Westpac will decrease its floor rate from 5.75% to 5.35%, effective 30 September.

The same change will go into effect at its subsidiaries: St. George, BankSA and Bank of Melbourne.

After the initial round of floor reductions across lenders of all sizes, Westpac matched CBA with the higher floor rate of the big four banks at 5.75%, while ANZ and NAB each amended theirs to 5.50%.

Smaller lenders followed suit, the majority also updating their rates to either the 5.50% or 5.75% figure.

While some went even lower, ME Bank amending its rate down to 5.25% and Macquarie to 5.30%, Westpac has taken a step away from the other majors with its newest update.

With July marking the strongest demand for new mortgages in five years and further RBA rate cuts expected in the near future, the floor reduction seems well timed to capitalise on the strong market activity forecasted to continue into the coming

This is a race to the bottom, and is bad news for financial stability. When will APRA wake up? It will also jack some home prices higher, in selected areas and types.

The New Zealand Reserve Bank will be reporting material breaches from banks on its website from next year, in an effort to improve transparency and market discipline.

The decision follows a public consultation on the matter late last year, and ongoing discussion with stakeholders on a new framework for the reporting of banks’ breaches. The Reserve Bank today published a summary of submissions and final policy decisions on the reporting and publication of breaches by banks.

The new policy will require a bank to report promptly to the Reserve Bank when there is a breach or possible breach of a requirement in a material manner, and report all minor breaches every six months. Only actual material breaches will then be published on the Reserve Bank’s website.

“The policy aims to enhance market discipline by ensuring prompt breach reporting and publication, and by making it easier to find and compare information about banks’ compliance history,” says Geoff Bascand, Deputy Governor and General Manager Financial Stability. “It also encourages bank directors to focus on materially significant issues and the management of key risks rather than concern themselves with relatively minor issues.

“We will be further discussing the implementation of this policy directly with banks, and at this stage we expect it will take effect from 1 January 2020,” Mr Bascand says.

Reverse factoring, a form of financial engineering, is on the rise. This is a technique used by a number of companies to dress their financial results.

Australian engineering group UGL, which is working on large

infrastructure projects such as Brisbane’s Cross River Rail and

Melbourne’s Metro Trains, recently sent a letter

to suppliers and sub-contractors informing them that as of October 15,

they will be paid 65 days after the end of the month in which their

invoices are issued. The company’s policy had been, until then, to

settle invoices within 30 days.

The letter also mentioned that if the suppliers want to get paid

sooner than the new 65-day period, they can get their money from UGL’s

new finance partner, Greensill Capital, one of the biggest players in

the fast growing supply chain financing industry, in an arrangement

known as “reverse factoring”. But it will cost them.

Reverse factoring is a controversial financing technique that played a major role in the collapse of UK construction giant Carillion,

enabling it to conceal from investors, auditors and regulators the true

magnitude of its debt until it was too late. Here’s how it works: a

company hires a financial intermediary, such as a bank or a specialist

firm such as Greensill, to pay a supplier promptly (e.g. 15 days after

invoicing), in return for a discount on their invoices. The company

repays the intermediary at a later date.

In its letter to suppliers UGL trumpeted that the payment changes would “benefit both our businesses,” though many suppliers struggled to see how. One subcontractor interviewed byThe Australian Financial Review complained that the changes were “outrageous” and put small suppliers at a huge disadvantage since they did not have the power to challenge UGL. Some subcontractors contacted by AFR refused to be quoted out of fear of reprisal from UGL.

CIMIC is one of Australia’s largest construction and infrastructure

groups. It is majority owned by the German company Hochtief, which in

turn is majority owned by the Spanish consortium ACS. In August ACS, the

world’s seventh largest construction company, admitted

it is making “extensive use” of both conventional factoring and reverse

factoring “across the group,” to “more efficiently manage cash flows

and match revenues and costs over the course of the year.”

Conventional factoring is a perfectly legitimate, albeit expensive,

way for cash-strapped companies to speed up their cash flow. It involves

selling accounts receivable — the amounts a company has billed to its

customers and expects to be paid in due time — at a discount to a third

party, which then collects the money from the customers.

Reverse factoring, by contrast, is a much more pernicious yet

increasingly prevalent form of supply chain financing that is being used

by large companies to effectively transform their supply chain into a

bank. Put simply, if suppliers want to get paid in a reasonable period

of time, they must pay an intermediary for the privilege.

More importantly, in most countries there is no explicit accounting

requirement to disclose reverse factoring transactions. The companies

can effectively borrow the money from the third party lender — thus

incurring a debt — without having to disclose it as debt, meaning it

expand its borrowing while maintaining its leverage ratios. This process

causes the debt to be understated.

Credit rating agency Fitch warned last year that reverse factoring effectively served as a “debt loophole” and that use of the instrument had ballooned, though no one knows by exactly how much since there is so little disclosure.

The use of an accounting loophole allowing companies to extend ‘payables days’ by the use of third-party supply chain financing without classifying this as debt may be on the rise, according to Fitch Ratings. We believe the magnitude of this unreported debt-like financing could be considerable in individual cases and may have negative credit implications.

Supply chain financing continues to be actively marketed by banks and other institutions in the burgeoning supply chain finance industry. A technique commonly referred to as reverse factoring was a key contributor to Carillion’s liquidation as it allowed the outsourcer to show an estimated GBP400 million to GBP500 million of debt to financial institutions as ‘other payables’ compared to reported net debt of GBP219 million.

