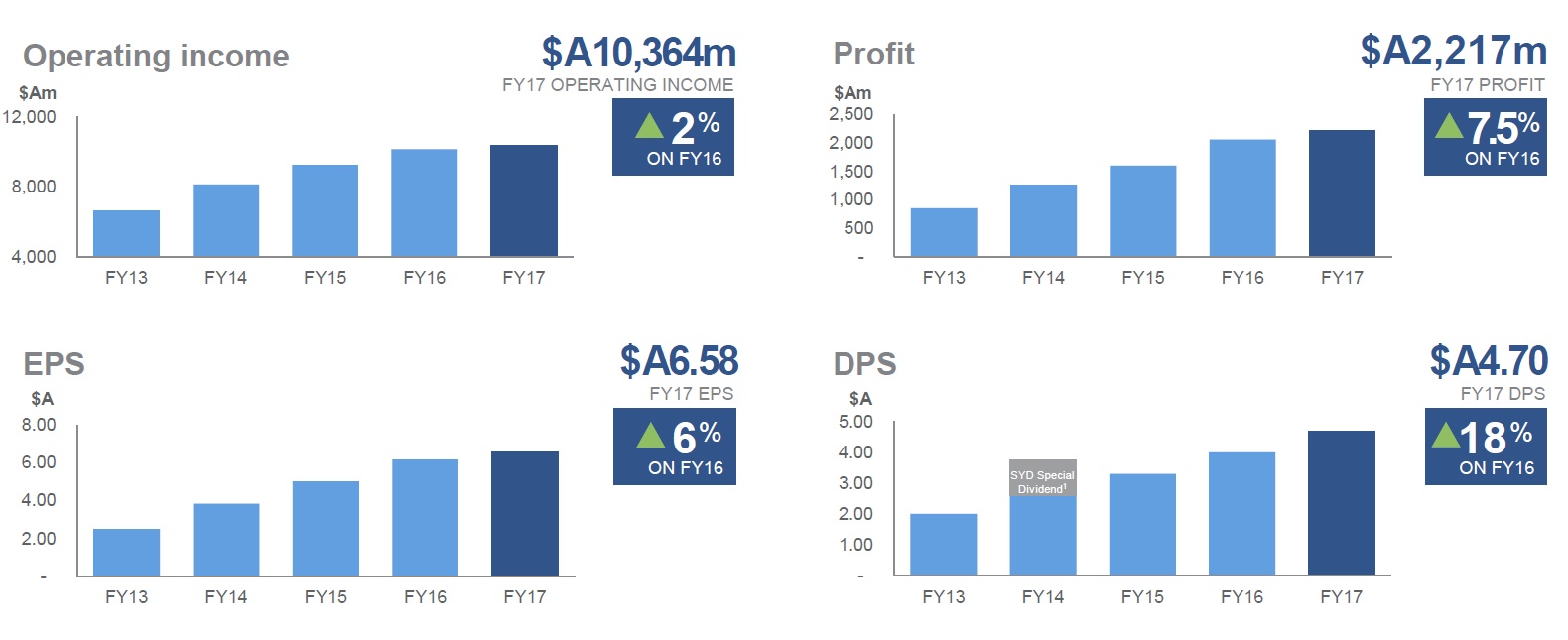

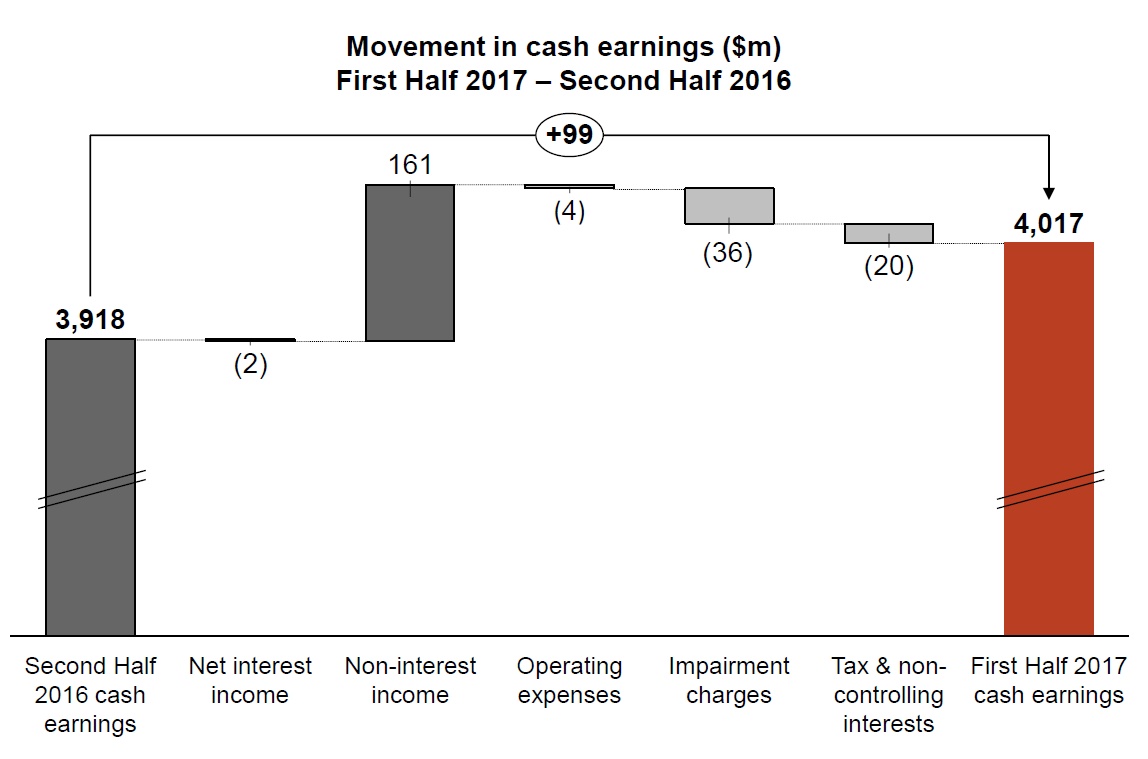

Westpac has declared a 1H17 Statutory net profit of $3,907 million, up 6% compared with 1H16, with Cash earnings $4,017 million, up 3%.

Most of the increase in net operating income was due to a higher Institutional Bank contribution from participation in a number of significant customer transactions and from stronger markets income. This strong markets result relies on non-customer trading, and may be hard to replicate. They were impacted by higher insurance claims mostly associated with Cyclone Debbie, and higher delinquencies with a $44 million rise in impairment charges in the consumer book.

