Mckinsey says that Consumer adoption of digital banking channels is growing steadily across Asia–Pacific, making digital increasingly important for driving new sales and reducing costs. The branch-centric model is gradually but unmistakably giving way to the mobile-centric one.

Deferring the development and refinement of a digital offering leaves a bank exposed to the risk of weakened relationships and lower profitability. Now is a critical moment to draw retail-banking customers toward Internet and mobile-banking channels, regardless of the general level of network connectivity in a given market.

Our annual study, the Asia–Pacific Digital and Multichannel Banking Benchmark 2016, was led by Finalta, a McKinsey Solution, and examined digital consumer-banking data collected between July 2015 and July 2016 from 41 banks. This article focuses on our findings from Australia and New Zealand, Hong Kong, Malaysia, Singapore, and Taiwan, examining consumer digital engagement, user adoption, and traffic and sales via Internet secure sites, public sites, and mobile applications.1 We detail three counterintuitive findings, and make suggestions for how banks should move forward.

Three counterintuitive findings

Consumer use of digital banking is growing steadily across all five markets (Exhibit 1). In the more developed markets of Australia and New Zealand, Hong Kong, and Singapore, growth in recent years has been concentrated in the mobile channel. Indeed, among some banks use of the secure-site channel has begun to shrink, as some customers enthusiastically shift most of their interactions to mobile banking. In emerging markets, growth is strong in both secure-site and mobile channels.

Exhibit 1

Three counterintuitive findings point to the need for banks to act aggressively to improve their use of digital channels to strengthen customer relationships.

First, banks can excel in their digital offering despite limitations in the digital maturity of the markets they serve. One measure of digital maturity is the Networked Readiness Index (NRI), published annually by the World Economic Forum. This scorecard rates how well economies are using information and communication technology. It examines 139 countries using 53 indicators, including the robustness of mobile networks, international Internet bandwidth, household and business use of digital technology, and the adequacy of legal frameworks to support and regulate digital commerce. Comparison of digital-banking adoption with the level of networked readiness reveals that a country’s level of digital maturity does not necessarily promote or inhibit the growth of a bank’s digital channels.

Singapore, for example, has the most highly developed infrastructure for digital commerce in the world. However, when it comes to digital banking, Singaporean banks trail their peers from the less-networked markets of Australia and New Zealand, where banks have been able to draw consumers to digital channels despite gaps or weaknesses in digital connectivity.

Some banks have also been successful in pushing mobile banking regardless of network limitations (Exhibit 2). While Australia and New Zealand have moderately high levels of third-generation (3G) and smartphone penetration (trailing both Hong Kong and Singapore), the banks surveyed have achieved much stronger consumer adoption of mobile channels than their peers in other markets.

Exhibit 2

The second key finding is that having a relatively small base of active users does not necessarily mean low traffic (Exhibit 3). Among all participating banks in our survey, banks in Malaysia report among the smallest share of customers using the secure-site channel; however, these customers tend to log on many times a month, and the typical secure-site customer interacts with the bank more than twice as often as the secure-site banking customers of participating banks in Hong Kong and Singapore.

Exhibit 3

Third, the survey data reveal wide variations in performance across key metrics by country. In Australia and New Zealand, for example, there is wide variation in digital-channel traffic, with customers logging on with 32 percent more frequency at participating banks in the upper quartile than those in the lower quartile. In Hong Kong, digital adoption among upper quartile peers exceeds that of the lower quartile peers by ten percentage points. Participants in Singapore observe a sixteen-percentage-point gap between the upper and lower quartile peers in the proportion of sales through digital channels.2 The wide gap between best and worst in class in multiple markets points to a significant opportunity for banks to beat the competition with compelling digital offers.

What banks should do

Banks in emerging markets have an opportunity to leapfrog to digital banking. Despite gaps in technology and smartphone penetration, a number of banks have tapped into consumer segments eager to adopt digital channels. Banks in emerging markets should prepare for rapid consumer adoption of digital channels. The digital evolution in emerging markets will differ considerably from the trajectory of banks in more developed markets.

Banks in highly developed markets have room to grow their active user base and digital sales. Indeed, the cost and revenue position of banks that do not act to improve their digital offering may weaken relative to peers that shift more business to digital channels. Banks in all markets should plan for this transition, especially through the integration of diverse technology platforms, the consolidation of customer data across multiple channels, and the continuous analysis of customer behavior to identify real-time needs. It is important to build services rapidly and to go live with minimally viable prototypes in order to attract early adopters—these digital enthusiasts eagerly experiment with new features and provide valuable feedback to help developers.