The debt classified as ‘other payables’ was unnoticed by most market participants due to the near complete lack of disclosure about these practices and the effect on financial statements. Whether these programmes require disclosure under accounting standards depends greatly on their construction, which in practice allows many companies not to disclose them.

In the six months to June, CIMIC used reverse factoring and other

supply chain financing techniques to increase its total days payable to

159 days from 135 days in the previous six months, according to New Zealand investment bank, Jarden. By the end of June, its total factoring level was almost $2 billion.

More and more Australian companies are following the same playbook.

Rail group Pacific National told suppliers in May that it was using

global financial group C2FO‘s services to facilitate what it calls “accelerated payment of approved supplier invoices.”

Telecoms giant Telstra has ramped

up its exposure to “reverse factoring” more than 14-fold in the space

of just one year, from $42 million to almost $600 million. This $551

million increase, which is also reportedly being provided at least in

part by Greensill, represents a staggering 18% of Telstra’s 2019 free

cashflow, according to a report by governance firm Ownership Matters.

Yet the company’s credit is still rated A- by S&P Global, making it

one of Australia’s highest rated industrial corporations.

A Telstra spokesman said the company strongly denies that its

accounts “are not an accurate reflection of our business,” adding for

good measure that “supply chain financing is a practice commonly used

worldwide – it provides our suppliers the option of getting paid upfront

while at the same time getting the benefit of Telstra’s strong credit

rating.” Once again, it’s a win-win for both company and suppliers.

Yet in its last financial report, Telstra disclosed that it had extended payment terms to suppliers from 30 to 45 days to 30 to 90 days. This is part of “a persistent trend” that is hurting the cash flows of small and family businesses across Australia, revealed a review of payment terms released in March by the Australian small business and family enterprise ombudsman.

There is a persistent trend in Australia of payment times being extended beyond usual industry standards. Late payment, where businesses get paid beyond contract terms, adds to the cash flow problem faced by suppliers. It appears as though large Australian companies and multinationals apply these policies to improve their own working capital efficiencies at the expense of their suppliers. While the average days to get paid is declining, it is still above 30 days at an average of 36.74 days

This average obscures the imbalance between large and small business as large business are the worst for late payments and small business the fastest.

This imbalance intensifies cash flow pressure for small and family businesses. Scottish Pacific, a large independent finance provider, estimates the cost is $234.6 billion in lost revenue. That is, SMEs would have generated more revenue if cash flow was improved, as late payments accounted for a 43% downturn in cash flow.

Small and family businesses must find other ways to finance the short fall in their working capital. This places stress on smaller businesses with significant ramifications for solvency and mental health.

The outcome; small businesses cannot invest in growth and cannot increase employment.Since the Hayne Royal Commission, banks have tightened responsible lending standards across the board which has caused a ‘credit crunch’ for small businesses. They are finding it increasingly difficult to demonstrate ‘employee-like’ cash flow like a consumer. A high growth, entrepreneurial SME is highly unlikely to demonstrate cash flow in this way.

The increased bank focus on ‘employee-like’ cash flow means more needs to be done by large corporations paying their suppliers on time. Where large corporations delay payment to their small business suppliers beyond the contracted payment time, small business cash flow is unpredictable and presents significant difficulties in their ability to access and service finance.

Not only that, it’s also making it more likely that Australia will sooner or later have a Carillion of its own on its hands.

Jyske Bank A/S, Denmark’s second-largest listed lender, will impose negative rates on all private customers with 750,000 krone ($110,000) or more, according to Bloomberg. Until Friday, only people with roughly $1 million in surplus cash at their banks were facing a negative rate. Now, the threshold has been reduced to just over $100,000, with no guarantee it won’t go lower.

Chief Executive Officer Anders Dam said the latest Danish rate cut this month means Jyske is now “losing even more money” when it deposits excess reserves at the central bank at minus 0.75%. Dam also says it’s possible the rule will be extended to an even larger group of depositors.

Denmark’s monetary policy is designed to defend the krone’s peg to the euro. But its effect on the broader economy is being closely watched. Danes have now spent seven years with rates below zero — a world record — and Dam at Jyske says he’s bracing for another eight.

Normally, low rates encourage more household spending as it gets cheaper to borrow and less appealing to save. In Denmark, negative rates have led to a surge in mortgage refinancing, but they’ve also coincided with a record build-up of consumer deposits. And, as is the case in much of the rest of Europe, inflation is missing in action.

“Households have gotten all the benefits of negative rates so far, but now they’re starting to see the bad side of negative rates,” Nielsen said.

For consumers, it’s made more sense to keep their cash in a deposit account that paid zero, rather than invest in short-term market products at negative yields. Jyske’s decision now has implications for everything from debt levels to inflation.

But it may not just be a question of economic theory. In Germany, lawmakers have debated whether to ban banks from passing negative rates on to retail depositors. Finland’s regulator has also asked its lawyers to examine the legality of the practice. In Denmark, politicians have voiced concerns.

Perhaps is time here in Australia to mount a campaign to outlaw negative deposit rates here, and even align it to the war on cash!

Australia’s pioneering

alternative lender, SocietyOne,

has reinvented P2P lending for retirees and savers in response to continuing

reductions in interest rates, where a growing inability to survive on

fixed-term deposit returns is causing an exodus into higher-risk investment

options.

