In 2017 then Treasurer Scott Morrison announced a bill that would require the big four banks to participate fully in the mandatory comprehensive credit reporting regime. Via The Adviser.

The legislation passed the

House of Representatives but had not passed the Senate prior to the

dissolution of parliament due to the election.

The

revised bill has introduced a new category of information within credit

reporting, enabling hardship information to be reporting alongside

repayment history information.

Attorney-General Christian Porter

also introduced new hardship arrangements to allow consumers to reveal

hardship arrangements to other credit providers.

“Proposed

changes to the Privacy Act will make sensible changes to allow for

transparent and responsible lending practices where people are subject

to hardship arrangements,” Mr Porter said.

“The amendments will

benefit consumers by making sure credit products are suitable, and

ensuring consumers are encouraged to seek hardship arrangements if they

are struggling to meet repayments under their credit contract.”

The draft legislation has just been released for public consultation which will introduce these changes.

“These

changes balance the needs of both credit providers and consumers. They

are intended to give credit providers relevant information about

consumers who are in financial hardship, or have recently experienced

hardship, in order to facilitate better and informed lending decisions,”

said Mr Porter.

The consultation period is open until September with interested parties welcome to comment on the draft legislation.

The big four bank has told ASIC to consider the utility of the broker channel before proposing bespoke responsible lending obligations, adding that it has not identified a notable difference in the quality of loans originated by the channel. Via The Adviser.

In

February, the Australian Securities and Investments Commission (ASIC)

launched a review to update its responsible lending guidance (RG 209),

which has been in place since 2010.

ASIC opened consultation by

inviting submissions from stakeholders within the financial services

sector and has since commenced a second round of consultation in the

form of public hearings, in which stakeholders that provided submissions

have been called to provide further guidance.

Appearing before

ASIC during its first round of public hearings, Westpac’s general

manager of home ownership, Will Ranken, was asked to provide an

assessment of the quality of mortgages originated through the broker

channel.

Mr Ranken noted that the bank’s verification requirements

for loans originated via the proprietary channel are the same for those

originated by brokers but acknowledged that broker-originated loans

require an “extra layer of oversight and governance”.

“When a

customer chooses to go to a broker, we’re one step removed, so there’s

another layer of oversight and governance on the broker channel,” he

said.

However, the Westpac representative stated that the bank has

not observed substantive differences in the quality and characteristics

of home loans originated by the third-party channel.

“If

you look at performance, particularly the metric around 90-day

delinquencies, they’re largely the same with our proprietary channel –

there’s no meaningful difference between those channels,” Mr Ranken

said.

“In terms of the tenure of loans, I think on average it’s

measured in months rather than quarters. In terms of the difference [in

the average tenure of the loans], it’s one or two [months].

“In terms of the size of a loan, if you look at averages, and averages can be a bit misleading, the average size of a loan through the broker channel is a little bit larger. That’s probably more for smaller loan sizes, customers are happier to deal with a branch, but for larger complex lending requirements, there’s a greater propensity for customers to go to a broker.”

Mr

Ranken was then asked if Westpac would support a move by ASIC to

prescribe different responsible lending obligations depending on how a

loan is originated.

In response, Mr Ranken warned that ASIC should

consider the effect of such changes on the value proposition of the

broker channel.

“I would say on providing additional guidance on

one particular channel over another, it would be important to take into

account the very valuable contribution that brokers do make to the

overall market,” he said.

“Specifically, I talk to the level of

competition that they facilitate in the market, either through providing

independence and access to a multitude of lenders, as well as the

service they give to customers in terms of assisting them with complex

needs.

“To the extent that guidance may require additional steps

either on the lender or the broker themselves, we just want to balance

that with ensuring that it maintains a viable and dynamic broker

channel.”

When pressed on the question, Mr Ranken added: “We’re comfortable with the policies and procedures that we’ve got in place around the broker channel, so it’s hard to comment on guidance… The devil’s in the detail. It really depends on what the detail of the guidance would be.”

Other stakeholders, however, including consumer group CHOICE, have called on ASIC to enshrine specific broker obligations in its RG 209 guidance.

CHOICE

pointed to research from ASIC’s review of interest-only home loans in

2016, which reported that mortgage broking record-keeping from

verification enquiries was “inconsistent” and, in some

cases, “fragmented and incomplete”.

