world war. These days central banks are more

likely to err on the side of creating too little inflation than too

much.

Some have argued that QE in the US is to blame for the rise of left-wing populists

like Alexandria Ocasio-Cortez and “millennial socialism”. But it is probably truer to say that their grievances grew out of too tight rather than too lose monetary policy.

QE has been road tested. We’ve little to fear from it, just as we have had little to fear from conventional monetary policy.

Author: Stephen Kirchner, Program Director, Trade and Investment, United States Studies Centre, University of Sydney

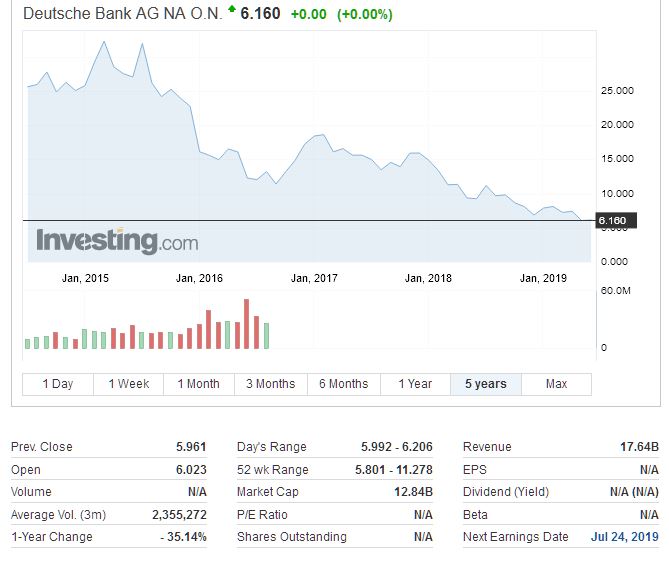

According to a report in the Financial Times, Deutsche Bank is going to overhaul its trading operations and create “bad bank” which will house or sell assets valued at up to €50B (risk adjusted). This would lead to the closure or reduction in its U.S. equity and trading businesses.

While this will likely de-risk the business, it will also reduce profitability (as the US trading division contributed higher returns, and the remaining bank will rely more on deposits for funding. This helps to explain the falls in its share price.