The ACCC proposes to impose conditions on the Australian Banking

Association’s (ABA) Banking Code of Practice to ensure the revised Code

will benefit low-income consumers and drought-affected farmers.

The ABA, on behalf of its 23 members including the major banks, has

sought authorisation to amend its Banking Code in line with

recommendations of the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry (Hayne Royal Commission).

The proposed amendments aim to improve basic bank accounts and low or

no-fee accounts by prohibiting informal overdrafts unless requested by

the customer, and dishonour fees. The ABA is also proposing that certain

types of basic bank accounts have no minimum deposits, free direct

debit facilities, access to a debit card at no extra cost and free

unlimited domestic transactions.

In addition, the ABA’s changes would prevent default interest being charged on agricultural loans in drought-affected areas.

After considering the ABA’s proposal, the ACCC believes that additional conditions are required to strengthen these changes.

“The proposed changes to the Code should result in public benefits,

by giving customers on low incomes better access to affordable banking,

and to address a source of significant harm to farmers experiencing

drought,” ACCC Deputy Chair Delia Rickard said.

“While the ACCC strongly supports these objectives, we are proposing

to place extra conditions on ABA members to ensure the changes

effectively address the Royal Commission’s recommendations, and in turn

actually deliver these public benefits.”

For example, under the ABA’s proposal, basic bank accounts could

still be overdrawn without the customer’s agreement in some

circumstances, and banks could continue to charge interest, in some

cases at rates approaching 20 per cent, on overdrawn amounts.

“This could lead to low income customers getting into debt from

overdrafts they did not agree to, which is exactly the kind of problem

the Hayne Royal Commission sought to address,” Ms Rickard said.

The proposed conditions of authorisation would not allow interest to

be charged in these cases, or would require any such interest charges to

be repaid to the customer.

The ACCC also shares consumer groups’ concerns that the ABA’s

proposed changes would not require banks to proactively identify

existing customers who would be eligible for the accounts, or even to

continue to offer a basic bank account at all.

To address this, the ACCC’s proposed conditions would require banks

to proactively identify eligible customers, including through data

analysis; inform these customers of their eligibility, and for the ABA

to report to the ACCC on measures taken to offer them fee-free bank

accounts, and report how many customers have taken them up.

The ACCC will also require members of the ABA who currently offer a

basic banking product to continue to do so for the period of

authorisation.

Feedback is invited on these issues and the proposed conditions by 14

October 2019. The ACCC’s final determination is due in November 2019.

The draft determination and more information about the application for authorisation is available at The Australian Banking Association.

A mortgage brokerage has welcomed and affirmed the sentiment yesterday expressed by Treasurer Josh Frydenberg that “hard-working families” are being negatively impacted by stricter responsible lending rules, via Australian Broker.

Aussie Home Loans

CEO James Symond said, “We are concerned about customers being knocked

back on home loan applications due to stringent interpretations of rules

by APRA and ASIC.”

According to Symond, there is cause for concern over the low property

listings and the downturn in construction activity, despite

historically low interest rates, the likelihood they will continue to

fall and auction clearance rates picking up.

Speaking at The Australian Financial Review’s Property Summit in Sydney yesterday, Frydenberg welcomed the increase in housing prices

and linked the stabilisation in the housing sector to the easing of

lending regulations — measures, he emphasised, that “at the time

achieved their desired objectives” through mitigating risks associated

with investor loans, interest-only lending and serviceability.

Speaking of responsible lending, Frydenberg said, “While these

obligations were first legislated back in 2009, the shadow of the Royal

Commission and recent litigation has given rise to uncertainty as to how

they ought to be implemented in practice.”

“Common sense dictates that a sensible balance needs to be struck

because an unduly restrictive application of these obligations can do as

much harm as an overly lax one.

“Should responsible lending laws be applied too stringently, they

will also negatively impact consumer behaviour with consumers more

likely to remain with their current provider than go through the red

tape burden associated with looking for alternatives.

A recent study commissioned by Aussie revealed an overwhelming lack

of consumer confidence both in the housing market and in their prospects

of securing a home loan.

Just one-third of Australians are more confident about buying a home

than they were five years ago, despite record low interest rates and

lower property prices.

The study also found 70% described the home loan process negatively,

calling it ‘stressful’, ‘a waiting game,’ ‘overwhelming,’ ‘confusing,’

‘difficult,’ ‘painstaking’ and ‘rigid.’

Further, about 29% of Australians are waiting to buy property despite

promising market conditions as the home loan process has been described

as hard to navigate and riddled with red tape.

“This is why it is so important for the regulators to act to restore Australians’ confidence in the housing market and their ability to buy property,” said Symond.