Where P2P or marketplace investment

options have traditionally been segmented by risk-return tiers, SocietyOne is

once again leading with its new “P2P 2.0” model, which provides two completely

separate and differentiated offerings for its two key investor categories:

individual investors and institutional investors.

Under the new model,

institutional investors will access the original P2P product but now at a

minimum investment of $10 million, so they gain exposure to a large enough pool

of loans to achieve an acceptable level of diversification and risk for the

desired return.

Individual investors will instead

be offered an entirely new income-managed fund in which investment can now

start as low as $50,000, and which will provide a smoothed 6 per cent per annum

return, paid monthly and supported by a reserving mechanism, as well as

increased liquidity, access, and diversification.

The new model is the next

evolution of traditional P2P or marketplace lending, says CEO Mark Jones, and

yet again demonstrates SocietyOne’s commitment to a constant process of

innovation to meet its customers’ changing needs.

“Being the first P2P lender in

Australia, we’ve had many years to build a thorough understanding of our

different investor categories’ needs, and hone our investment products accordingly,”

said Mr. Jones.

“We’re also conscious of changing

economic conditions, such as the all-time-low interest rates pushing a growing

number of retirees and savers to invest in more risky products to achieve

acceptable returns. We wanted to provide a more diversified, higher-return, and

income-producing alternative.”

The Reserve Bank recently cut

interest rates back-to-back in June and July of this year, landing them at a

historic low of 1 per cent and representing the first back-to-back cut since

2012.

Long-term falling yields are

forcing the growing pool of retiree savings into higher risk products such as

‘high-income or defensive equity portfolios’ more suited to institutional and professional

investors. The significant capital-at-risk nature of these asset classes is

often glossed over.

In the event of a further

economic downturn, such as a significant global equities correction, these

higher-risk options mean Australians who are no longer earning and who require

income-based investments could lose a substantial proportion of their savings,

according to SocietyOne Chief Investment Officer, John Cummins.

“Current and future market yields

are a reflection of a slowing global and local economy. Any further downturn in

global growth and trade should lead prudent investors to choose quality

yield-based assets and not higher-risk investments,” said Mr. Cummins.

The SocietyOne P2P

2.0 “Personal Loans Unit Trust” for individual investors, as it’s named, is

currently open to wholesale and professional investors. SocietyOne intends to

open it to retail investors in the future.

The Council of Financial Regulators (the Council) is the coordinating body for Australia’s main financial regulatory agencies. There are four members: the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC), the Australian Treasury and the Reserve Bank of Australia (RBA). The Reserve Bank Governor chairs the Council and the RBA provides secretariat support. It is a non-statutory body, without regulatory or policy decision-making powers. Those powers reside with its members. The Council’s objectives are to promote stability of the Australian financial system and support effective and efficient regulation by Australia’s financial regulatory agencies. In doing so, the Council recognises the benefits of a competitive, efficient and fair financial system. The Council operates as a forum for cooperation and coordination among member agencies. It meets each quarter, or more often if required.

This is the source of the Australian financial regulatory group-think and underscores connection between the “independent” central bank and Treasury! The CFR has recently started publishing updates on its activities. This is the latest. We need an inquiry into the regulatory system, something which was missing from the Hayne Royal Commission, by design.

At its meeting on 18 September 2019, the Council of Financial Regulators (the Council) discussed risks facing the Australian financial system, regulatory issues and developments relevant to its members. The main topics discussed included the following:

Financing conditions and the housing market. Council members discussed credit conditions and recent developments in the housing market. Housing credit growth has been subdued, particularly growth in credit to investors. The major banks have seen slower growth relative to other lenders. Subdued credit growth has been primarily driven by weaker credit demand, though loan approvals have picked up recently. The potential for risks to financial stability from falling housing prices in Sydney and Melbourne has abated somewhat, with prices rising in the past few months. In contrast, prices have continued their prolonged decline in Western Australia and the Northern Territory and so the prevalence of negative equity for borrowers in those regions has continued to rise. The Council also discussed the continuing tight credit conditions for small businesses, with little growth in credit outstanding over the past year. The Council will continue to closely monitor developments.

Members discussed progress with updating the guidance

regarding responsible lending provisions in the National Consumer Credit

Protection Act 2009. The updated guidance should provide greater clarity about

what is required for a lender to comply with its obligations, taking into

consideration enhancements to lending practices, the impact of competition from

new market entrants, as well as enhanced access to and usage of consumer credit

data and technological tools.

Policy developments. APRA provided an update on a number of policy initiatives, including changes to the related entities framework for banks and other ADIs and proposals to strengthen remuneration requirements across all APRA-regulated entities. The proposed remuneration requirements seek to better align remuneration frameworks with the long-term interests of entities and their stakeholders, and incorporate a recommendation from the Royal Commission on limiting remuneration based on financial metrics. APRA briefed members on the outcomes of its capability review.

Superannuation fund liquidity. The Council considered arrangements for managing liquidity at superannuation funds during periods of market stress. They noted that arrangements had operated as intended during the financial crisis and had since been strengthened. They agreed that existing arrangements provide an appropriate incentive for superannuation funds to manage their liquidity and that circumstances where a systemic liquidity problem could arise for the superannuation system were highly unlikely. Members concluded that no additional measures, including access to liquidity from the Reserve Bank, were warranted.