Most of the increase in net operating income was due to a higher Institutional Bank contribution from participation in a number of significant customer transactions and from stronger markets income. This strong markets result relies on non-customer trading, and may be hard to replicate. They were impacted by higher insurance claims mostly associated with Cyclone Debbie, and higher delinquencies with a $44 million rise in impairment charges in the consumer book.

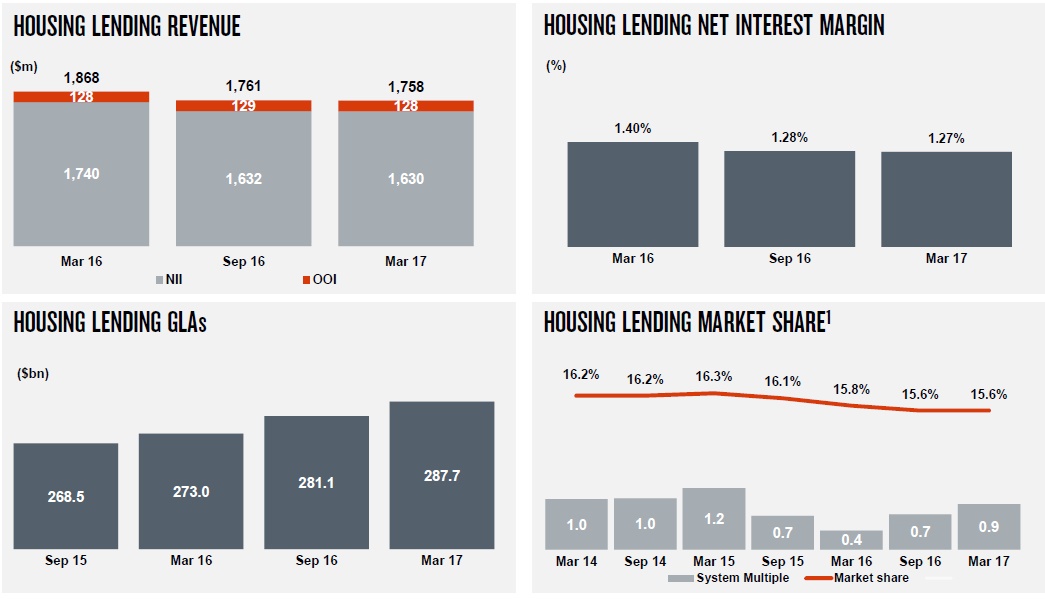

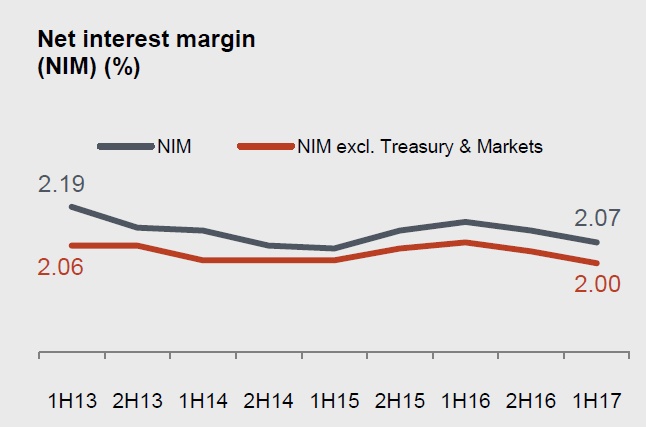

Net interest income increased $136 million or 2% compared to First Half 2016, with total loan growth of 4%, primarily from Australian housing which grew 6%.

However net interest margin is under pressure, and has declined 7 basis points over the past 12 months, of which 4 basis points was in 1H17. The consumer bank fell 6 basis points. Loan repricing may help in the 2H17.