Despite recent reforms from the Combined Industry Forum, which restricted the payment of commission to the loan amount drawn down by a borrower, the consumer group alleged that the supposed lack of record-keeping was “particularly harmful for consumers” because “brokers are currently incentivised to sell loans that will provide them with the largest commission”.

ASIC’s first

round of public hearings concluded, with the second round of hearings to

commence in Melbourne on Monday, 19 August.

The regulator is expected to publish its new guidance before the end of the calendar year.

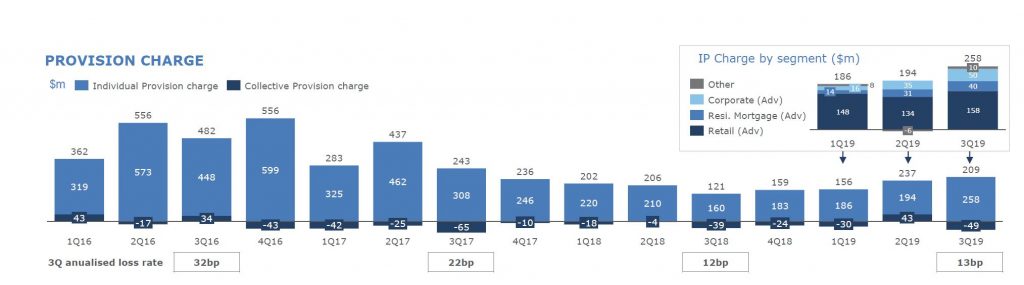

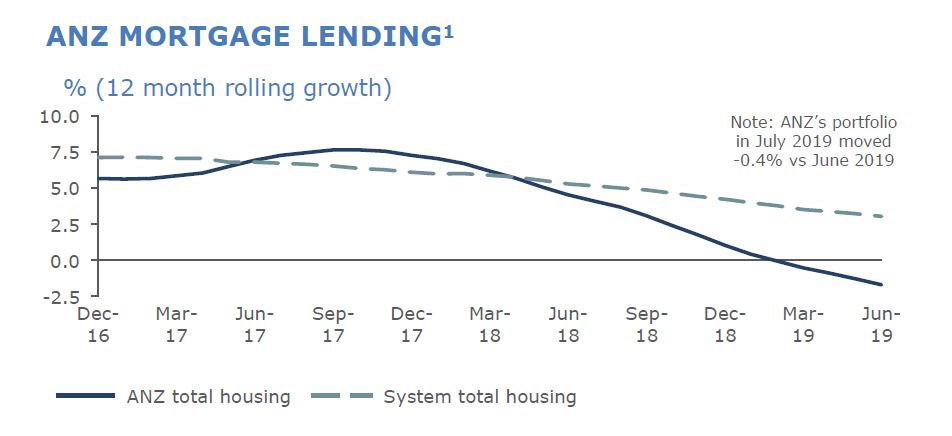

ANZ today provided an update on credit quality, capital and Australian housing mortgage flows as part of the scheduled release of its Pillar 3 disclosure statement for quarter ending 30 June 2019 and associated chart pack. Given the strategy was to shed a portfolio of businesses and focus on the Australian retail market, we need to give attention to their shrinking mortgage book and rising delinquencies.

Total provision charge of $209m for the June quarter remained broadly flat compared with the 1H19 quarterly average, while the individual provision increased $68m to $258m. Total loss rate was 13bp (consistent with the 1H19 loss rate of 13bp).

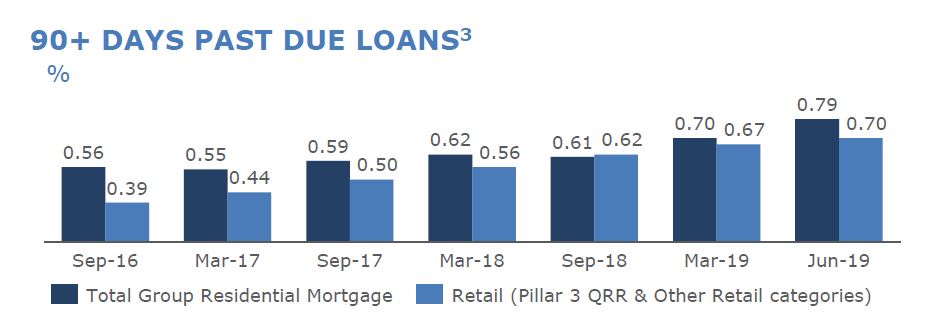

90+ Days Past Due Loans rose in the quarter.