Financial market infrastructure (FMI). Members discussed key elements of a package of proposed regulatory reforms for FMIs, including some changes to the supervisory framework and a resolution framework for clearing and settlement facilities. The reform package is expected to be released by the Council for consultation later in 2019. The package will seek to modernise and streamline regulators’ supervisory powers and provide new powers to resolve a distressed domestic clearing and settlement facility. Following the consultation, the Council will provide its findings to the Government to assist with policy design and the drafting of legislation.

Stored-value payment facilities. The Council finalised a report to the Government proposing a revised regulatory framework for payment providers that hold stored value. The proposed framework seeks to reduce the complexity of existing regulation, while providing adequate protection for consumers and the flexibility to accommodate innovation. Both the Financial System Inquiry and the Productivity Commission’s inquiry into Competition in the Australian Financial System called for a review of the regulatory framework. The report will be provided to the Government in the near future.

Banks’ offshore funding. The IMF’s recent Financial Sector Assessment Program (FSAP) review of the Australian financial system recommended that Australian regulators encourage a reduction of banks’ use of offshore funding and an extension of the maturity of their borrowings. Members noted that banks manage their risks from offshore borrowing through currency hedging and holding foreign currency liquid assets, and that there are various other factors mitigating the risks. They welcomed the progress that the banks had made in lengthening the maturity of their offshore term debt over recent years. A further lengthening of the maturity of their offshore borrowing would reduce the rollover risk for banks and the broader financial system.

Stablecoins. The Council considered some potential policy implications of so-called ‘stablecoins’ and associated payment services, particularly those linked to large, established networks. A stablecoin is a crypto-asset designed to maintain a stable value relative to another asset, typically a unit of currency or a commodity. Members concluded that elements of the existing regulatory framework, along with the framework proposed for stored-value facilities, were likely to apply to products of this type, but that Australian regulators would need to consider any international regulatory frameworks that might ultimately be established. Council agencies and a number of other Australian regulators are collaborating on their analysis of stablecoins. They are also drawing on their membership of several international groups focused on similar issues. Council members stressed the benefits of having a flexible, technology-neutral regulatory regime in dealing with these and other innovations.

Cyber security and crisis management. The Council reviewed work under way and planned by working groups focused on cyber security and crisis management. One focus of cyber security work in the period ahead will be aligning financial sector efforts with broader initiatives, including those of the Australian Cyber Security Centre and the Government’s 2020 Cyber Security Strategy. Recent work on crisis management in the banking sector has included a joint crisis simulation with New Zealand regulators, focussed on the testing of communications, under the auspices of the Trans-Tasman Council on Banking Supervision.

The latest edition of our weekly finance and property news digest with a distinctively Australian flavour.

Contents

1:00 The Apprentice

2:45 OECD Economic Outlook

06:28 Fed and the Repo

09:10 Trade Wars

10:00 US Markets

12:30 Central Bank Divergence

13:00 Euro zone and Brexit

13:30 Deutsche Bank Sales

15:45 AP Property Exposures

17:00 New Zealand GDP

18:24 Australian Section

18:24 Latest economic data

19:40 Employment data

20:48 Scenarios

21:30 Property prices and auctions

26:00 War on Cash

33:40 Australian markets

35:50 Australian Bank derivatives

According to the Fed, they will conduct another $75 billion worth of repurchase operations on Friday to help keep the federal funds rate within the target of 1 3/4 to 2.0 per cent. So things are still looking out of kilter – perhaps because of the Fed’s earlier balance sheet reduction?

In accordance with the FOMC Directive issued September 18, 2019, the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York will conduct an overnight repurchase agreement (repo) operation from 8:15 AM ET to 8:30 AM ET tomorrow, Friday, September 20, 2019, in order to help maintain the federal funds rate within the target range of 1-3/4 to 2 percent.

This repo operation will be conducted with Primary Dealers for up to an aggregate amount of $75 billion. Securities eligible as collateral in the repo include Treasury, agency debt, and agency mortgage-backed securities. Primary Dealers will be permitted to submit up to two propositions per security type. There will be a limit of $10 billion per proposition submitted in this operation. Propositions will be awarded based on their attractiveness relative to a benchmark rate for each collateral type, and are subject to a minimum bid rate of 1.80 percent.

In the latest RBA Bulletin there is an article on the Committed Liquidity Facility, which is a facility designed to support some of our major banks. Under the CLF, the Reserve Bank will provide an ADI with liquidity via repurchase agreements (repos), for a fee. Since the CLF was introduced in 2015, the number of ADIs that have applied to APRA to have a facility has risen from 13 to 15.

Under the Basel liquidity standard, the liquidity coverage ratio (LCR) requires authorised deposit-taking institutions (ADIs) to have enough high-quality liquid assets (HQLA) to cover their net cash outflows in a 30-day liquidity stress scenario. Jurisdictions with a clear shortage of domestic currency HQLA can use alternative approaches to enable financial institutions to satisfy the LCR – hence the CLF in Australia.

The RBA says the CLF has been in operation for five years and continues to be required given the still relatively low level of government debt in Australia. However, because the volume of HQLA securities has increased over recent years and they appear to have become more available for trading in secondary and repo markets, the Reserve Bank has assessed that the CLF ADIs should be able to raise their holdings to 30 per cent of the stock of HQLA securities. This increase will occur at a pace of 1 percentage point each year, commencing with an increase to 26 per cent in 2020. Taking into account how the CLF ADIs have responded to the framework between 2015 and 2019, the Reserve Bank has also concluded that the CLF fee should be increased from 15 basis points to 20 basis points by 2021; this is to proceed in two steps, with the fee rising to 17 basis points on 1 January 2020 and to 20 basis point on 1 January 2021.