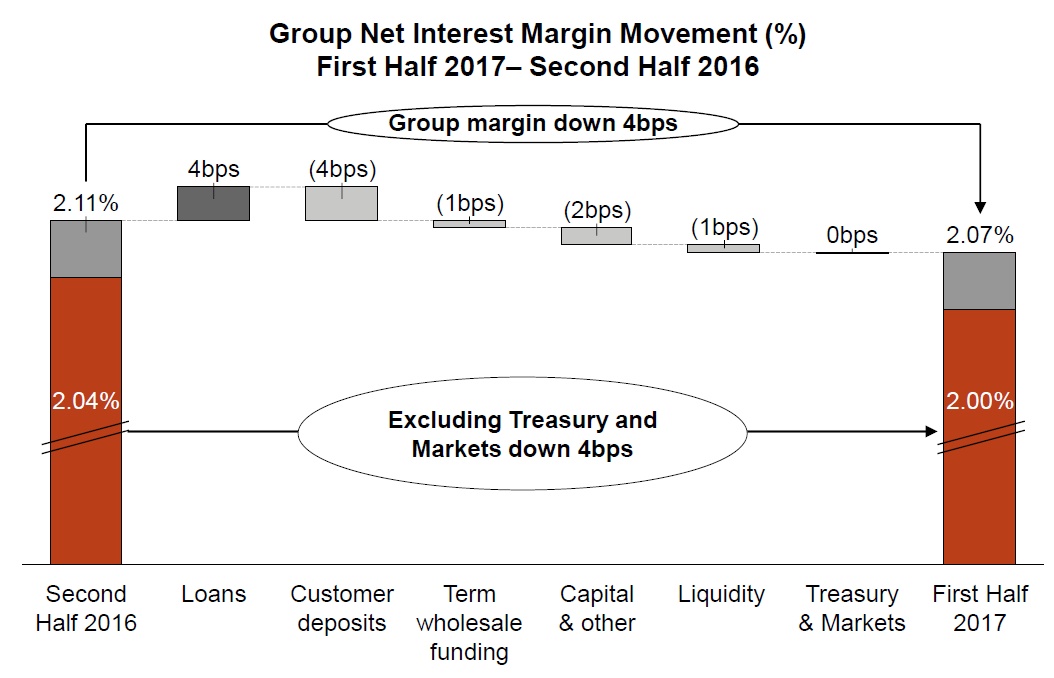

Group net interest margin was 2.07%, a decrease of 4 basis points from Second Half 2016. Key features included:

Group net interest margin was 2.07%, a decrease of 4 basis points from Second Half 2016. Key features included:

- 4 basis point increase from loan spreads. This reflected loan repricing mostly in Australian mortgages, including repricing of interest-only and investor loans. These increases were partly offset by competition;

- 4 basis point decrease from customer deposit spreads, driven by the full period impact of increased competition for term deposits in 2016 (3 basis points) and the continuing impact of lower interest rates on the hedging of transaction deposits;

- 1 basis point decrease from term wholesale funding costs reflecting an increase in Additional Tier 1 and Tier 2 capital balances and the higher costs of these instruments;

- Capital and other decreased 2 basis points primarily from the impact of lower interest rates; and

- 1 basis point decrease from liquidity, reflecting the increased holdings of third party liquid assets to meet the LCR requirement. This was partly offset by a lower CLF fee following a $9.5 billion reduction to the CLF from 1 January 2017.

Cash earnings was per share 119.8 cents, up 1% and the cash return on equity (ROE) was 14%, at the upper end of 13-14% range.

Cash earnings was per share 119.8 cents, up 1% and the cash return on equity (ROE) was 14%, at the upper end of 13-14% range.

Expenses are well controlled (up 1% over the year) and included a productivity saving of $118m with an expense ratio of 41.7%.

Impairments were down (15bps of loans) down 26% over year to $493 million as 1H16 included additional provisions for a small number of larger names. There were workouts of some larger facilities in the Institutional Bank and NZ.