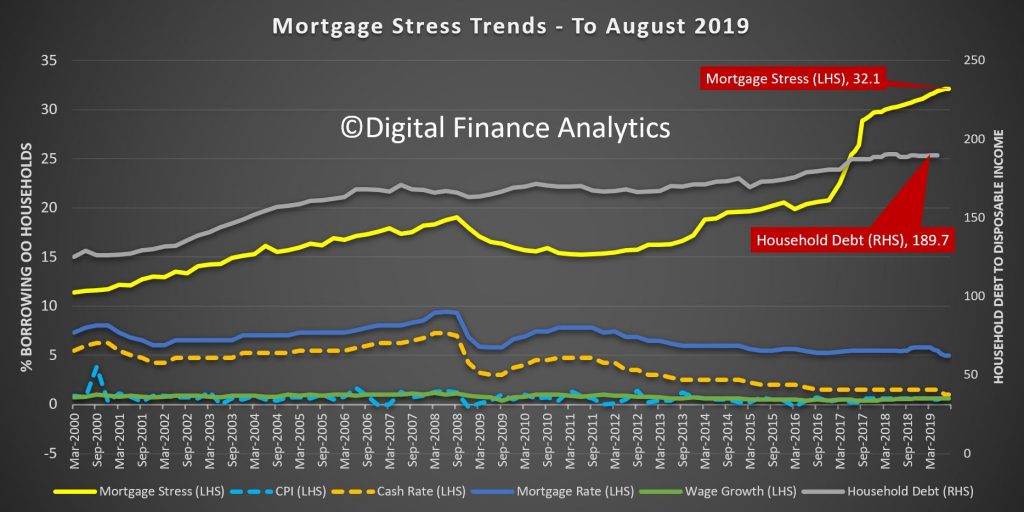

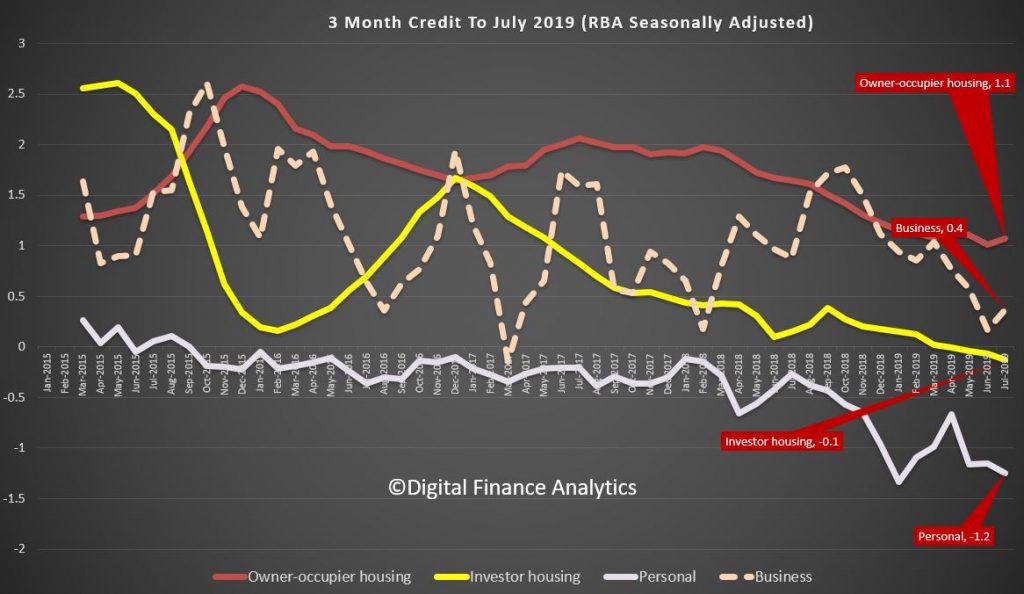

So, just worth remembering the high levels of mortgage stress in the system currently – at ultra low rates, based on our analysis to end August 2019.

As we discussed yesterday, there is only one game in town, more mortgage growth, but that game is deeply flawed….

Martin North is the Principal of Digital Finance Analytics, a boutique research, analysis and consulting firm. This former consultant of Booz Allen & Fujitsu Australia pedigree is well known for his level-headed approach to financial markets & the economy.

His Walk The World channel on YouTube is a must for astute economy watchers in Australia. While his commentary is highly regarded across mainstream media such as the AFR, Sydney Morning Herald, the ABC, 9News and many more.

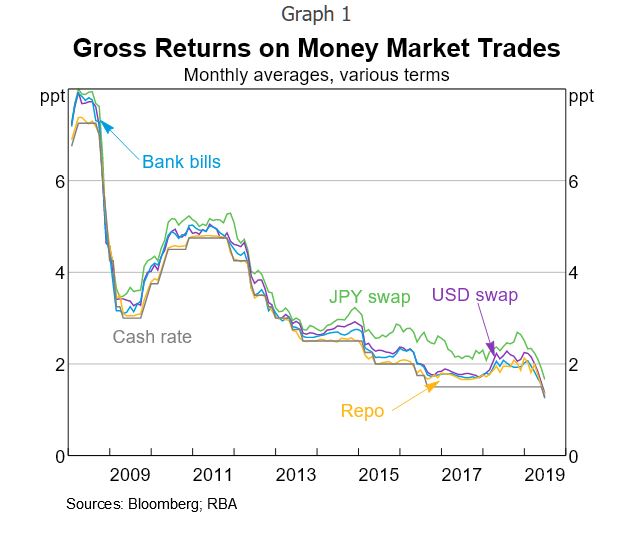

The recent RBA Bulletin included an article “Bank Balance Sheet Constraints and Money Market Divergence“, which in summary shows that money market trades have generally not been profitable for the four major banks since the financial crisis.

This is partly because debt funding costs have fallen by less than money market returns. In addition, equity funding, which is more expensive than debt, has increased. Consequently, the incentive for banks to arbitrage between money market interest rates has fallen.

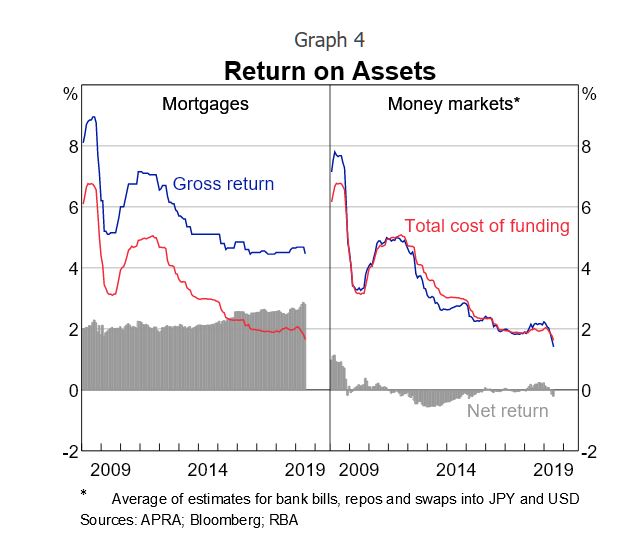

They show that residential mortgages are always significantly more profitable than money market trades over the sample period (Graph 4). This suggests that there has been a substantial opportunity cost associated with diverting equity funding away from mortgages and towards lower-margin activities such as money market trading. This is consistent with the balance sheets of the major banks being weighted towards mortgages and away from trading investments.

According to the latest property exposure statistics from the Australian

Prudential Regulation Authority (APRA), the ADI’s sector exposure to

residential mortgages increased by 3.6 per cent when comparing the June

quarter 2019 to the previous corresponding period.

Thus banks tend to prefer more profitable lines of business, such as lending for residential housing, over the narrow margins implied by money market arbitrage. In other words, bank profitability is strongly connected with mortgage growth.

We know that APRA has reduced the rules on minimum lending standards for mortgages in July, and since then, banks have dropped their minimum rate requirements, opening the taps for more loans. As Australian Broker reported recently:

Westpac will decrease its floor rate from 5.75% to 5.35%, effective 30 September.

The same change will go into effect at its subsidiaries: St. George, BankSA and Bank of Melbourne.

After

the initial round of floor reductions across lenders of all sizes,

Westpac matched CBA with the higher floor rate of the big four banks at

5.75%, while ANZ and NAB each amended theirs to 5.50%.

Smaller lenders followed suit, the majority also updating their rates to either the 5.50% or 5.75% figure.

While some went even lower, ME Bank amending its rate down to 5.25% and Macquarie to 5.30%, Westpac has taken a step away from the other majors with its newest update.