These pricing changes will have only a minor impact on the CLF Banks in terms of their net interest margins, at a time when many other factors are in play, such as reductions in the RBA’s cash rate, competition for mortgages and the yield curve driving pricing in the 2-5 years portion of banks treasury portfolios.

But there are two bigger questions to ask and answer. First, given the size of Government debt now, and the flow of bonds available, why do we still need this facility at all?

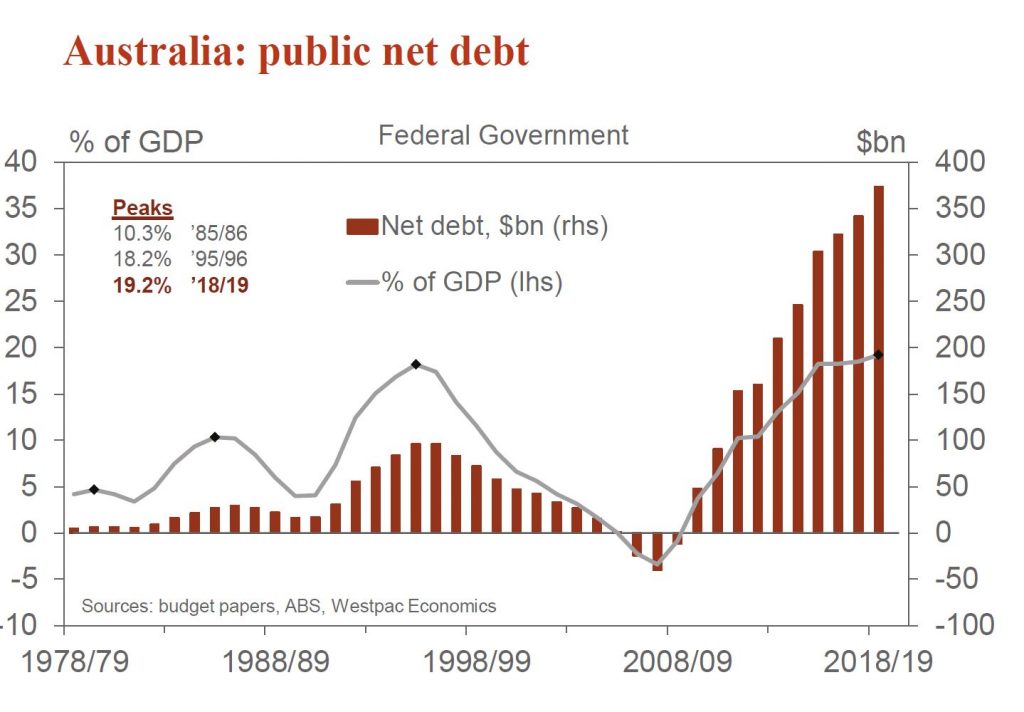

Net general government debt at June 2019 is $374bn (19.2% of GDP), some $12.5bn higher than forecast in the April 2019 Budget

The answer to that, and the second point is the CLF is essentially a back-door QE measure. If international liquidity became an issue, or if rate decreases triggered a capital flight, the CLF allows the RBA to step in and fund the banks’ funding shortfall from a loss of international investors, at rates below the banks’ international funding rates. Thus, high cost international funding by the banks can easily be replaced by cheap RBA funding through a form of QE or money printing subsidising bank profits and banker bonuses – for a short period.

This also distorts the markets because there are many lenders unable to get the CLF, creating a two-tier banking system with the “blessed” 15 supported by the CLF.

This is what the RBA says:

The Reserve Bank provides the Committed Liquidity Facility (CLF) as part of Australia’s

implementation of the Basel III liquidity standard.[1] This framework has been designed to improve the

banking system’s resilience to periods of liquidity stress. In particular, the liquidity coverage

ratio (LCR) requires authorised deposit-taking institutions (ADIs) to have enough high-quality liquid

assets (HQLA) to cover their net cash outflows in a 30-day liquidity stress scenario. Under the Basel

liquidity standard, jurisdictions with a clear shortage of domestic currency HQLA can use alternative

approaches to enable financial institutions to satisfy the LCR. These include the central bank offering a

CLF. This is a commitment by the central bank to provide funds secured by high-quality collateral through

the period of liquidity stress. This commitment can then be counted by the ADI towards meeting its LCR

requirement given the scarcity of HQLA. The Australian Prudential Regulation Authority (APRA) has

implemented the LCR in Australia, incorporating a CLF provided by the Reserve Bank.[2]

The CLF Is Required Due to the Low Level of Government Debt in Australia

The Australian dollar securities that have been assessed by APRA to be HQLA are Australian Government

Securities (AGS) and securities issued by the central borrowing authorities of the states and territories

(semis). All other forms of HQLA available in Australian dollars are liabilities of the Reserve Bank,

namely banknotes and Exchange Settlement Account (ESA) balances. For securities to be considered HQLA,

the Basel liquidity standard requires that they have a low risk profile and be traded in an active and

sizeable market. AGS and semis satisfy these requirements since they are issued by governments in

Australia and are actively traded in financial markets. In contrast, there is relatively little trading

in other key types of Australian dollar securities, such as those issued by supranationals and foreign

governments (supras), covered bonds, ADI-issued paper and asset-backed securities (Graph 1). Given

this, these securities are not classified as HQLA.