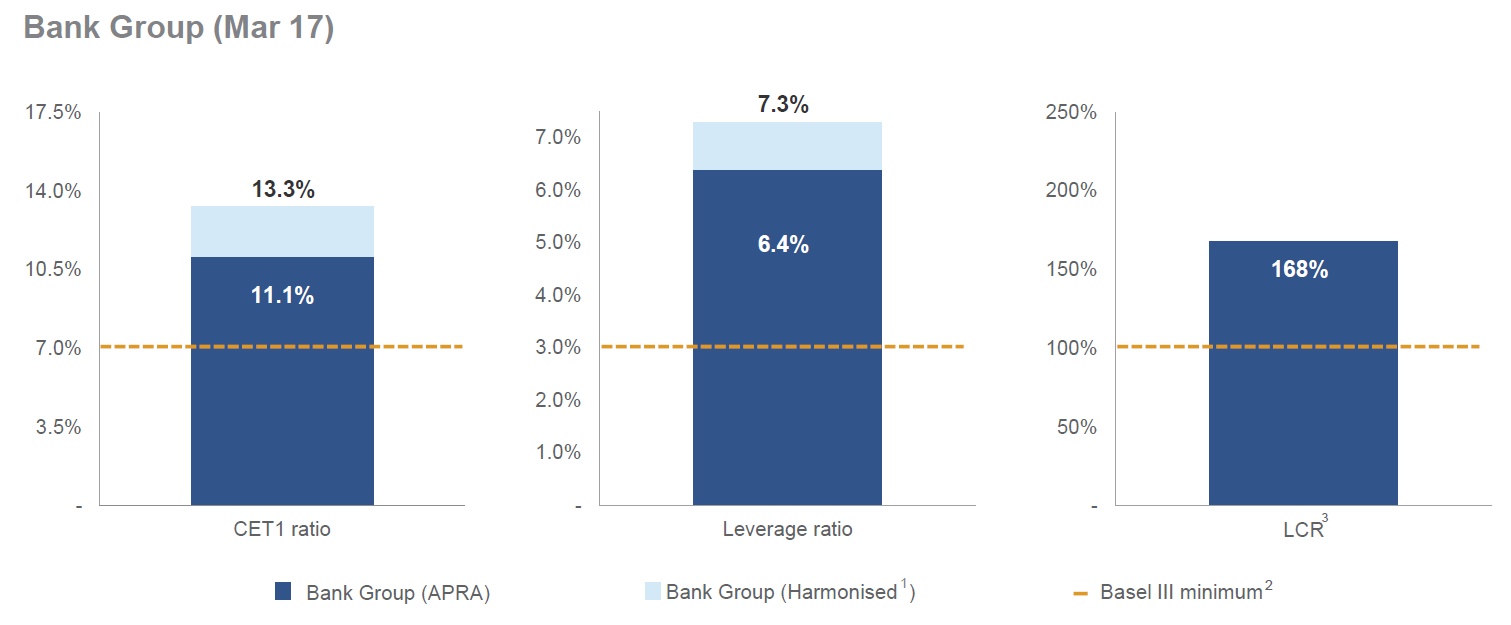

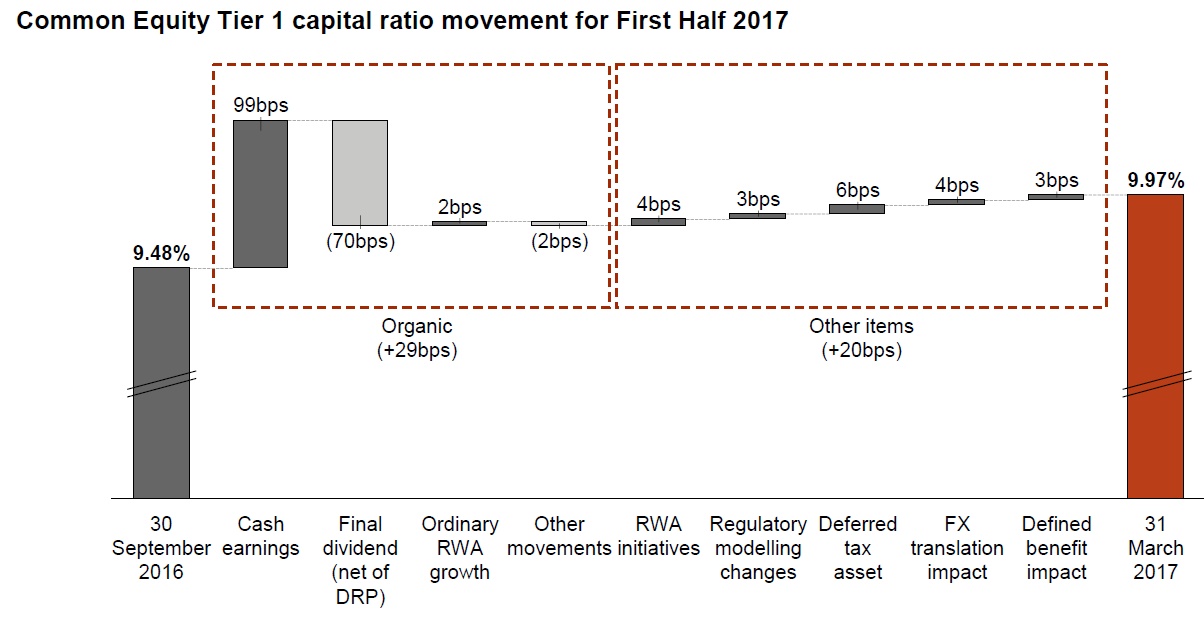

They further strengthened their Common equity Tier 1 capital ratio of 10.0%

Organic capital generation of 29 basis points included:

Organic capital generation of 29 basis points included:

- First Half 2017 cash earnings of $4.0 billion (99 basis points increase);

- The 2016 final dividend payment, net of DRP share issuance (70 basis points decrease);

- Ordinary RWA was modestly lower (excluding FX movements, RWA initiatives and modelling changes), a 2 basis point increase; and

- Other movements, decreased the CET1 capital ratio by 2 basis points.

Other items increased the CET1 capital ratio by 20 basis points:

- RWA initiatives including management of unutilised limits reduced RWA by $1.6 billion (4 basis points increase);

- Regulatory modelling changes (discussed further below) reduced RWA by $1.0 billion (3 basis points increase);

- Reduction in the deferred tax asset (6 basis points increase);

- The impact of foreign currency translation (4 basis points increase), mostly related to NZ$ lending; and

- A decrease in the accounting obligation for the defined benefit pension plan primarily reflecting higher discount rates used to value defined benefit liabilities (3 basis points increase).

They announced a 94 cents per share interim, fully franked dividend, which is unchanged from last period.