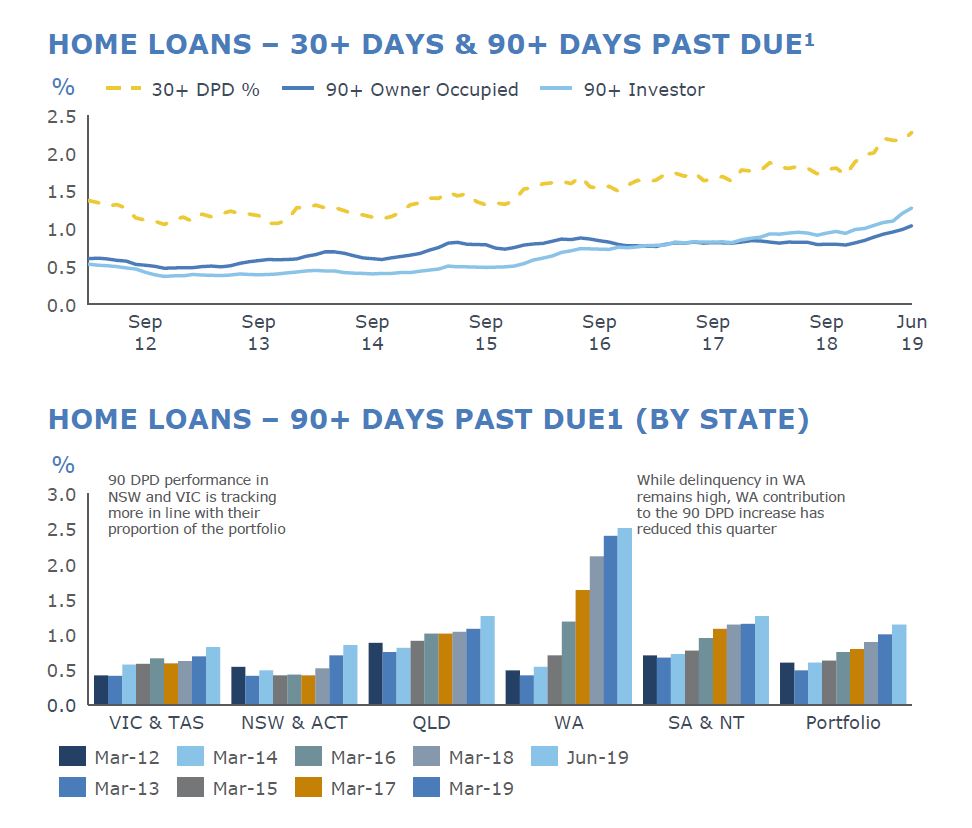

Mortgage delinquency rose in 3Q19, with 90 day increasing 14bp to 114bp. On a geographic basis, ~9bp of the movement came from NSW and VIC in aggregate. On a product basis, ~1/3 of the movement came from Interest Only home loan conversion to Principal & Interest.

WA still leads the way, but delinquencies are also rising in other states. FY17 & FY18 vintages continue to perform better than FY15 & FY16 (when of course lending standards were at their most loose, plus as we know from our mortgage stress work, it can take 2-3 years for households in financial stress to go delinquent). ANZ’s performance is likely to be biased higher given its shrinking mortgage portfolio, as we discuss below.