With July marking the strongest demand for new mortgages in five years and further RBA

rate cuts expected in the near future, the floor reduction seems well

timed to capitalise on the strong market activity forecasted to

continue into the coming

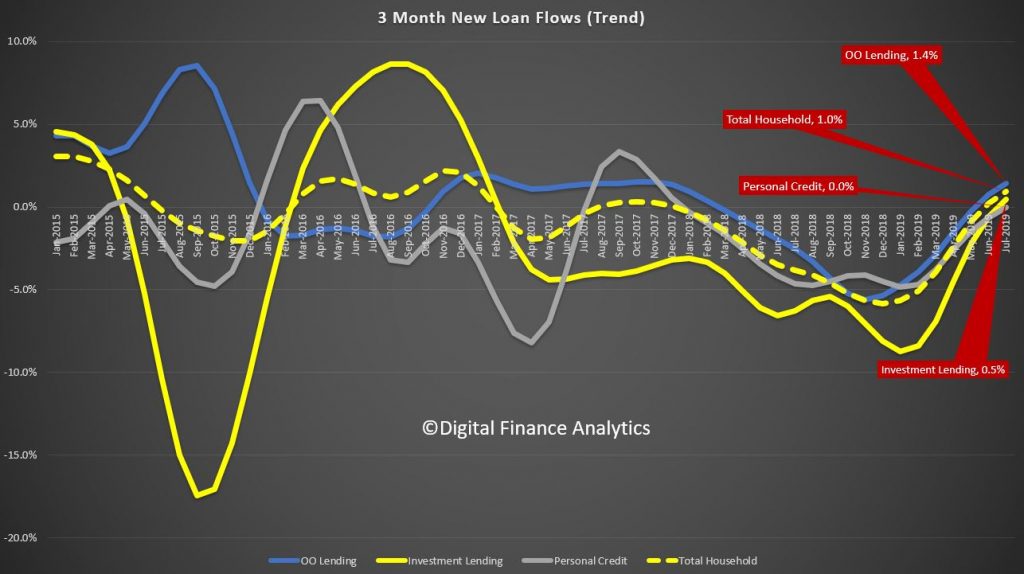

Now of course there are still tighter guidelines on income and cost analysis for mortgage applications than a couple of years ago, but have no doubt standards are lowering again, and mortgage lending momentum appears to be on the turn, judging by the most recent data.

And the RBA stock data showed a small rise in to total value of owner occupied loans outstanding, though investor loans are still sliding on a 3 month seasonally adjusted rolling basis.

We expect a further rise in the results to be released at the end of September, to end August 2019

In addition, as reported in the AFR, they are being encouraged to lend.

Scott Morrison says Australia’s banks must not shy away

from lending after the Hayne commission as he pushes back against what

he calls an “instinctiveness” in society towards responsible lending

standards that are too onerous.

Speaking to the Australian American Association in New York, the

Prime Minister said that while it was important to implement the

findings of the royal commission, as well as other reforms such as the

Banking Executive Accountability Regime, “we need our banks to keep

lending”.

“We can’t be scared of our own shadows in our economy, the animal

spirits in our economy and the role of the banking and financial system

in extending credit.

And lenders are responding with a tranche of mortgage rate cuts to attract new borrowers or new refinances (rather than passing cheaper funding costs through to existing borrowers).

For example, the Commonwealth Bank of Australia changed its New Wealth Package fixed rates for owner-occupied and investment home loans, for both new and existing customers switching to a fixed rate home/investment home loan as of Tuesday, 24 September.

The largest rate drop is for

owner-occupiers with interest-only home loans on a five-year fixed rate,

who will see rates drop by 90 basis points to 3.99 per cent, as will

investors with an interest-only home loans on a four-year fixed rate.

Owner-occupiers with IO mortgages on

one-year and four-year fixed rates will see rates drop by 65 basis

points (to 3.89 and 3.99 per cent, respectively), while those with a

three-year fixed rate will see their new rate start from 3.79 per cent

(10 basis points lower than previous).

Other sizeable rate drops include

investors with a four-year fixed rate on P&I repayments, who will

see their interest rates fall by 75 basis points to 3.64 per cent.

Investors with P&I repayments on other fixed rate terms will see rates drop from between 5 and 50 basis points.

Owner-occupiers with a P&I home

loan that is on a one-year fixed rate term will see a range change of 60

basis points, dropping the new rate to 3.29 per cent. Those with a

four-year fixed rate will also see their rates drop by the same amount,

bringing the new rate to 3.49 per cent.

And ME Bank announced reductions of up to 49 basis points across its variable home loan products for investors.

The rate reduction announcement comes a week following ME bank’s 2019 financial year results, which saw its home loan portfolio grow by 7.3 per cent, from $24.5 billion to $26.3 billion (or 2.5 times system growth).

The bank has cut rates for investors on both principal and interest (P&I) and interest-only (IO) loans with a loan-to-value ratio of less than, or equal to, 80 per cent.

The changes have been applied to the

“flexible home loan member package” for investors, as well as the “basic

home loan” investor product, with all changes effective as of Tuesday,

24 September 2019.

The largest rate reduction (49 basis

points) was applied to the bank’s basic home loan product, for investors

making principal and interest repayments.

For investors on the bank’s basic home loan product, the new rates are as follows:

P&I repayments, any loan amount – 49 basis point reduction to 3.68 per cent p.a. (3.70 per cent comparison rate)

IO repayments, any loan amount – 45 basis point reduction to 3.89 per cent p.a. (3.79 per cent comparison rate)

Investors currently on the flexible home loan package (which requires an annual fee of $395) will see the following changes:

P&I

repayments on a loan amount above $700,000 – 14 basis point reduction to

3.63 per cent p.a. (4.06 per cent comparison rate)

IO

repayments on a loan amount between $400,000-$700,000 – 23 basis point

reduction to 3.89 per cent p.a. (4.19 per cent comparison rate)

So to Philip Lowe’s recent speech “An Economic Update” where he said that…

…the global economy is that while it is still growing reasonably well, the risks are increasingly tilted to the downside. The main source of these downside risks are geopolitical developments in many parts of the world. These developments are creating considerable uncertainty and this uncertainty is causing businesses to reconsider their spending plans. This is making the international environment more challenging for us.

On the Australian economy, he said after having been through a soft patch, a gentle turning point has been reached. While we are not expecting a return to strong economic growth in the near term, we are expecting growth to pick up. Against this backdrop, the main source of domestic uncertainty continues to be the strength of household spending.