Looking at the divisional splits

Consumer Bank

Consumer Bank

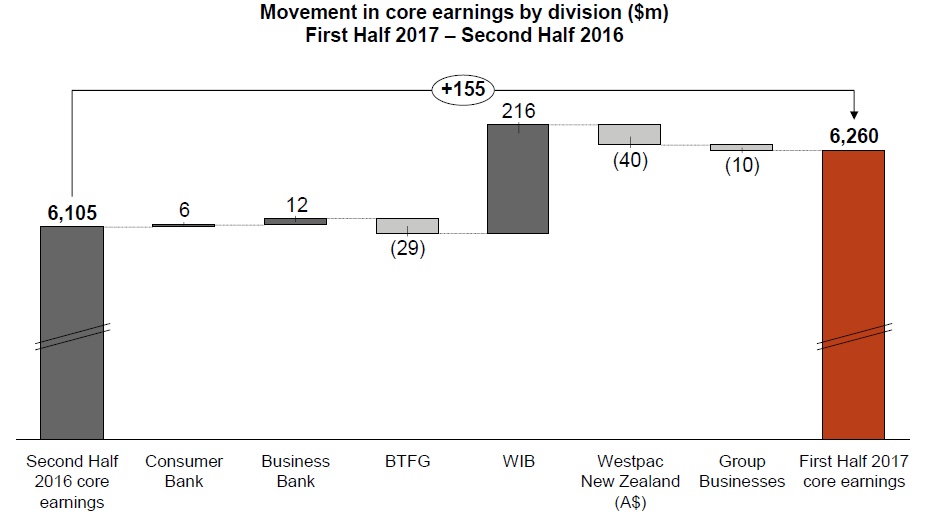

Cash earnings of $1,511 million was 2% lower than Second Half 2016 with the decline primarily due to a $44 million rise in impairment charges. While asset quality remains sound, higher delinquencies – including from

changes in the reporting of facilities in hardship – led to the increase in impairment charges. Core earnings were relatively flat over the period (up $6 million) as were most of its components, with operating income up $2 million and expenses declining $4 million. The division recorded disciplined growth with mortgages rising 2% and other lending slightly lower.

Customer deposit growth was solid, up 3% supported by a 2% rise in customers and a focus on deepening relationships by growing transaction accounts. Balance sheet growth, however, was largely offset by a 6 basis point decline in net interest margin. The margin decline was mostly due to competition for lending and higher funding costs, particularly across term deposits. As a result of these movements, net interest income was up $12 million. Non-interest income was $10 million lower mostly from reduced cards related income.

Productivity continues to be a significant focus with costs broadly unchanged over the half and the expense to income ratio continuing to fall. A range of initiatives contributed to the improved efficiency including the further digitisation of manual processes such as: changing PINs online, enhancing the origination of personal loans, and improving access to key mobile banking transactions. Improving customers’ digital access contributed to a net reduction of 26 branches over the half.

