From Australian Broker.

Virgin Money Australia has announced details of its brand new mortgage product, the Reward Me Home Loan, designed to offer customers points of distinction in alignment with the famous Virgin brand, as well as opportunities for brokers.

The home loans, set for launch in May, will initially be sold through mortgage brokers and serviced via a Virgin Money contact centre. Brokers are set to go through an initial accreditation process this week.

Speaking with Australian Broker, Virgin Money CEO Greg Boyle said, “The key rationale for us using the broker channel is that after extensive customer research on home loans, we found that customers expressed a preference for face-to-face interaction. We’re not a branch-based business so the third-party channel was the natural place for us.”

Boyle added that the new home loans take inspiration from Virgin Money in the UK, which does 80% of its lending through third-party channels.

The product will aim to capitalise on the wider reputation of the Virgin name, which demands a certain level of distinction to the rest of the marketplace, says Johnny Lockwood, General Manager of Lending, Cards and Deposits at Virgin Money Australia.

“We have something that has differentiation to what’s on the market at the moment,” Lockwood said. “There is an expectation for Virgin to do things differently at times, and home lending is largely homogenised and I guess regulated at the moment, so we’ve put a lot of consideration into something that’s going to be a little bit different.”

Those points of difference include an array of Virgin-branded benefits, including frequent flyer programs and offers from Virgin Australia, Virgin Mobile, Virgin Wines and Virgin Active. Another unique selling point, says Boyle, will be transparency about what rate discounts are available, with customer research revealing a perceived lack of transparency from lenders regarding discounts.

Boyle added that the target customer will be aged between 25 and 49, based in an urban area and technologically savvy.

The Reward Me Home Loan could also represent a significant development for Australia’s mortgage brokers, thanks to the introduction of a special online tool on the product’s website designed to match brokers with customers.

Lockwood said, “For brokers who are accredited with us, we are going to provide what we’ve called the ‘Find a Broker’ tool.

“Customers will come to our site and will understand they can access our loans through brokers, so we have created a lead capture and referral tool. Customers put their details in and a map will come up showing accredited brokers in their area, and they can choose one that fits their needs, with customer details sent through to the broker and vice-versa.

“Brokers are an important channel for us as they provide the face-to-face interaction with customers. We’ve been talking to some key aggregator groups for some time now so we’ve certainly taken their feedback on board, and we’ll be looking for broker input into any future product.”

The first mortgage aggregator to partner with Virgin Money will be PLAN Australia. Virgin Home Loan’s interest rates will be announced in May.