Graph 1

The supply of AGS and semis is not sufficient to meet the liquidity needs of the Australian banking

system. This reflects the relatively low levels of government debt in Australia (Graph 2). When the

CLF was first introduced in 2015, ADIs would have needed to hold around two-thirds of the stock of HQLA

securities to be able to cover their LCR requirements. Such a high share of ownership by the ADIs would

have reduced the liquidity of these securities, defeating the purpose of them being counted on as

HQLA.

Graph 2

Jurisdictions with low government debt have used a range of approaches to address the resulting shortage

of domestic currency HQLA. Australia is one of three countries that have put in place a CLF, along with

Russia and South Africa. Some other jurisdictions have allowed financial institutions to hold HQLA in

foreign currencies to cover their liquidity needs in domestic currency. The main downsides of the latter

approach is that it relies on foreign exchange markets to be functioning smoothly in a time of stress and

increases the foreign currency exposures in the banking system. Some jurisdictions have classified a

broader range of domestic currency securities as HQLA. However, this approach has not been taken in

Australia due to the low liquidity of Australian dollar securities other than AGS and semis.

The Conditions for Accessing the CLF

APRA determines which ADIs can establish a CLF with the Reserve Bank. Access is limited to those ADIs

domiciled in Australia that are subject to the LCR requirement.[3] Before establishing a CLF, these ADIs must

apply to APRA for approval. In these applications, the ADIs have to demonstrate that they are making

every reasonable effort to manage their liquidity risk independently rather than relying on the CLF. APRA

also sets the size of the CLF, both in aggregate and for each ADI.

The Reserve Bank makes a commitment under the CLF to provide a set amount of liquidity against eligible

securities as collateral, subject to the ADI having satisfied several conditions.[4] The ADI is

required to pay a CLF fee to the Reserve Bank that is charged on the entire committed amount (not just

the amount drawn). To access liquidity through the CLF, an ADI must make a formal request to the Reserve

Bank that includes an attestation from its CEO that the institution has positive net worth. The ADI must

also have positive net worth in the opinion of the Reserve Bank.

Under the CLF, the Reserve Bank will provide an ADI with liquidity via repurchase agreements (repos). In

a repo, funds are exchanged for high-quality securities as collateral until the funds are repaid. These

securities must meet criteria set by the Reserve Bank. The types of securities that the ADIs can hold for

the CLF include self-securitised residential mortgage backed securities (RMBS), ADI-issued securities,

supras, and other asset-backed securities. To protect against a decline in the value of these securities

should an ADI not meet its obligation to repay, the Reserve Bank requires the value of the securities to

exceed the amount of liquidity provided by a certain margin. These margins are set by the Reserve Bank to

manage the risks associated with holding these securities.[5] If the CLF is drawn upon, the ADI must also pay

interest to the Reserve Bank for the term of the repo at a rate set 25 basis points above the cash

rate.

The First Five Years of the CLF

Since the CLF was introduced in 2015, the number of ADIs that have applied to APRA to have a facility

has risen from 13 to 15.[6] Each year, APRA sets the total size of the CLF by taking the difference between the

Australian dollar liquidity requirements of the ADIs and the amount of HQLA securities that the Reserve

Bank assesses can be reasonably held by these ADIs (the CLF ADIs) without unduly affecting market

functioning.

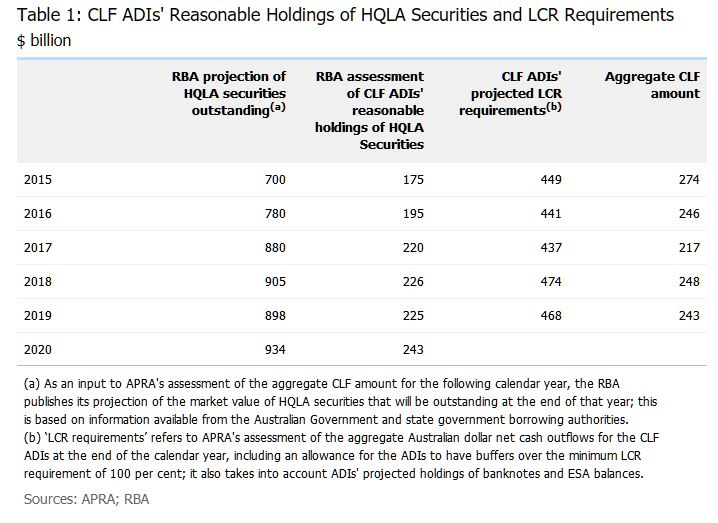

For 2015-19, the Reserve Bank assessed that the CLF ADIs could reasonably hold 25 per cent of

the stock of HQLA securities. In determining this, the Reserve Bank took into account the impact of the

CLF ADIs’ holdings on the liquidity of HQLA securities in secondary markets, along with the

holdings of other market participants. The volume of HQLA securities that the CLF ADIs could reasonably

hold increased from $175 billion in 2015 to $225 billion in 2019, reflecting growth in the stock of HQLA

securities (Table 1). Over the period, the CLF ADIs held a significantly higher share of the stock

of HQLA securities than in the years leading up to the introduction of the LCR (Graph 3). The CLF

ADIs have been holding a larger share of the stock of semis compared to AGS.