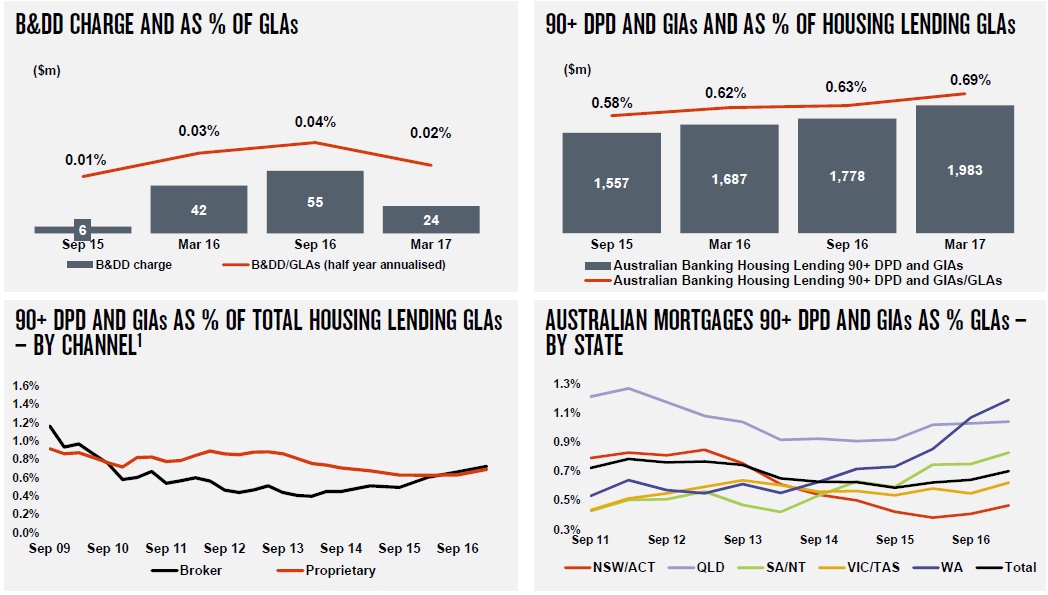

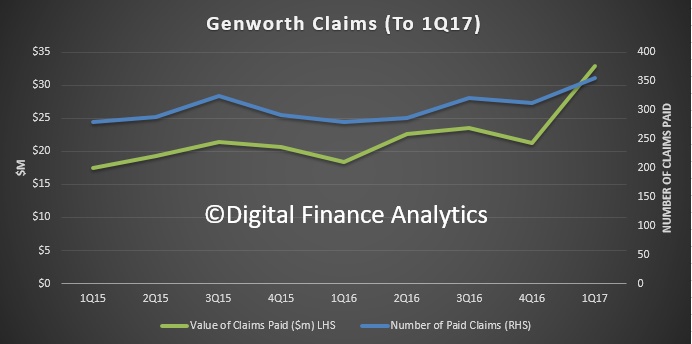

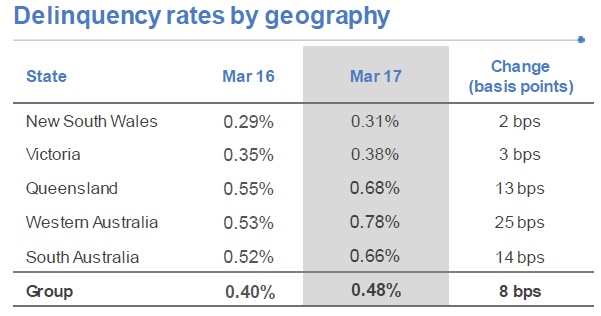

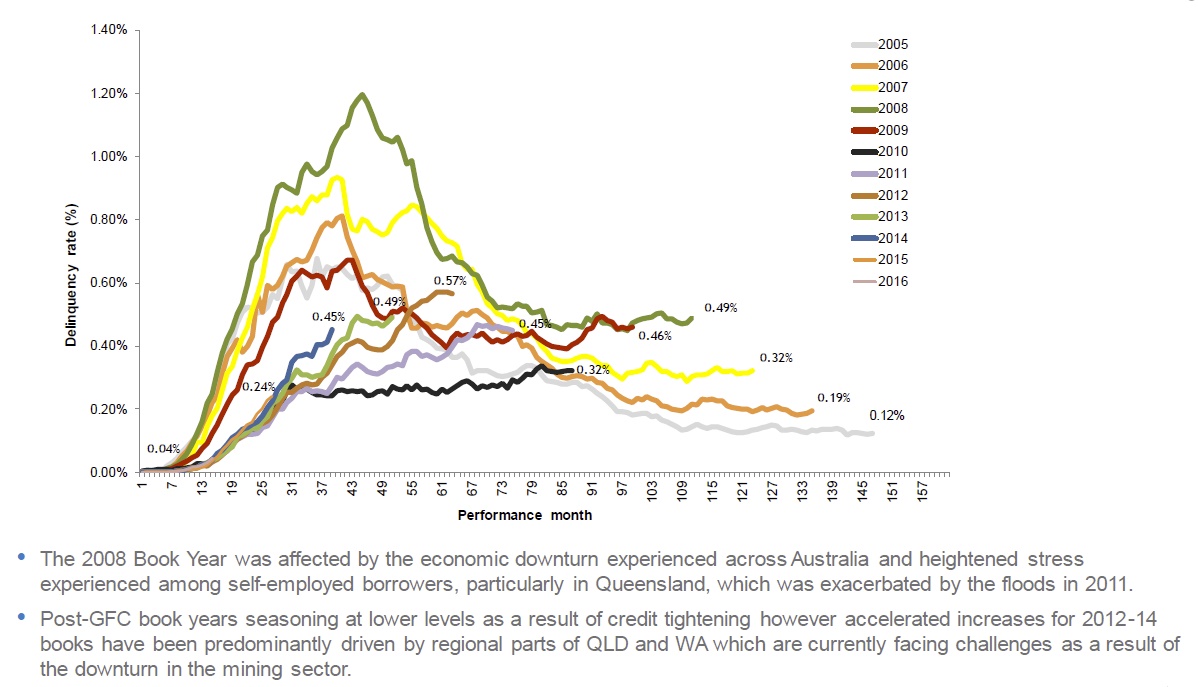

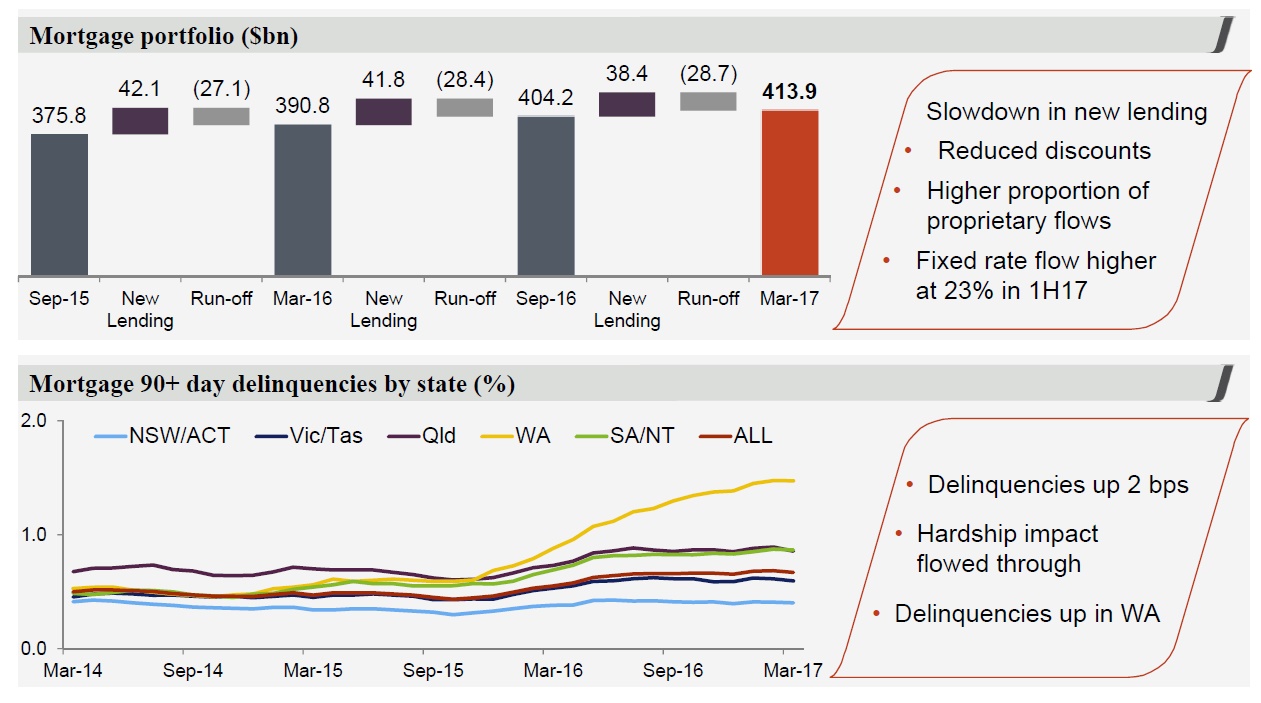

Australian mortgages accounts for 62% of group loans. They showed a 2 basis point rise in delinquencies, with a rise in WA. The number of consumer properties in possession rose from 261 in Sept 16 to 382 in Mar 17. Investment property 90+ day delinquencies rose from 38 basis points in Mar 16, to 47 basis points in Mar 17. Loss rates remain at 2 basis points.

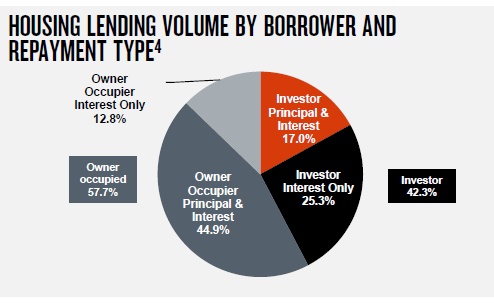