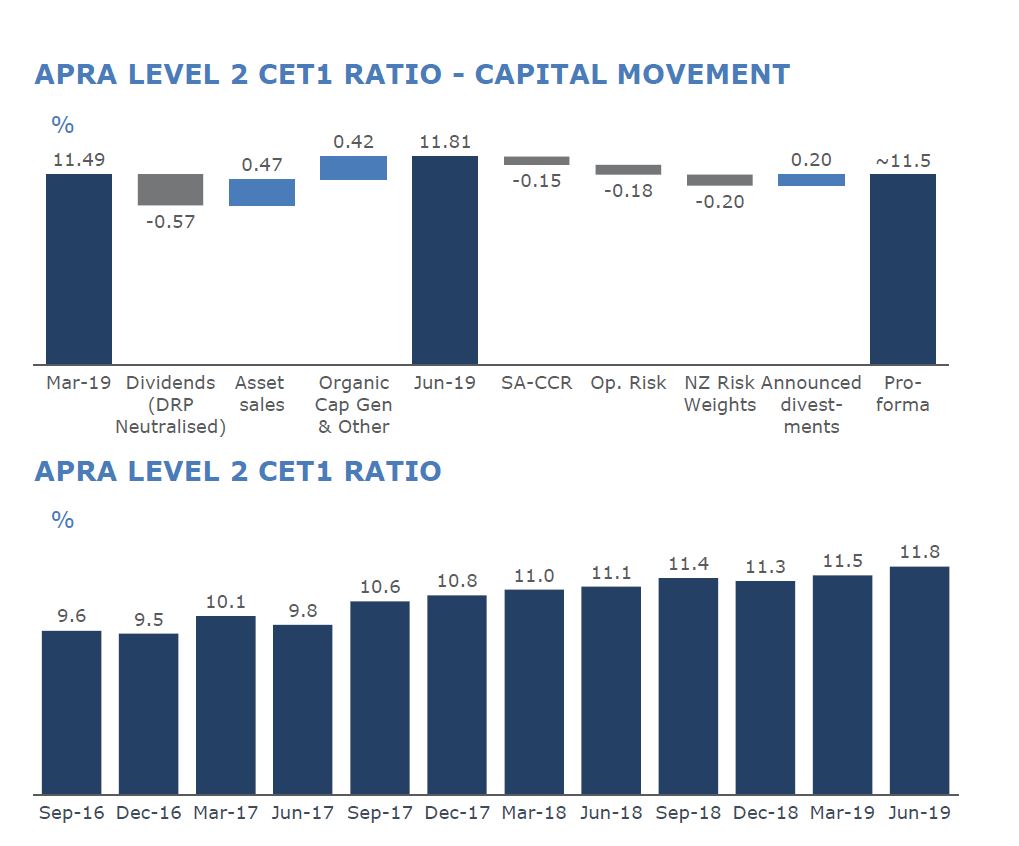

Group Common Equity Tier 1 ratio (APRA Level 2) was 11.8% at the end of June 2019, a ~30bp increase for the June quarter. On a pro-forma basis, inclusive of announced divestments and the recently announced capital changes, ANZ’s Level 2 CET1 ratio is 11.5%.

As indicated at ANZ’s first half result presentation, expectation was for home loan volumes in Australia to decline during the June quarter, with Owner Occupied down 0.2% and Investor down 1.8% (June 2019 compared with March 2019).

They say that home loan applications improved in July 2019 with actions taken in recent months to clarify credit policy and reduce approval turnaround times having a positive impact.

Following its Tuesday victory against ASIC, with the court dismissing the regulator’s allegations of irresponsible lending, Westpac has announced a spectrum of changes to its home lending policies. From Australian Broker.

The updated guidelines are set to go into effect on 20 August, at not

only the major, but its associated brands: St. George, Bank of

Melbourne, and Bank SA.

Perhaps most notably, Westpac is to update and add new expense

categories to its household expenditure measure “to reflect industry

guidelines on the HEM values we use as our customer expense benchmarks” –

bringing the total number of categories from 13 to 18.

Further, the bank will apply income-based HEM bands based on total gross unshaded income, including gross rental income.

Particularly relevant in light of the recently dismissed court case, in instances when total liability is seven times or more higher than total gross income, the loan applications will be reviewed by a credit assessment officer rather than run through the automated system.

ASIC’s case against the bank had hinged on the allegation Westpac

breached the National Consumer Credit Protection Act 2009 through

assessing loans via its automated system which solely considers the

benchmark HEM rather than customers’ declared living expenses.

Westpac additionally addressed the changes being made to tax debt through changing its approach to margin loans. They will now be assessed on the higher of 1% of the balance or the customer’s monthly declared commitment.

Further, Westpac will require a more comprehensive understanding of

payment plans businesses have made with the ATO and decline to lend to

customers with an overdue amount payable to the ATO for the previous

year’s tax without a formal payment plan in place.

The policy changes will impact all new and re-submitted applications

made from Tuesday, requiring brokers to utilise the expanded 18

categories for expenses, as well as heed the new seven times

debt-to-income ratio.

Westpac also announced that changes to the commercial, SME and private wealth broking channels will be made later this year.

The New Zealand Council of Financial Regulators (CoFR) has announced a new vision for New Zealand’s economic wellbeing and has welcomed the addition of the Commerce Commission to the forum.

The new vision aims to contribute to maximising New Zealand’s sustainable economic wellbeing through responsive and coordinated financial system regulation, and allows for a longer term view that more effectively recognises the specific responsibilities of each agency.