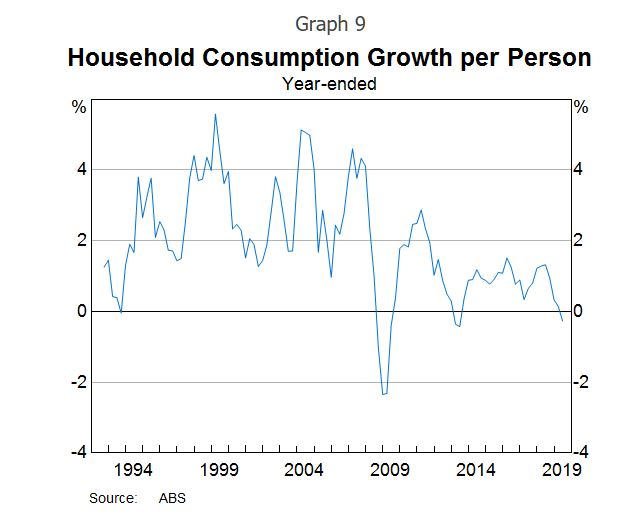

He went on to say over the past year, there has been no growth at all in consumption per person, which is an unusual outcome at a time when employment is growing strongly (Graph 9). An important part of the explanation here is that household disposable income has been increasing only slowly for an extended period, reflecting both subdued wage increases and strong growth in taxes paid.

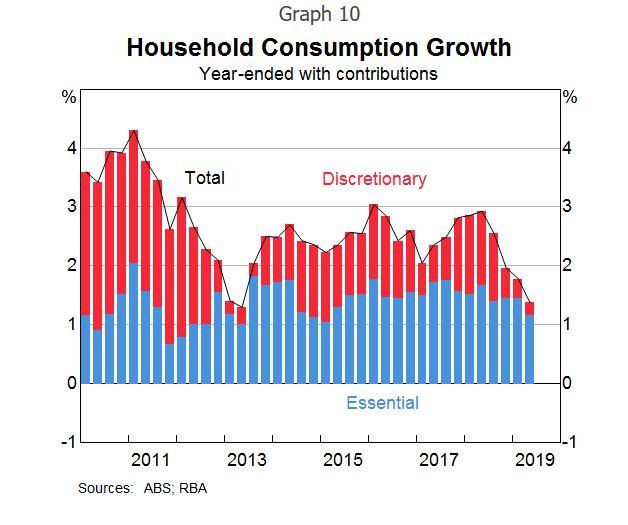

The persistence of slow growth in household income has led many people to reassess how fast their

incomes will increase in the future. As they have done this, they have also reassessed their spending,

particularly on discretionary items, which has been quite weak over recent times (Graph 10). Not

surprisingly, spending on household essentials has been much less affected.

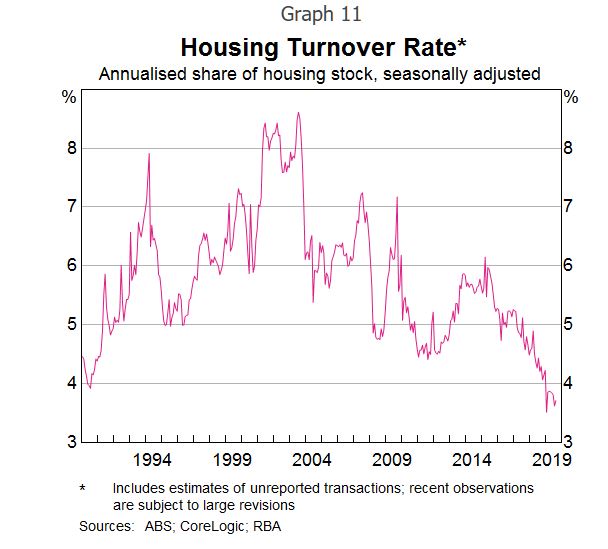

Another part of the explanation for weak growth in household spending is the adjustment in the housing

market. As housing prices have fallen, there has been a marked decline in housing turnover, with the

turnover rate having declined to the lowest level in more than 20 years (Graph 11). With fewer

of us moving homes, spending on new furniture and household appliances has been quite soft. So too has

expenditure on moving costs and real estate fees. More broadly, the correction in the housing market has

also affected the economy through its impact on residential construction activity.

Thus, we can join the dots, if banks lend more and stoke the housing market, this may reverse the weak consumer spending and drive the economy harder. This is of course why the Government and regulators are doing all they can to pull prices higher (though volumes remain very low, and the number of new listings have hardly moved).

And according to the ABC, more building firms are failing.

Statistics, provided by ASIC, show 169 NSW-based construction companies went into administration, receivership or a court-ordered shutdown in the June quarter — the highest number since the September quarter in 2015.

Over the whole 2018-19 financial year, 556 construction companies went under — 101 more than the previous financial year.

Yet, despite all this in a Q&A the Governor was asked if he was concerned about the recent developments in the housing market. Lowe said the RBA was not worried about the recent lift in dwelling prices and he does not expect credit growth to materially lift due to lower interest rates – meaning that the recent acceleration in the housing market will not be an impediment to a near term rate cut.

In fact the only point of resistance against looser lending and more credit is ASIC’s appeal against the recent ruling relating to HEM (Household Expenditure Measures) that found knowing a customer’s current living expenses was immaterial to deciding whether they could afford repayments on a loan.

In the most famous line of his judgment, Justice Perram found that

“Knowing the amount I actually expend on food tells one nothing about what that conceptual minimum [of how much one can spend without going into “substantial hardship”] is. But it is that conceptual minimum which drives the question of whether I can afford to make the repayments on the loan.”

ASIC commissioner Sean Hughes said the regulator felt compelled to

appeal after Justice Perram ruled that a lender “may do what it wants in

the assessment process”.

“The Credit Act imposes a number of legal obligations on credit providers, including the need to make reasonable inquiries about a borrower’s financial circumstances, verifying information obtained from borrowers and making an assessment of whether a loan is unsuitable for the borrower,” he said in a statement.

“ASIC considers that the Federal Court’s decision creates uncertainty as to what is required for a lender to comply with its assessment obligation, nor does ASIC regard the decision as consistent with the legislative intention of the responsible lending regime.

“For those reasons, ASIC will appeal to the Full Court of the Federal Court.”

If ASIC loses then the final drag on future credit growth will be blown away.