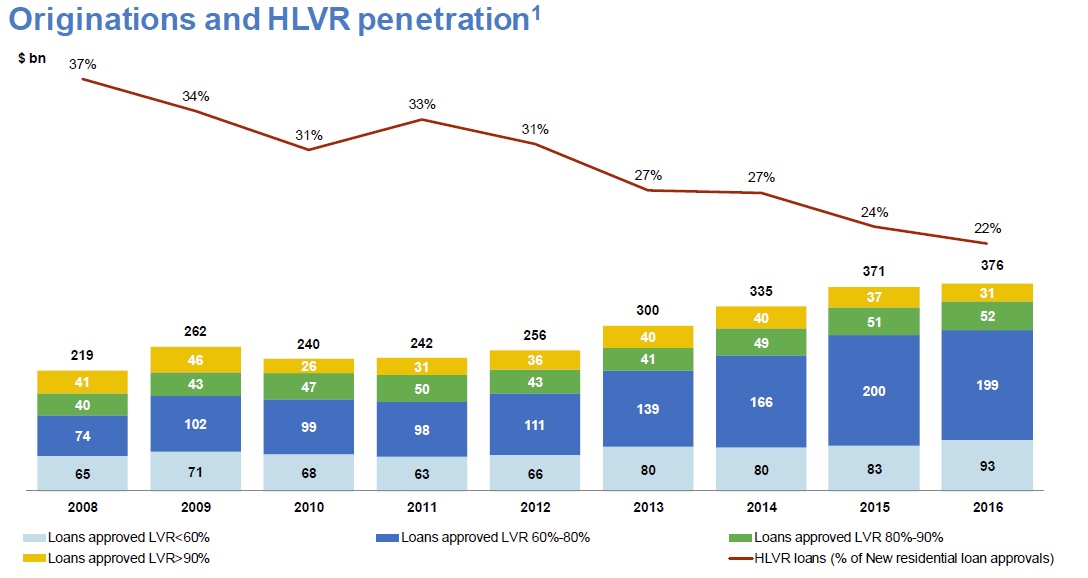

They said that interest-only represented 46% of flow in 1H17 and 50% of the total mortgage book. That said, the proportion of current drawdowns that are interest-only has already fallen into the mid-30s of total flow, remembering the APRA target of no more than 30% by September.

They said that interest-only represented 46% of flow in 1H17 and 50% of the total mortgage book. That said, the proportion of current drawdowns that are interest-only has already fallen into the mid-30s of total flow, remembering the APRA target of no more than 30% by September.