CoFR works to identify and respond to issues of cross-agency relevance. CoFR’s members are the Reserve Bank, Financial Markets Authority, the Treasury, Ministry of Business, Innovation and Employment, and now the Commerce Commission. Responsibility for chairing CoFR alternates between the Reserve Bank Governor and the FMA Chief Executive.

The Reserve Bank’s Governor, Adrian Orr, said: “We recognise our responsibility for joint stewardship (te hunga tiaki) of a healthy and efficient financial system that benefits all New Zealanders.”

The Financial Markets Authority’s Chief Executive, Rob Everett, said: “The Council was instrumental in launching the recent conduct and culture review of New Zealand’s banks and life insurers. This illustrated the importance and benefits of regulators working together to tackle issues that span across the financial markets’ regulatory system. Ensuring a coordinated response to such issues will help to build confidence in the regulation of New Zealand’s financial markets.”

Mr Orr says, “Bringing the Commerce Commission on board with its consumer credit focus is a welcomed addition to this forum.”

CoFR meets quarterly to discuss financial markets regulatory issues, risks and priorities, and is attended by the heads of each agency. The existence of CoFR does not derogate from the existing statutory rights and responsibilities of the respective authorities. The most recent meeting occurred yesterday.

Its main objectives are to:

Develop a collective view on longer-term strategic priorities for the financial system;

Identify and monitor important issues, risks and gaps in the financial system that may impinge upon achievement of member agencies’ regulatory objectives;

Agree collaborative responses to issues that require cross-agency involvement and put in place appropriate mechanisms to deliver them.

About the Council of

Financial Regulators

The Council of Financial Regulators (CoFR) has been operating since 2011 as a

forum for agencies with responsibility for financial sector regulation. CoFR is

comprised of the Reserve Bank, Financial Markets Authority, the Treasury,

Ministry of Business, Innovation and Employment, and recently the Commerce

Commission as a forum to share information, identify issues and develop

coordinated responses to issues that may require cross-agency involvement.

CoFR agreed to a financial markets regulatory charter in 2016, which sets out

how we operate our shared ownership of regulatory functions in this area. MBIE

developed the charter as a management tool to set expectations and provide an

overview of the regulatory system. The new vision seeks to build on this

charter.

CoFR formally meets quarterly to discuss financial markets regulatory issues,

risks and priorities. It comprises senior leaders from each agency and from

time to time, CoFR may invite representation from other regulatory agencies and

public authorities, as required.

The Federal Court has dismissed ASIC’s responsible lending case against Westpac and ordered the regulator to pay the bank’s costs. Via ABC.

I will make a separate post on the implications of this finding, in the light of ASIC stated intent to change the responsible lending laws, and the current hearings underway.

ASIC had alleged that Westpac breached responsible lending

laws on up to 262,000 home loan approvals made using an automated

process that relied on the Household Expenditure Measure benchmark,

rather than using each applicant’s individually assessed living costs.

In September last year, Westpac agreed to pay a $35 million settlement to ASIC and admit that it breached responsible lending laws.

However, in November Justice Nye Perram sensationally rejected the settlement, finding that it was ambiguous and that the parties did not actually agree on what the responsible lending laws required and, therefore, how many loans were in breach and what the penalty should be.

Today,

Justice Perram dismissed ASIC’s case against the bank, awarding costs

against the regulator and leaving it negotiating with Westpac over the

legal bill in reaching the failed settlement.

In the rejected settlement, Westpac had admitted its automated loan approval system used the Household Expenditure Measure (HEM) — a relatively low estimate of basic living expenses — to calculate potential borrowers’ living costs.

The bank used the HEM instead of actually evaluating

the customers’ declared living expenses, and admitted this practice

breached the National Consumer Credit Protection Act in certain

circumstances.

However, there was an irreconcilable difference of opinion between ASIC and Westpac over when use of the HEM breached the law.

Out

of 261,987 loans approved using the HEM benchmark, 211,937 involved

customers declaring expenses that were lower than the HEM — that is,

below the typical household’s spending on basic goods and services, and

in the bottom 25 per cent of household spending on less essential items.

In these cases, use of the HEM actually reduced the amount of money the customer could borrow compared to what they declared.

In

the roughly 50,000 cases where declared living expenses were higher

than the HEM, use of the benchmark increased the loan amount the

customer could receive.

However, in about 45,000 of these cases, both ASIC and Westpac agreed the use of the customers’ actual expenses rather than the HEM would have had no impact on whether they were deemed suitable for the loan.

That left 5,041 loans approved using the HEM that may

not have been if actual declared expenses were used — they would have

been referred to manual credit assessment instead.