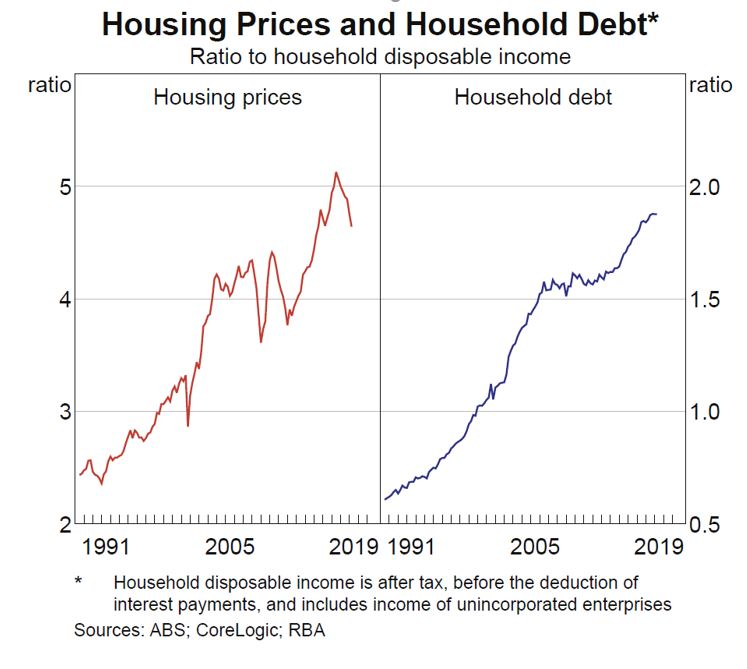

I have to say, I find this whole narrative very unconvincing. Remember home prices relative to income remain very stretched, the debt burden has never been higher, and yet people are being encouraged to borrow big, and help resurrect the housing market (and the economy), at any cost.

If rates are cut again, the flow of credit will rise (thanks to the APRA changes and heightened competition among lenders). And of course the main driver of this is that banks need lending growth to drive future profitability. But my own modelling suggests that as we approach the zero bounds, profitability will actually be squeezed some more. That said, we can see why it is that Mortgage Growth is The Only Game In Town. From Polys, to Regulators, to Lenders, they all want it. Household though will bear the consequences.

The Official Cash Rate (OCR) remains at 1.0 percent. The Monetary Policy Committee agreed that new information since the August Monetary Policy Statement did not warrant a significant change to the monetary policy outlook.

Employment is around its

maximum sustainable level, and inflation remains within our target range but

below the 2 percent mid-point.

Global trade and other

political tensions remain elevated and continue to subdue the global growth

outlook, dampening demand for New Zealand’s goods and services. Business

confidence remains low in New Zealand, partly reflecting policy uncertainty and

low profitability in some sectors, and is impacting investment decisions.

Global long-term interest

rates remain near historically low levels, consistent with low expected

inflation and growth rates into the future. Consequently, New Zealand interest

rates can be expected to be low for longer.

The reduction in the OCR

this year has reduced retail lending rates for households and businesses, and

eased the New Zealand dollar exchange rate.

Low interest rates and

increased government spending are expected to support a pick-up in domestic

demand over the coming year. Household spending and construction activity are

supported by low interest rates, while the incentive for businesses to invest

will grow in response to demand pressures.

Keeping the OCR at low

levels is needed to ensure inflation increases to the mid-point of the target

range, and employment remains around its maximum sustainable level. There

remains scope for more fiscal and monetary stimulus, if necessary, to support

the economy and maintain our inflation and employment objectives.

Summary record of

meeting

The Monetary Policy

Committee agreed the new information since the August Monetary Policy Statement

did not warrant a significant change to the monetary policy outlook.

The Committee noted that

employment remains close to its maximum sustainable level but consumer price

inflation remains below the 2 percent target mid-point.

The Committee members

discussed the initial impacts of reducing the OCR to 1.0 percent in August.

They were pleased to see retail lending interest rates decline, along with a

depreciation of the exchange rate.

The members anticipated a

positive impulse to economic activity over the coming year from monetary and

fiscal stimulus. The members noted that there remains scope for more fiscal and

monetary stimulus if necessary, to support the economy and our inflation and

employment objectives.

The Committee noted that,

while GDP growth had slowed over the first half of 2019, impetus to domestic

demand is expected to increase. Household spending and construction activity

are supported by low interest rates, while business investment should lift in

response to demand pressures.

The Committee expected

increasing demand to keep employment near its maximum sustainable level. Rising

capacity pressures and increasing import costs, higher wages, and pressure on

margins are expected to lift inflation gradually to 2 percent.

The Committee discussed the

long and variable lags between monetary policy decisions and outcomes.

The members noted several

key uncertainties affecting the outlook for monetary policy, where there was a

range of possible outcomes.

Global trade and other geopolitical

tensions remain elevated and continue to subdue the global growth outlook,

dampening demand for New Zealand’s goods and services.

Business confidence remains

low in New Zealand, partly reflecting policy uncertainty and low profitability

in some sectors, and is affecting investment decisions.

Fiscal policy is expected to

lift domestic demand over the coming year. However, any increase in government

spending could be delayed or it could have a smaller impact on domestic demand

than assumed.

Some members noted that

ongoing low inflation could cause inflation expectations to fall. Others noted

that this risk was balanced by the potential for rising labour and import costs

to pass through to inflation more substantially over the medium term.

The Committee discussed the

secondary objectives from the remit and remained comfortable with the monetary

policy stance.

The Committee agreed that

developments since the August Statement had not significantly changed the

outlook for monetary policy. They reached a consensus to keep the OCR at 1.0

percent and that, if necessary, there remains scope for more fiscal and

monetary stimulus.

Morningstar has low hopes for new banks like Volt, Xinja, 86 400 and Judo, which it says are at high risk of taking on low-quality debt in the pursuit of growth, via InvestorDaily.

In

a research report published this week, Morningstar analyst Nathan Zaia

said neobanks are unlikely to cause any disruption in the Australian

banking industry, which remains dominated by CBA, Westpac, NAB and ANZ.

“Volt,

86 400, Up, Xinja and Judo are just a few of the interestingly named

banks gaining media attention as ‘disruptors’ in the Australian banking

sector,” Mr Zaia said.

“It’s easy to be lured by a new website,

heavy marketing, new account discounts and a promise of offering

something different. But history has shown it can be extremely difficult

to build requited scale to run a profitable and sustainable bank.”

The analyst said competition from non-bank and digital banks have had limited effect on the banking landscape to date.

He

said a number of neobanks, focused on digital offerings, are growing

and while some are reporting large percentage growth rates in their loan

books, they have made only a minor dent in market share.

Mr Zaia

noted that digital-only banking is nothing new in Australia, pointing to

ING Bank Australia, which has held a banking licence since 1994 and

amassed a total loan book of $60 million and $47 million in deposits.

Morningstar stated that without the balance sheet and technology to

leverage tech spend, neobanks will struggle to be as disruptive as ING.

“There

are significant risks to the challenger banks and fintech start-ups

that we think the market is underestimating,” Mr Zaia said.

“Chasing

growth in lending often comes at the expense of credit quality, and in a

downturn, spectacular growth can quickly give way to mounting bad

debts,” he said, pointing to numerous boom and bust examples in

Australia.