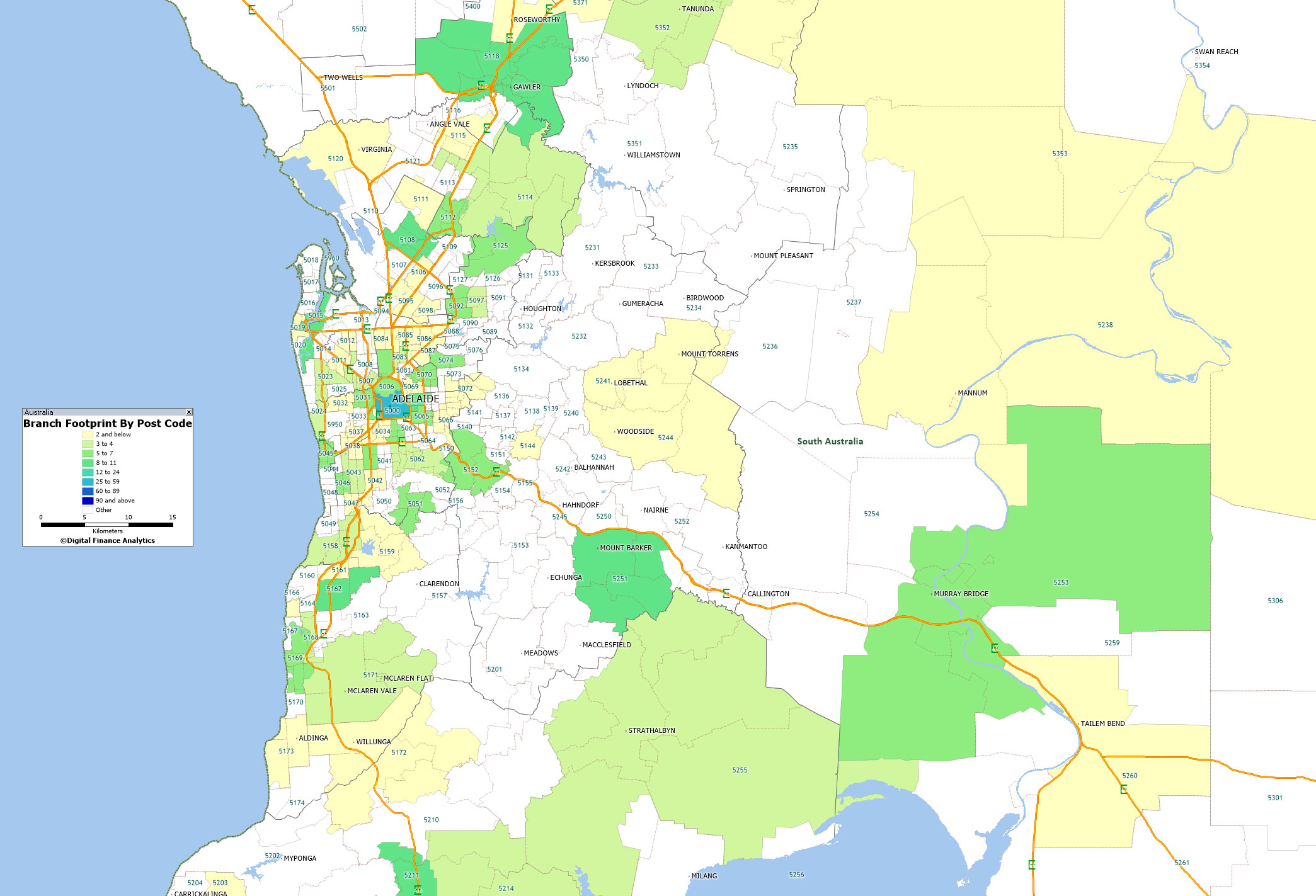

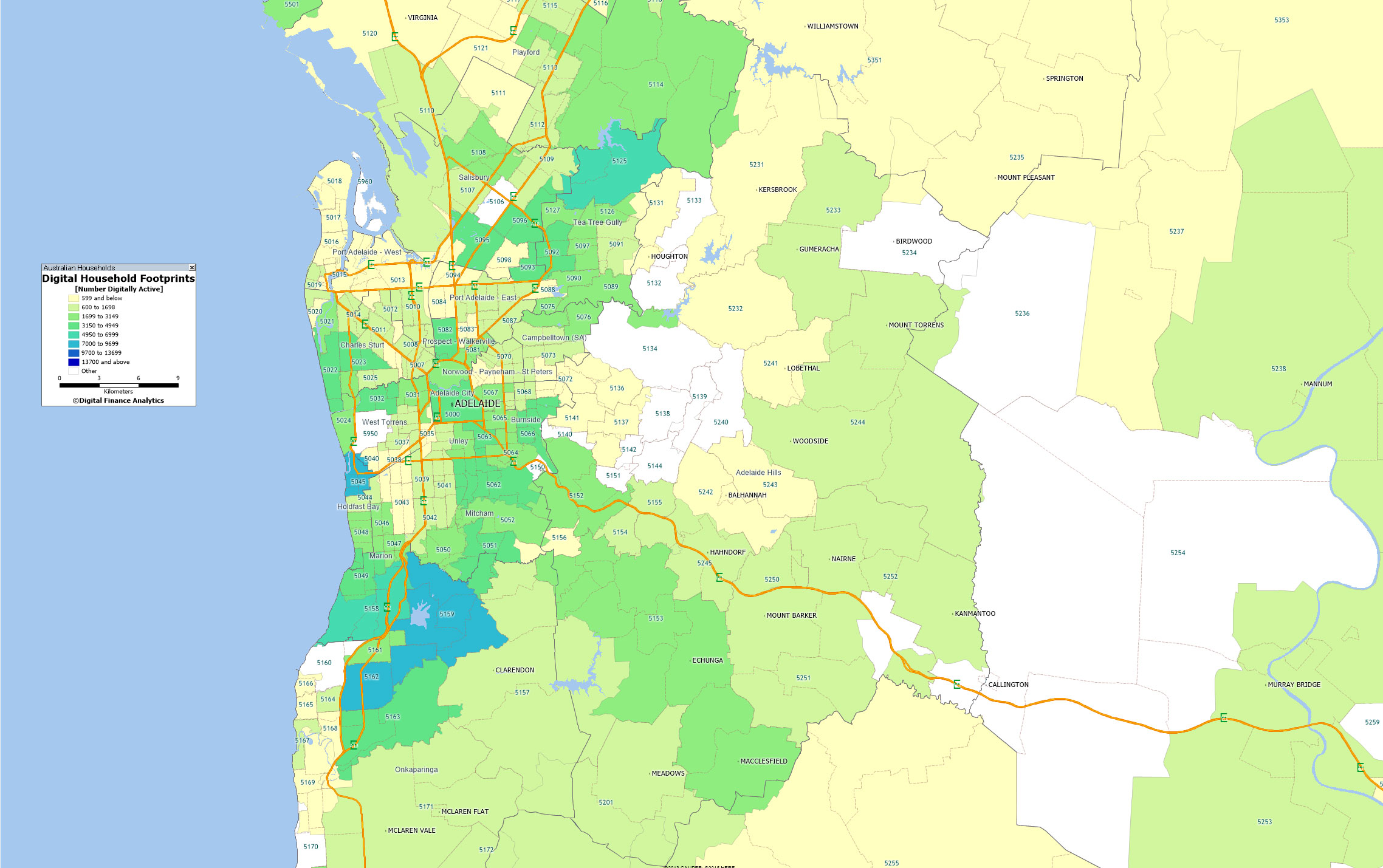

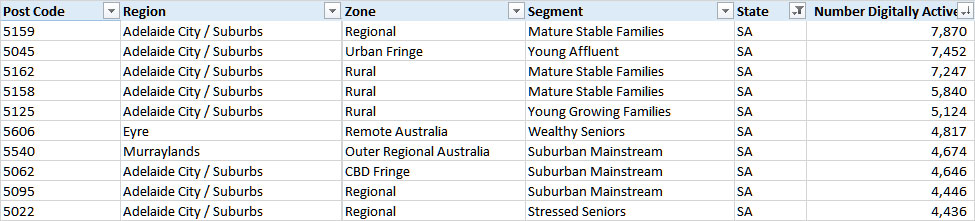

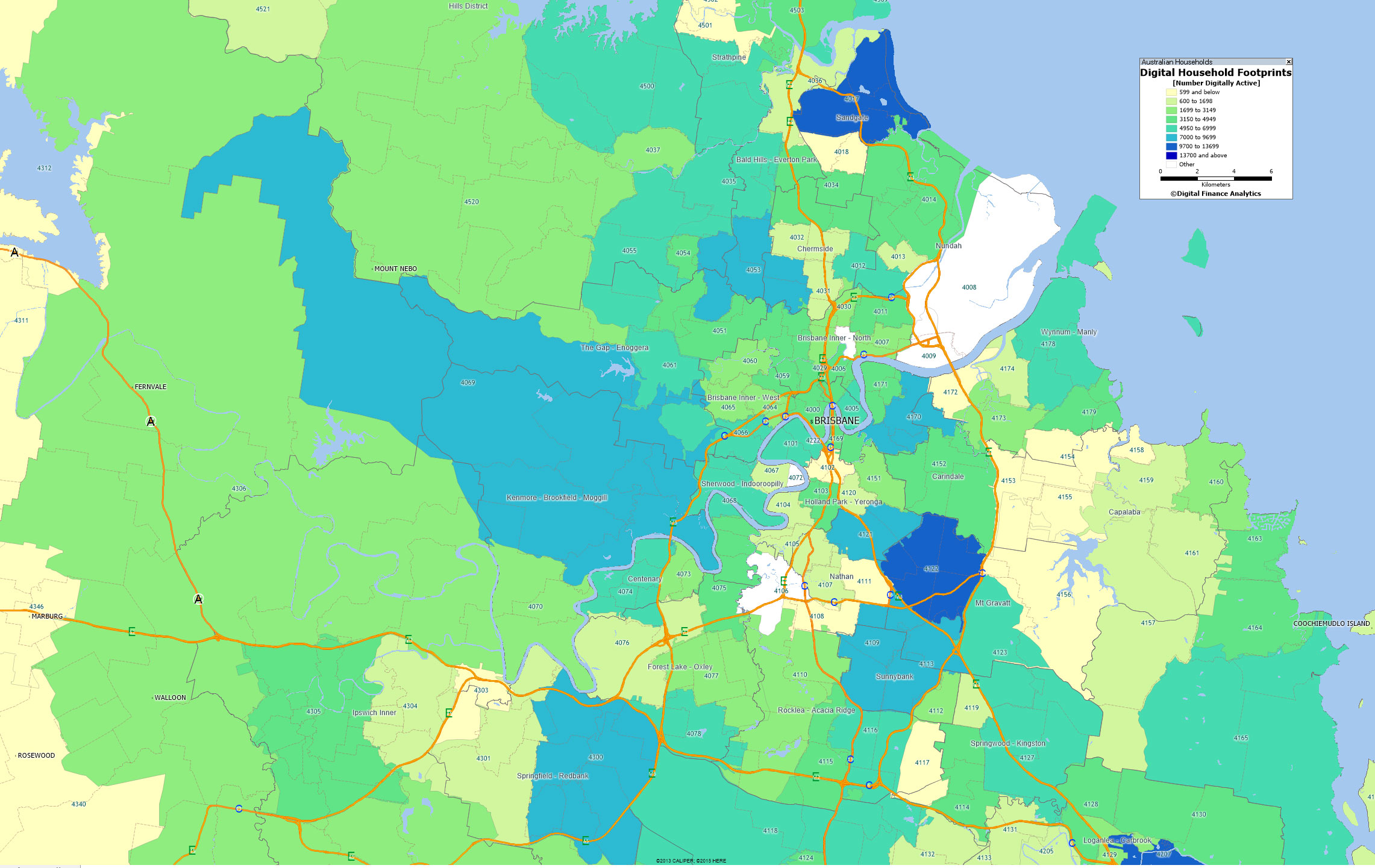