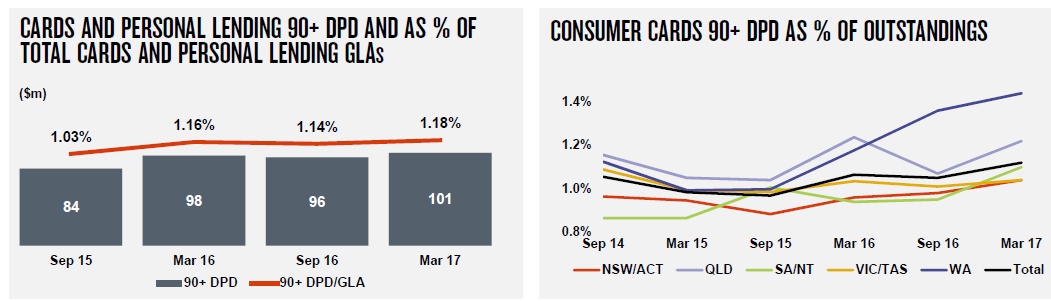

They also reported higher delinquency rates in their unsecured consumer books, with 90+ day up from 1.17% in Sept 16 to 1.63% in Mar 17. 28 basis points reflect an adoption of APRA hardship policy adopted across Westpac’s Australian unsecured portfolios.

Business Bank

Cash earnings of $1,008 million was $9 million, or 1% higher than Second Half 2016. The result was supported by higher fee income, targeted loan growth, and efficiency gains from digitisation and simplification initiatives. The division took a disciplined approach to growth in the half choosing to grow in sectors such as services and in SME and reducing exposure to some lower returning sectors including asset finance and commercial property. As a result, lending was up less than $1 billion (1%). Deposits grew 1%, mostly from working capital balances (up 4%) as the division focused on broadening relationships. Fee income was also higher mostly from a rise in line fees.

Expenses were up 1%, mostly from increased technology and investment including expanding the use of the division’s online origination platform and the continued roll out of new payment technologies. These increases

were partially offset by improved efficiencies including from the greater use of digital and refining the banker to customer ratio across segments. Impairment charges were flat, reflecting higher provisions in the auto loan portfolio, mostly related to a rise in delinquencies from changes in hardship reporting, offset by a lower impairment provisions for other business lending.

BT Financial Group

BTFG delivered a sound performance in a challenging environment, with good increases in funds, strong volume growth in lending and deposits and disciplined expense management. FUM and FUA balances were up 14% and 4% respectively while Life in-force premiums were up 6%.

Despite these benefits, the division was impacted by higher insurance claims mostly associated with Cyclone Debbie, and reduced fund margins from product mix changes, including from customers being transitioned from legacy products to lower fee MySuper products. As a result, cash earnings were 5% lower to $397 million for First Half 2017. Expenses were $17 million lower over the half (down 3%) with productivity more than offsetting higher compliance costs and an increase in investment related expenses. The division reached a major milestone over the half with the release of a number of modules on the Panorama platform. The key elements of the platform are now complete resulting in increased activity and flows onto the platform.

Westpac Institutional Bank

WIB delivered a strong result, with a 26% increase in core earnings from a rise in customer transactions, improved markets income and disciplined expense management. Cash earnings increased 20%, supported by the higher core earnings and partially offset by a $65 million rise in impairment charges. WIB has managed the business in a disciplined way over recent periods, including changing its business model in 2016 helping to keep costs flat and reducing exposures with low returns. This active management of the balance sheet contributed to a 3% decline in

lending over the half with margins up 1 basis point. A focus on relationships has supported a 6% increase in deposits and contributed to a rise in non-interest income as the division has been well placed to support customers involved in significant transactions. This was reflected in higher markets income and an improved contribution from foreign exchange and commodities. Impairment charges were $64 million from an increase in IAPs from new impairments which are partially offset by a reduction in CAPs due to a decrease in stressed assets. Overall asset quality remains sound with stressed assets to TCE falling by one third to 0.59% and impaired assets also declining.

Westpac New Zealand

Westpac New Zealand delivered cash earnings of NZ$462 million, up 6% over the half, with most of the rise due to impairments which were a benefit of NZ$36 million in First Half 2017. Core earnings were 7% lower over the half reflecting a 4% decline in net interest income with growth in lending more than offset by a 17 basis point decline in margins. Most of the decline in margins was from higher funding costs, particularly customer deposits and from the ongoing effects of low interest rates.

Non-interest income was little changed over the prior half. Expenses

were 1% higher, as the business continued the investment in its transformation program. Productivity benefits, from this multi-year program partially offset inflationary increases. Asset quality improved over the half with stressed assets to TCE of 2.41% down 13 basis points. The improvement reflects the stronger outlook for the dairy sector and the work-out of one larger facility. These two elements led to the NZ$36 million impairment benefit. In 2016 a drop in the price of milk solids saw a large number of facilities become classified as stressed; with milk prices having significantly improved, the division is beginning to see customers use the higher prices to improve their financial position and migrate out of stress.

Realised earnings from completed contracts will still be included, but the mark-to-market element will now be excluded. Interesting timing given the fact that home price growth looks to be stalling! This will probably reduce the volatility of earning going forward. But Bendigo had a 6% long run home price growth assumption.

Realised earnings from completed contracts will still be included, but the mark-to-market element will now be excluded. Interesting timing given the fact that home price growth looks to be stalling! This will probably reduce the volatility of earning going forward. But Bendigo had a 6% long run home price growth assumption.