CBA acquired Bankwest in 2008 after its UK parent at

the time, HBOS, ran into financial trouble during the GFC. Mr Zaia said

the bank incurred hefty impairments following a period of rapid

expansion and took on high-risk loans that other lenders did not want.

“Westpac’s acquisition of RAMS Home Loans followed another notable industry failure,” the analyst said.

“In

2007 the RAMS Home Loans business model of lending to low-income

earners using cheaply sourced debt in the US came unstuck when credit

markets froze and it was unable to roll out $5 billion in commercial

paper.”

Mr Zaia added that prioritising low growth over credit

quality has also caught out regional bank Suncorp, which required a

capital raising after incurring large corporate and commercial property

impairments.

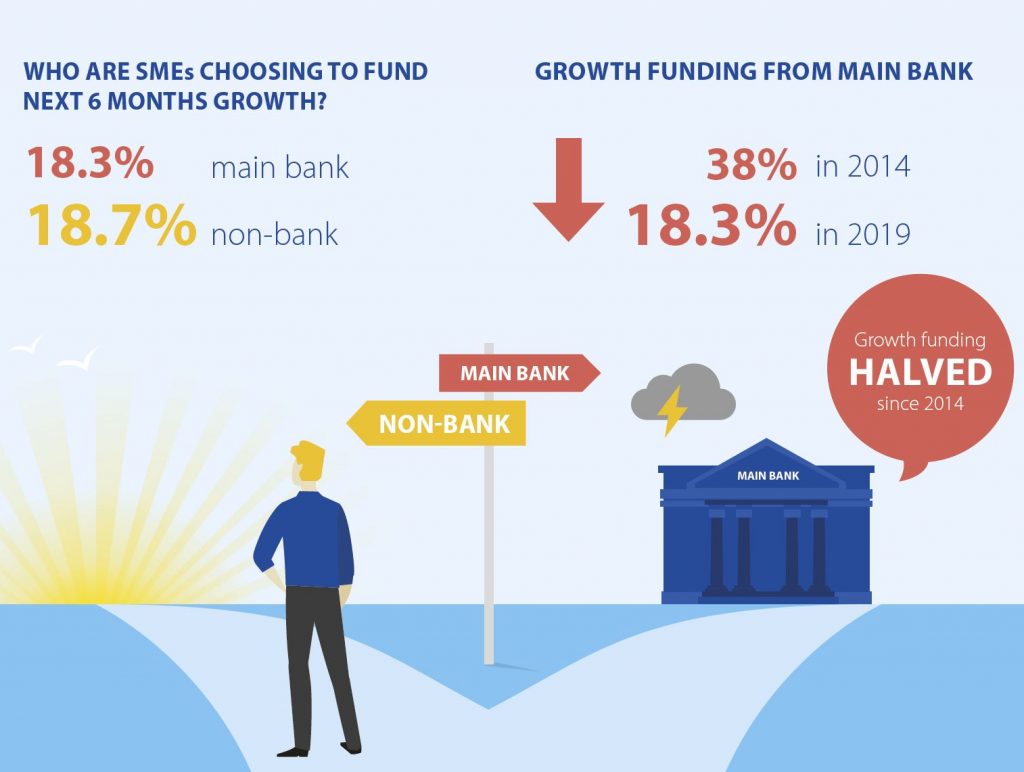

A new trend has emerged in the SME lending space, with Australian small businesses more likely to use a non-bank to fund growth rather than their main bank, according to a national survey, via Australian Broker.

Small business owners’ reliance on non-banks is the highest it’s ever been, with 18.7% of SMEs planning to fund revenue growth with such a lender, as charted in the September 2019 SME Growth Index commissioned by Scottish Pacific and drawing data from over 1,000 businesses.

Conversely, business owners planning to fund their growth via their

main bank has halved, dropping from 38% in the first year of reporting

in 2014 to 18.3% in the most recent data.

The main reason given for turning away from banks, cited by 21.3% of the SMEs, was avoiding having to use property as security against new or refinanced loans, up from 18.7% in September 2018.

Other considerations contributing to the gravitation towards

non-banks included reduced compliance paperwork (19.8%), short

application times (17.1%), royal commission disclosures (8.8%) and

banks’ credit appetite (6.9%).

Of the SME owners relying on non-bank funding, 77% utilise invoice

finance, 23% merchant cash advances, 10% peer to peer lending, 9%

crowdfunding and 5% other online lending.

Just 2.6% of those surveyed indicated they would not consider using a non-bank lender – down from 4.0% last year.

“[However], the SME sector still has a long way to go in taking

advantage of the alternatives available to them,” said Peter Langham,

Scottish Pacific CEO.

“Some business owners remain unaware of funding alternatives. [They]

are aware of non-bank funding, but don’t fully understand how it works.

“They are too busy to research it, so put this in the ‘too hard’

basket. When they can’t secure bank funding, they just tip their own

money in to fund growth.”

For growth SMEs, almost twice as many as in H1 2018 say their cash flow is worse or significantly worse (21.2%, up from 12.3%). At the same time, non-growth SMEs reporting worsening cash flow has increased to 17.6%, up from 10% in H1 2018.

According to the survey, 83% of business owners plan to stimulate revenue growth with their own funds.

The main message from The RBA Governor tonight on the global economy is that while it is still growing reasonably well, the risks are increasingly tilted to the downside. The main source of these downside risks are geopolitical developments in many parts of the world. These developments are creating considerable uncertainty and this uncertainty is causing businesses to reconsider their spending plans. This is making the international environment more challenging for us.

On the Australian economy, there are two main messages.

The first is that after having been through a soft patch, a gentle turning point has been reached.

While we are not expecting a return to strong economic growth in the near term, we are expecting growth

to pick up. Against this backdrop, the main source of domestic uncertainty continues to be the strength

of household spending.

The second message is a longer-term one. And that is the fundamental factors underpinning the

longer-term outlook for the Australian economy remain strong. One of the ongoing challenges we face as a

country is to capitalise on those strong fundamentals.

The Global Economy

This first graph shows global economic growth and the International Monetary Fund’s (IMF)

forecasts for the next few years (Graph 1). Looking at this graph, one might ask why the concern:

global growth has been stable and reasonable over recent times and the IMF is forecasting this to

continue over the next couple of years. If this forecast were to come to pass, that would make for

12 years of solid growth.

Graph 1

Looking at labour markets, one might also ask why the concern. Unemployment rates in most advanced

economies are the lowest they have been in many decades, and businesses are finding it more difficult to

fill jobs (Graph 2). These tighter labour markets are finally translating into stronger wages

growth, with wages now increasing at close to the rates seen before the financial crisis in some

countries. With inflation remaining low, this pick-up in wage growth is translating into real wage

increases and strong growth in household spending.

