Australian Finance Group (AFG) reported a net profit after tax (NPAT) of $30.2 million for the 2017 financial year (FY2017). This excludes the impact of the recognition of AFG Home Loans (AFGHL) white label settlements relating to prior years (normalised NPAT). This is slightly ahead of the result forecast and an increase of 33% on FY2016.

They now have around 2,900 mortgage brokers, and process on average around 10,000s loan each month with 45 lenders on their panel.

AFG Chief Executive Officer David Bailey said the strong result has been driven by AFG’s core business of residential mortgages, commercial lending, and the continued strong growth in the own-branded AFGHL business.

“Today’s results are a testament to AFG’s strategy of continuing to focus on our core business and growth through earnings diversification. We are very pleased with our progression down this path.”

These results have been achieved in an environment of flat credit growth and significant regulatory changes impacting foreign investment and credit appetites of Australia’s lenders.”

Highlights include:

- Reported NPAT of $39.1 million, normalised NPAT of $30.2 million

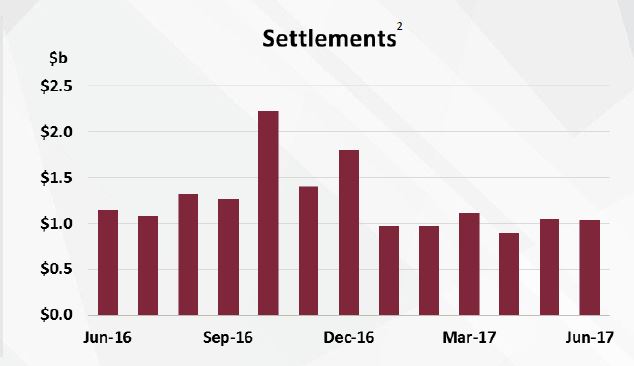

- White label AFG Home Loans settlements of $2.7 billion

- Combined residential and commercial loan book of $133 billion, growth of 11% over FY2016

- Residential settlements of $34.3 billion

- Commercial settlements of $2.8 billion

- Final dividend 5.5 cents per share

- Earnings Per Share (EPS) for FY2017 is 14 cents per share based on normalised NPAT

- ROE of 31%

Company Outlook

The AFGHL business finished the full year 2017 with settlements of $2.7 billion. This result represents a 38% increase on FY2016 and evidences the success of our ongoing strategy to deliver competitive choice to Australian borrowers. The AFGHL loan book is now $5.5 billion, an increase of 44% from $3.8 billion in FY2016.

Overall, the company has a residential loan book of $126 billion that will generate ongoing trail commission. The AFG Home Loans securitised book has seen a 10% increase in settlements for FY2017 to finish the financial year at $1.15 billion, whilst maintaining a strong net interest margin.

Mr Bailey noted the company has achieved another strong year in the recruitment of brokers. From 2,650 active brokers in FY2016, numbers have increased by 8.5% to 2,875.

“In a clear sign of the health of the commercial lending market AFG Commercial asset financing settlements rose 20% to finish the year at $445 million,” he said.

“AFG Commercial mortgage settlements for the year were $2.84 billion, which represents just 0.7% of the overall $410 billion commercial lending market in Australia. The potential for growth is tangible.”

The small to medium enterprise (SME) segment of the market in particular is also one where AFG is optimistic. AFG is poised to harness this growth with the impending rollout of an Australian-first SME lending platform. The new platform, AFG Business, will enable our network of brokers to provide small business borrowers access to a broad range of options and deliver faster access to capital.”

Market conditions

The complexity of the Australian lending market has increased significantly in the past 12 months. “AFG began its listed life with around 1,450 products on its lending platform,” explained Mr Bailey. “That number has now increased to more than 3,400 at FY2107.

“The growth is a reflection of multiple changes by lenders to their Australian product suites. The introduction of new products, changes to LVR bands, numerous product splits with differing rates, repayment options according to loan type, and significant changes to investor and owner occupier pricing have been rolled out across our platform in the past 12 months. These ongoing changes have been delivered at an unprecedented pace and reaffirms the importance to a consumer of having an informed broker.

With more than 10,000 customers seeking the assistance of an AFG broker every month, the value consumers place on the mortgage broking channel continues to be clear. “The mortgage broking channel accounts for 53% of the Australian lending market and more than 20% of those mortgage brokers work with AFG,” said Mr Bailey.

2017 has also been marked by significant regulatory scrutiny of the Australian lending market. “AFG has been at the forefront of consultation with industry, government and regulators. The message we have had for all stakeholders has been clear – AFG has 45 lenders on its panel with more than 35% of borrowings going to lenders other than the four major banks, and we remain committed to ensuring choice and competition remains for Australian consumers.

“This competitive tension ensures consumers continue to have choice and most importantly benefit in terms of home loan price and service because of what brokers deliver on a daily basis across the Australian lending market,” he concluded.