This meant some

of those customers might have been approved for home loans they

potentially could not afford to repay without financial hardship.

In

rejecting the settlement, Justice Perram said neither party could

explain what would have happened after that manual loan assessment

process, whether any of these 5,041 loans were actually unsuitable and

whether any significant harm had been done to any or all of those customers

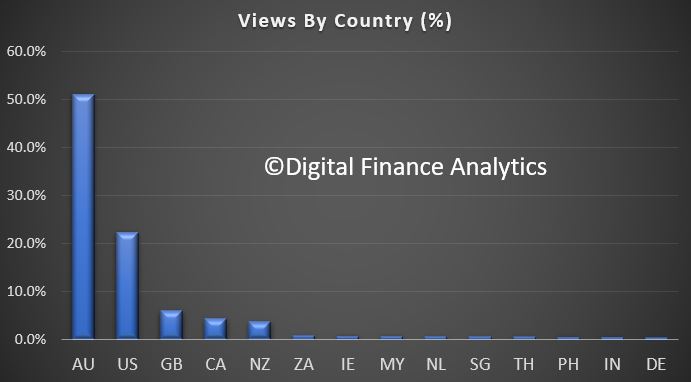

Well, who would have though it. My show with the CEC’s Robbie Barwick has now had 105,000 views in the past week and counting. So this draft bill is really hitting a nerve.

This is the biggest audience we have ever had for any of our shows. Thanks to all those who watched it and shared it.

Still time to get your submission into the Treasury today, when the consultation closes.

The country of origin is also interesting with 50% based in Australia, followed by the USA, Great Britain Canada and New Zealand. So this has significant international interest.

And if I count up the messages I have received from viewers who have posted a response to the treasury, then they will have received not tens but hundreds of submissions. Now, I wonder if they were expecting that. And if they will report the true volumes received.

And if you have submitted a response, remember to also contact your local MP and Senators in your home states. Contact details are easily found on the Parliamentary website.

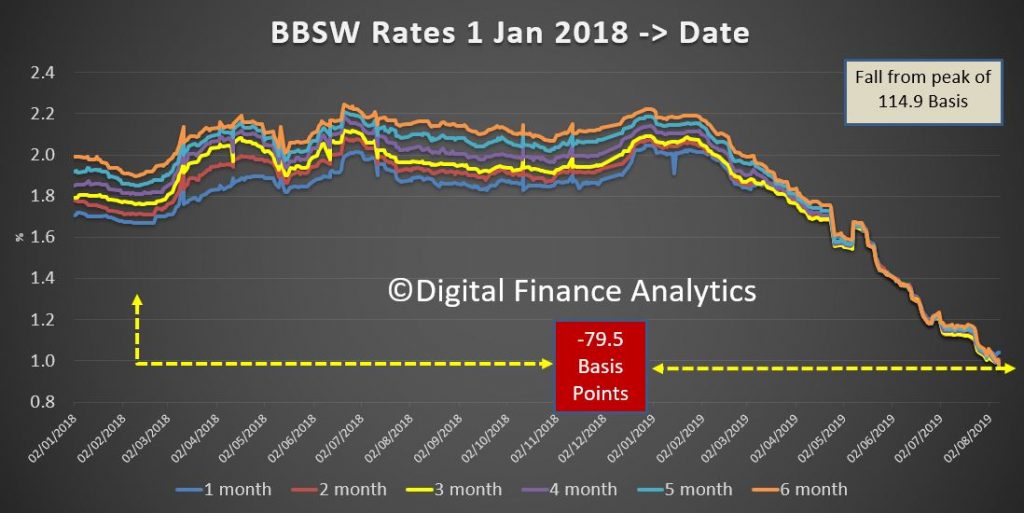

Reflecting the era ahead, the BBSW fell again and is now 114.9 basis points from peak just over 6 months ago.

This week we get June wages growth data on Wednesday and Jobs growth Thursday. We will also get more consumer confidence data on Tuesday and Wednesday, as well as a further read on business confidence.

In addition, China will release more data on Wednesday covering sales, investment and production, interesting in the context of the trade wares.

The profit reporting continues with Bendigo and Adelaide Bank already released today and Insurer QBE on Thursday.

Finally, the RBA will be busy, with Christopher Kent, Assistant Governor (Financial Markets) speaking on Tuesday, and Guy Debelle, Deputy Governor – Risks to the Outlook – on Thursday.