Graph 2

So why the concern?

The answer is the increased downside risks generated by various geopolitical developments. The most

prominent of these are the trade and technology disputes between the United States and China. Others

include: the Brexit issue, developments in the Middle East, the problems in Hong Kong and the tensions

between Japan and South Korea.

The US–China disputes, in particular, are having a disruptive effect on international trade

flows. Over the past year there has been no growth at all in international trade, despite the global

economy growing at a reasonable rate (Graph 3). This weakness on the trade front is flowing through

to factory output, with growth in industrial production slowing considerably.

Graph 3

More broadly, though, the geopolitical concerns are creating considerable uncertainty about the future.

This can be seen in measures of economic policy uncertainty constructed from news stories in leading

media around the world (Graph 4).

Graph 4

In the face of this uncertainty, it is not surprising that many businesses are preferring to wait

before committing to significant investments; they are inclined to sit on their hands for a while and

see how things play out. This is evident in the surveys of business investment intentions, which have

fallen considerably (Graph 5). The effect is also evident in June quarter GDP figures, with GDP

declining in Germany, the United Kingdom and Singapore.

Graph 5

A particular concern is that if this uncertainty continues, businesses might decide not only to defer

investment, but to also defer hiring. Of course, it is also possible that some of these uncertainties

will be resolved. If this were to happen, the global economy could grow quite strongly as firms caught

up on their capital spending in an environment of easy financial conditions.

Notwithstanding this possibility, as the downside risks have come more clearly into focus, there has

been a marked shift in the outlook for monetary policy globally. Almost all major central banks are

expected to ease monetary policy over the year ahead, with the United States Federal Reserve and the

European Central Bank having already moved in this direction (Graph 6). Given that inflation is low

– and forecast to remain low – investors are also expecting central banks to maintain very

accommodative settings of monetary policy for years to come.

Graph 6

This expectation has had a major effect on long-term bond yields around the world. In Europe and Japan,

investors are paying governments to hold their money for them (Graph 7). The Swiss Government, for

example, can borrow for 30 years at a negative interest rate of 0.5 per cent. For the

world as a whole, around a quarter of the total stock of government bonds on issue has negative yields.

And where yields are in positive territory, they are at very low levels and in many cases at the lowest

on record.

Graph 7

All this is making for a challenging international environment.

The Australian Economy

I would now like to move to the Australian economy.

Over recent times, our economy has been going through a soft patch. Over the year to June, GDP grew by

just 1.4 per cent, which is the slowest year-ended growth for some years (Graph 8).

We did not expect this slowdown, so it has come as a bit of a surprise.

Graph 8

It is important, though, that we keep things in perspective. The economic expansion in Australia has

now been running for 28 years. That is quite an achievement. Over such a long expansion, there are

going to be ebbs and flows in growth. There are also going to be periods where growth is stronger than

expected – as it was in the first half of 2018 – and other periods, like now, where growth

is weaker than expected.

With the benefit of hindsight, there are a few factors that help explain the slowing in the Australian

economy over the past year.

One is the international developments that I spoke about earlier. While Australia has been less

directly affected by the US–China trade disputes than have many other countries, there is an

indirect effect through slower global growth and increased global uncertainty.

A second and more important factor is weak consumption growth.

Over the past year, there has been no growth at all in consumption per person, which is an unusual

outcome at a time when employment is growing strongly (Graph 9). An important part of the

explanation here is that household disposable income has been increasing only slowly for an extended

period, reflecting both subdued wage increases and strong growth in taxes paid.

Graph 9

The persistence of slow growth in household income has led many people to reassess how fast their

incomes will increase in the future. As they have done this, they have also reassessed their spending,

particularly on discretionary items, which has been quite weak over recent times (Graph 10). Not

surprisingly, spending on household essentials has been much less affected.

Graph 10

Another part of the explanation for weak growth in household spending is the adjustment in the housing

market. As housing prices have fallen, there has been a marked decline in housing turnover, with the

turnover rate having declined to the lowest level in more than 20 years (Graph 11). With fewer

of us moving homes, spending on new furniture and household appliances has been quite soft. So too has

expenditure on moving costs and real estate fees. More broadly, the correction in the housing market has

also affected the economy through its impact on residential construction activity.

Graph 11

A third factor contributing to the slower growth has been the drought.

Across the Murray-Darling Basin, including here in the Northern Tablelands, farmers have faced

extremely dry conditions. Indeed, as indicated in this graph, in some areas conditions have been the

driest on record (Graph 12). Reflecting this, farm output in Australia has fallen for the past two

years and there has been a sharp drop in farm income as farmers have had to cope with the increased

costs for obtaining feed and water. These difficult conditions have contributed to the weakness in

overall household incomes and consumption, and the effects are particularly felt in regional

communities. The drought has also put upward pressure on food prices over the past year, particularly

for bread, milk and meat. We are all hoping that the drought breaks soon.

Graph 12

Even after accounting for these three factors – the slowdown overseas, weak growth in household

disposable incomes and the drought – part of the slowing in the Australian economy remains

unexplained. This is especially so taking into account the labour market data, which continue to paint a

stronger picture of the economy than the GDP data.

Over recent times, employment growth has been stronger than was expected. Over the past year, the

number of people with a job increased by 2½ per cent (Graph 13). Reconciling this

with GDP growth of just 1½ per cent remains a challenge, because, normally, output growth

exceeds employment growth, rather than falls short. We are seeking to understand what is going on here.

It is possible that it is just measurement noise, but we can’t yet rule out something more

structural.

Graph 13

The other striking feature of the labour market over recent times has been a large increase in labour

supply. In particular, there has been a material lift in the labour force participation by women and by

older Australians (Graph 14). As a result, the increase in labour supply has more than outstripped

the increase in labour demand. Reflecting this and despite the strong employment growth, the

unemployment rate has moved higher since the start of the year to 5¼ per cent.

Graph 14

This increase in labour supply is a positive development, but it does mean that it is proving quite

difficult to generate a tight labour market with the flow-on consequence that wage increases remain

subdued. Over the past year, the Wage Price Index increased by just 2.3 per cent

(Graph 15). This is a pick-up from the rates of recent years, but the lift in wages growth

looks to have stalled recently. Another relevant factor here is the ongoing caps on wage increases in

the public sector.

Graph 15

Low wages growth is one of the factors contributing to low inflation outcomes. Over the year to June,

inflation was 1.6 per cent, in both headline and underlying terms (Graph 16). Another

contributing factor is the adjustment in the housing market, with rents increasing at the slowest rate

in decades and declines being recorded in the price of building a new home in some cities

(Graph 17). Another factor is various government initiatives to address cost-of-living pressures,

with these initiatives pushing down inflation in administered prices. The price rises for utilities are

also much lower than over recent years. Working in the other direction, the drought and the

depreciation of the exchange rate have been pushing up retail prices over the past year.