Graph 3

The CLF ADIs’ projected LCR requirements, which were used in calculating the CLF, increased

modestly in aggregate from $449 billion in 2015 to $468 billion in 2019. This increase can be entirely

explained by the CLF ADIs seeking to raise their liquidity buffers over time to be well above the minimum

LCR requirement of 100. Reflecting this, the aggregate LCR for these ADIs increased from around

120 per cent in 2015 to around 130 per cent in 2019; this was the case for their

Australian dollar liquidity requirements as well as for their requirements across all currencies

(Graph 4).[7]

Graph 4

The aggregate CLF amount is the CLF ADIs’ projected LCR requirements less the RBA’s

assessment of their reasonable holdings of HQLA securities. APRA reduced the aggregate size of the CLF

from $274 billion in 2015 to $243 billion in 2019. This reflected that the volume of HQLA securities that

the CLF ADIs could reasonably hold increased by more than their projected liquidity requirements over

this period.

From 2015 to 2019, the Reserve Bank charged a CLF fee of 15 basis points per annum on the

commitment to each ADI. The fee is set so that ADIs face similar financial incentives to meet their

liquidity requirements through the CLF or by holding HQLA. The amount of CLF fee paid by the CLF ADIs to

the Reserve Bank declined from $413 million in 2015 to $365 million in 2019, which is in line with the

reduction in the size of the CLF. Since the CLF was established, no ADI has drawn on the facility in

response to a period of financial stress.[8]

Assessing ADIs’ Reasonable Holdings of HQLA Securities

When assessing the volume of HQLA securities that the CLF ADIs can reasonably hold, the Reserve Bank

seeks to ensure that these holdings are not so large that they impair market functioning or liquidity.

For the period from 2015 to 2019, the Reserve Bank assessed that the CLF ADIs could reasonably hold

25 per cent of HQLA securities without materially reducing their liquidity. This was informed

by the fact that a large proportion of HQLA securities were owned by ‘buy and hold’

investors. These investors were price inelastic and generally did not lend these securities back to the

market, reducing the free float of HQLA securities. Many of these investors were non-residents (such as

sovereign wealth funds), which were holding nearly 60 per cent of the stock of HQLA securities

earlier in the decade (Graph 5). So overall, the Reserve Bank concluded that these bond holdings

were not contributing significantly to liquidity in the market.

Graph 5

Over recent years, the volume of HQLA securities has risen and they have become more readily available

in bond and repo markets (Table 1). The Australian repo market has grown considerably, driven by

more HQLA securities being sold under repo. Since 2015, non-residents have emerged as significant lenders

of AGS and semis (and borrowers of cash) in the domestic market (Graph 6). Over the same period,

repo rates at the Reserve Bank’s open market operations have risen relative to unsecured funding

rates (Graph 7). This is consistent with market participants financing a larger volume of HQLA

securities on a short-term basis through the repo market. For this assessment, the increased availability

of HQLA securities in the market suggests that the CLF ADIs should be able to hold a higher share of

these securities without impairing market functioning.

Graph 6

Graph 7

Analysis of transactions in the bond and repo markets using data from 2015–17 suggests that most

HQLA securities were being actively traded.[9] Monthly turnover ratios for AGS bond lines were well above

zero, and much higher than turnover ratios for other Australian dollar securities such as asset-backed

securities, covered bonds, ADI-issued paper and supras (Graph 1). Although semis bond lines were

traded less frequently than AGS, relatively few semis had low turnover ratios (Graph 8). As such,

some increase in ADIs’ holdings of AGS and semis would appear unlikely to jeopardise liquidity in

these markets.

Graph 8

Earlier in the decade, a ‘scarcity premium’ had emerged in the pricing of HQLA securities.

Australia’s relatively strong economic performance and AAA sovereign rating have been of

considerable appeal to investors with a preference for highly rated securities. Higher yields compared to

other AAA-rated sovereigns also contributed to strong demand from foreign investors, particularly for

AGS. The scarcity premium was most prominent before 2015, when the yield on 3-year AGS was well below the

expected cash rate over the equivalent horizon (as measured by overnight indexed swaps (OIS);

Graph 9). However, the scarcity premium has dissipated alongside an increase in the stock of AGS on

issue. This suggests that there is scope for the CLF ADIs to hold more HQLA securities without impairing

market functioning.

Graph 9

Given these developments, the Reserve Bank has assessed that the CLF ADIs should be able to increase

their holdings to 30 per cent of the stock of HQLA securities.[10] To

ensure a smooth transition and thereby minimise the effect on market functioning, the increase in the CLF

ADIs’ reasonable holdings of HQLA securities will occur at a pace of 1 percentage point per

year until 2024, commencing with an increase to 26 per cent in 2020.

The CLF Fee

The Reserve Bank sets the level of the CLF fee such that ADIs face similar financial incentives when

holding additional HQLA securities or applying for a higher CLF in order to satisfy their liquidity

requirements. A useful starting point to assess the appropriate CLF fee is to compare the yields on the