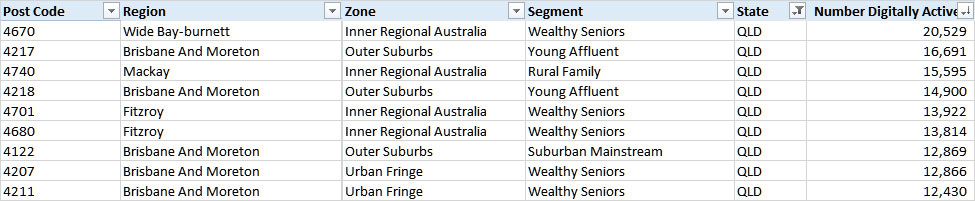

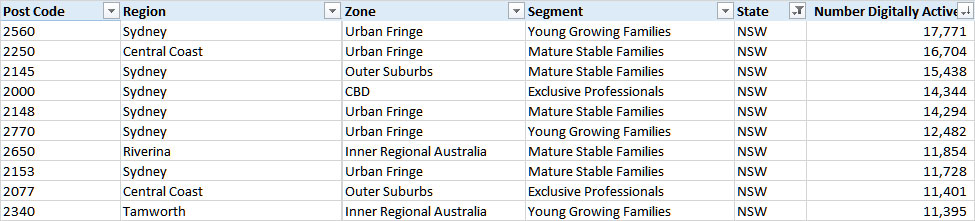

This is an interesting list because it consists of a wide spread of household segments, locations and states. This means that counter to the initial idea of a standardised “digital first” approach, effective digital strategy needs to be tailored and targetted to each group. Segmentation is still required.