Graph 16

Graph 17

Looking forward, there are some signs that, after a soft patch, the economy has reached a gentle

turning point. This is evident in the fact that GDP growth over the first half of this year was stronger

than it was over the second half of last year (Graph 8). We are expecting a further modest pick-up

in the quarters ahead.

This outlook is supported by a number of developments, including lower interest rates, the recent tax

cuts, the depreciation of the Australian dollar, ongoing spending on infrastructure, the stabilisation

of the housing markets in some cities and a brighter outlook for the resources sector. It is reasonable

to expect that, together, these factors will see growth in the Australian economy return to around its

trend rate next year, although there are some obvious risks to this outlook.

One factor that should help is an expected pick-up in household disposable income. Many households are

currently receiving larger tax refunds due to the low and middle income tax offset. These payments will

boost aggregate household income by 0.6 per cent this year. Past experience suggests that

around half of these tax refunds will be spent over coming quarters. Household disposable income is also

being boosted by lower interest rates, although the effect is uneven across the community, with lower

rates reducing the income of those households who rely on interest income. Household spending should

also be supported by an increase in housing turnover. Working in the other direction, though, is a

further contraction in residential construction activity.

Another positive element is likely to come from the resources sector. Mining investment is expected to

increase over the next year, after having declined for six years as the LNG investment boom wound

down (Graph 18). Mining companies are increasing their investment not only to sustain their current

production levels but, in some cases, to expand capacity as well. There has also been a pick-up in

exploration activity. To be clear, we are not predicting a return to boom-time conditions in the

resources sector. But we are predicting better times for the sector ahead.

Graph 18

Business investment elsewhere in the economy is also expected to move higher. Earlier I discussed how

uncertainty globally is affecting the outlook for investment in many countries. Fortunately, we

don’t see the same spike in the measure of policy uncertainty in Australia that I showed in the

earlier graph for the world economy. There has, however, been some softening in measures of business

conditions – from well above average to around average.

The investment outlook is being supported by a solid pipeline of infrastructure projects. This ongoing

investment in infrastructure is not only supporting demand in the economy at a time when this is needed,

but it is also adding to the supply capacity of the economy and directly improving people’s lives,

including through providing better services and reducing transport congestion.

Together, it is reasonable to expect that these various factors will see annual growth pick up from

here. Apart from the international uncertainties, the main source of uncertainty around this outlook

continues to be the strength of household spending. It remains the case that a sustained pick-up in

household spending will require faster growth in household incomes than we have seen over recent

times.

As we grapple with these issues, it is important that we do not lose sight of the fact that the

Australian economy has strong fundamentals.

Australia is fortunate in having enviable endowments of natural resources, both in terms of minerals

and agricultural land. We have a reputation as a highly reliable supplier and a producer of high-quality

clean food. We also have close links with the rapidly growing countries of Asia. Three of the four most

populous countries in the world – China, India and Indonesia – are in our neighbourhood.

And our ties with these countries are strengthened by the many people from there who live, work and

study in Australia.

Our demographics are also reasonably favourable. Our population is aging less quickly than that of many

other advanced economies. The population is also growing relatively rapidly for an advanced economy

– 1.7 per cent a year, compared with 0.6 per cent in the United States and

declining populations in some countries in north Asia and Europe. Immigration has been a strong

contributor to this: almost half of us were born overseas or have at least one parent who was born

overseas. While we have struggled to meet the infrastructure needs that come with this growing

population, it does bring a dynamism that is not easily matched in countries with declining

populations.

We also have a highly talented, flexible and adaptive workforce. We have strong public institutions, a

well-established macroeconomic framework, and the rule of law is respected. There is also a demonstrated

record of responsible fiscal policy and low public debt. And, finally we benefit from having both a

flexible exchange rate and a flexible labour market. So, our fundamentals are strong.

The challenge we face is to fully capitalise on these fundamentals. If we can do this then I am

confident that we can, once again, experience strong growth in real incomes in Australia.

Monetary Policy

I would like to finish with some remarks about monetary policy.

As you would be aware, the Reserve Bank Board lowered the cash rate in June and July to a new low of

1 per cent. Financial markets are pricing in further reductions in the cash rate over the next

year.

Our decisions – and the expectations of investors about the future – reflect both

international and domestic factors.

On the international front, as I discussed earlier, interest rates around the world are low and they

are moving lower. There are many reasons for this, but the central reason is that the global appetite to

save is elevated relative to the global appetite to use those savings to invest in new productive

capital. When lots of people want to save and there is not much demand for those savings, savers earn

low returns.

We live in an interconnected world, which means that we cannot completely insulate ourselves from

long-lasting shifts in global interest rates. Our floating exchange rate gives us a degree of

monetary independence, but we can’t ignore structural shifts in global interest rates. If we did

seek to ignore these shifts, our exchange rate would appreciate, which, in the current environment,

would be unhelpful in terms of achieving both the inflation target and full employment.

As I have spoken about on other occasions, the key to more normal interest rates globally is addressing

the factors that are leading to a depressed appetite to invest relative to the appetite to save. Whether

or not this will happen, time will tell. But as a small open economy, we have to take the world and

global interest rates as we find them.

On the domestic front, there has been an accumulation of evidence over recent times that the economy

can sustain lower rates of unemployment and underemployment than previously thought likely. The

flexibility of labour supply also means that strong rates of employment growth can be sustained without

inflation becoming a problem. These are both positive developments.

Inflation has been below the 2–3 per cent medium-term target range for some time now

for the reasons that I spoke about earlier. Looking ahead, inflation is expected to pick up, but to

remain below the midpoint of the target range for some time to come.

The decisions to ease monetary policy in June and July were taken to help make more assured progress

towards full employment and the inflation target. Further monetary easing may well be required. While we

are at a gentle turning point and expect growth to pick up, the strength and durability of this pick-up

remains to be seen.

Regardless of the short-term outlook for monetary policy, the point about the solution to low global

rates is relevant here in Australia too. We will all be better off if businesses have the confidence to

expand, invest, innovate and hire people. Given Australia’s strong fundamentals, this is not out of

our reach, but it does require constant effort.

At our Board meeting next week, we will again take stock of the evidence. It is nevertheless likely

that an extended period of low interest rates will be required in Australia to make progress in reducing

unemployment and achieving more assured progress towards the inflation target. The Board is prepared to

ease monetary policy further if needed to support sustainable growth in the economy, make further

progress towards full employment, and achieve the inflation target over time.