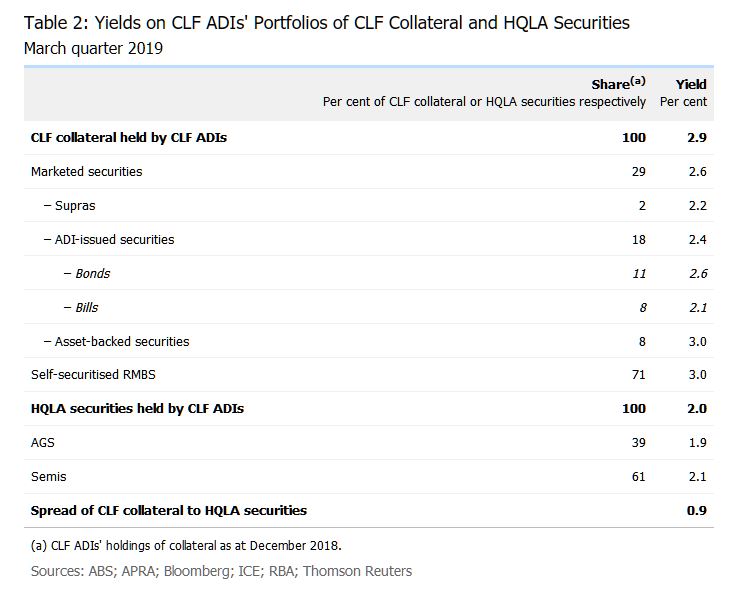

CLF collateral and the HQLA securities held by the relevant ADIs.[11] The Reserve Bank estimated that the

weighted average yield differential between the CLF collateral and the HQLA securities was around

90 basis points in the March quarter 2019 (Table 2). This includes the compensation required by

ADIs to account for the higher credit risk associated with holding CLF collateral rather than HQLA

securities, which would be a sizeable share of the spread. However, it is only the additional liquidity

risk associated with holding CLF collateral that should be reflected in the CLF fee. In practice,

adjusting the spread between CLF collateral and HQLA securities to remove the credit risk component is

not straightforward.

When the Reserve Bank set the CLF fee earlier this decade, it looked at repo rates on some CLF-eligible

securities to gauge how much a one-month liquidity premium might be worth. Before late 2013, it was

possible to separately identify repo rates on government securities (AGS and semis) and private

securities (such as ADI-issued securities) in the Reserve Bank’s market operations. Based on these

data, it was estimated that the one-month liquidity premium for private securities was less than

10 basis points in normal circumstances. However, given that part of the purpose of the liquidity

reforms was to recognise that the market had under-priced liquidity in the past, it was judged to have

been appropriate to set the fee at 15 basis points.

It has since become more difficult to gauge a liquidity premium by using repo rates. In particular, in

late 2013 the Reserve Bank ceased to charge different repo rates for government and private securities.

Instead, the Bank revised its margin schedule to manage the credit risk on different types of collateral

accepted under repo. Moreover, most of the collateral now being purchased by the Reserve Bank under repo

is HQLA securities. This suggests that repo rates mostly reflect the price for converting HQLA securities

into ESA balances, rather than CLF collateral into HQLA.

At the same time, it is now possible to take into account how the CLF ADIs have responded to the

existing framework when setting the future CLF fee. Since the CLF was introduced, the CLF ADIs (in

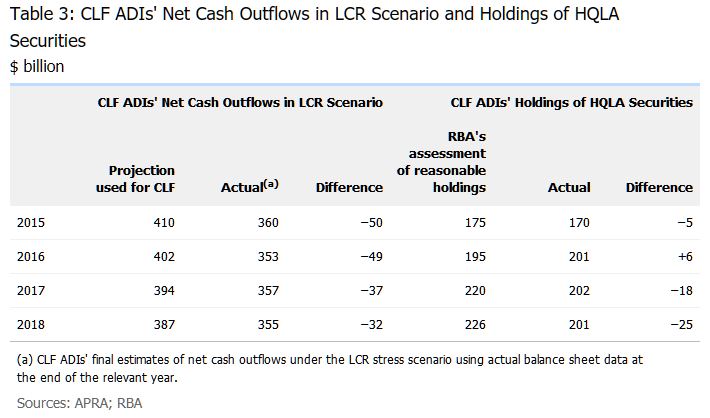

aggregate) have consistently overestimated their liquidity requirements (Table 3). This has resulted

in the CLF ADIs being granted larger CLF amounts, which they have mainly used to hold larger buffers

above the minimum required LCR of 100 (Graph 4).[12] In recent years, the CLF ADIs have also been

holding fewer HQLA securities than the Reserve Bank had judged could be reasonably held without impairing

the market for HQLA securities. Taken together, these two observations suggest that the CLF fee should be

set at a higher level in future.

However, there is uncertainty about the exact level of the fee that would make ADIs indifferent between

holding more HQLA or applying for a larger CLF. If the CLF fee is set too high, this could trigger a

disruptive shift away from using the facility and distort the markets that use HQLA. This has potential

implications for the implementation of monetary policy, since the market that underpins the cash rate

involves the trading of ESA balances, which are also HQLA.[13] The remuneration on ESA balances is purposefully

set at a rate of 25 basis points below the cash rate target in order to encourage ADIs to recycle

their surplus ESA balances rather than holding them. There are scenarios where holding ESA balances could

be a cheaper way to satisfy the LCR than holding HQLA securities. For instance, earlier in the decade,

the yield on AGS was at or below the expected return from holding ESA balances (Graph 9). In this

context, the CLF fee should be set such that ADIs would not have an incentive to meet their LCR

requirements by holding excessive ESA balances.

As a result of these considerations, the RBA has concluded that the CLF fee should be increased

moderately. This should ensure that ADIs have strong incentives to manage their liquidity risk

appropriately, without generating unwarranted distortions in the markets that use HQLA. To ensure a

smooth transition by minimising the effect on market functioning, the increase will occur in two steps,

with the CLF fee rising to 17 basis points on 1 January 2020 and to 20 basis points on 1

January 2021.[14]