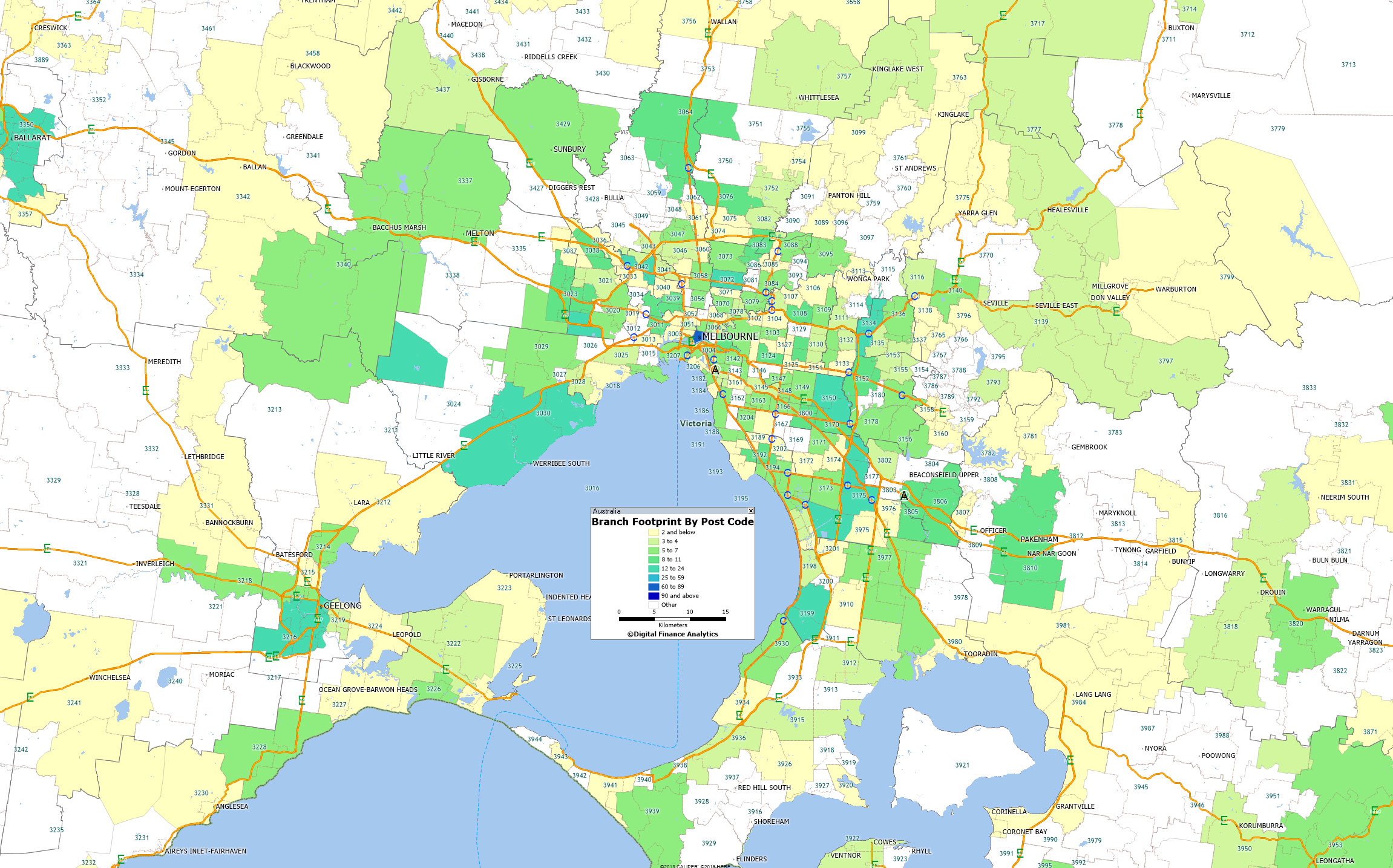

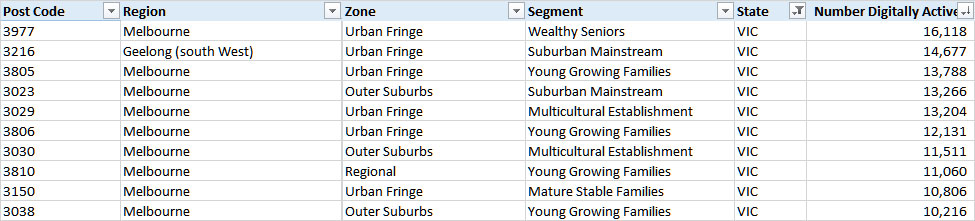

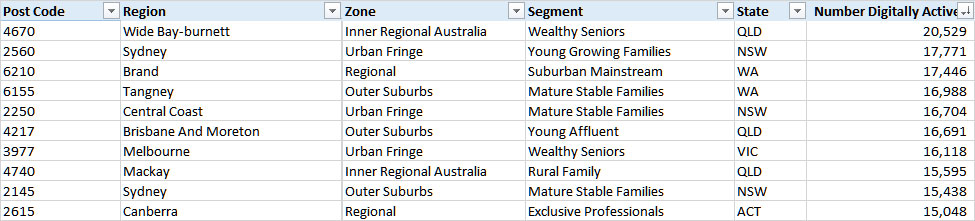

This is an interesting list because it consists of a wide spread of household segments, locations and states. This means that counter to the initial idea of a standardised “digital first” approach, effective digital strategy needs to be tailored and targetted to each group. Segmentation is still required.