The significant variation of performance among countries shows great potential for banks to boost digital engagement with a dual emphasis on enrollment and cross-selling. Banks should carefully consider four best practices that often bring immediate gains by streamlining the customer’s digital experience:

Deliver credentials instantaneously upon in-app enrollment. The global best practice shows that banks that issue credentials instantaneously through in-app enrollment see their mobile activity rise on average 1.5 times faster. Of the banks that provided data on functionality, more than 50 percent do not have in-app enrollment. This presents a significant value-creation opportunity.

Simplify authentication processes to make them both secure and user friendly. Approximately three in five banks surveyed lack the ability to authenticate a user’s mobile device. In our experience, banks that store device information and allow users to log on simply by entering a personal identification number or fingerprint see three times more digital interaction than banks that require users to enter data via alphanumeric digits each time they log on.

Implement ‘click to call’ routing to improve response times. Instead of using a voice-response system, where customers must listen to a long list of options before selecting the relevant service choice, an increasing number of mobile apps are adopting click-to-call options for each segment, enabling customers to bypass the voice-response menus. Of the banks that provided data on capability, only 30 percent in our Asia–Pacific survey offer authenticated click-to-call options. The improvement in customer service is significant, with global banks able to improve the speed of answering customer calls by up to 40 percent.

Make digital sales processes intuitive and simple. Take credit cards as an example: best-practice global banks achieve average conversion rates (the ratio of page visits to applications) some 1.6 times those of Asia–Pacific banks. They do this by presenting products and features for which a customer has been prequalified through an intuitive, easy-to-read dashboard display or via tailored messages. Application forms are prefilled automatically with customer data. With intuitive and simple applications, banks in the Asia–Pacific region could increase the rate of completed applications by 22 percent, to come up to par with global best-practice banks.

Across the five markets we focused on, the branch-centric model is gradually but unmistakably giving way to the mobile-centric one. Looking at how digital-channel adoption and usage is evolving, along with the diversity of scenarios, banks have ample room to win in their target markets with a carefully tailored digital offering. Digital-savvy consumers warm quickly to well-designed and easy-to-use digital-banking channels, often shifting to the new channel in a matter of days. Banks need to act quickly to improve their customers’ digital experience or risk being left behind.

REST Industry Super became the first Australian super fund to provide its 1.9 million members with ‘mobile first’ access to personalised financial advice with the launch of the REST Advice Online platform.

REST Advice Online is delivered on Midwinter’s next generation Advice Operating System (AdviceOS) and provides REST members with the ability to receive instant financial advice and make immediate changes to their super account from any mobile device.

The innovative new platform also provides live webchat and over-the-phone support from qualified advice specialists with REST. Importantly the offering is linked to the REST member’s account to enable secure straight-through processing so members can make changes to their super quickly and easily.

The digital advice offering leverages Midwinter’s Digital Advice technology which means that regardless of which method REST members choose to receive advice (phone based, web chat or self-service), it is delivered, recorded and processed from the same integrated advice system.

REST Industry Super CEO Damian Hill said that the new digital advice platform offers user friendly and convenient access to financial advice that is personalised to each member’s unique needs.

“For many Australians, investing can be a daunting task and superannuation, which is an important long-term investment, is no exception. REST Advice Online allows members to make an informed decision about how they’d like to invest their money and grow their retirement savings with confidence.

“Importantly it allows REST members to seek financial advice on their own terms in a way and at a time that best suits them – on their mobile device, via our website or over the phone.”

REST’s new Advice Online service is supported by bespoke technology enabling REST members to explore their options for simple advice related issues and receive an emailed statement of advice after being asked a series of questions and prompts about their circumstances.

Managing Director of Midwinter Julian Plummer said there is now a generation of members who don’t necessarily want the first point of advice contact to be a face to face pitch, especially if it is for simple strategies. “Members want to experience the value of advice digitally in a way that is non-threatening and is instantly accessible.

“For REST to be able to provide this digital advice at no additional charge to its members is a leap forward because they are meeting individuals where they typically spend a lot of their time – on their smart phone or device.”

Initially the new service will help members choose an appropriate investment option and will be expanded over time to encompass a range of advice options across more channels. Mr Hill said, “As custodians of Australians retirement savings we have an obligation to ensure our members are as financially prepared for retirement as possible – introducing REST Advice Online ensures we’re able to provide personalised financial advice at no additional charge to every one of our members.”

Although consumers have quickly adopted digital channels for both service and sales, they aren’t abandoning traditional retail stores and call centers in their interactions with companies. Increasingly, customers expect “omnichannel” convenience that allows them to start a journey in one channel (say, a mobile app) and end it in another (by picking up the purchase in a store).

For companies, the challenge is to provide high-quality service from end to end, regardless of where the ends might be. That was the case for a regional bank that sensed that too many customers were falling into gaps between channels.

Mapping its customers’ journeys confirmed the suspicions (exhibit). Four out of five potential loan customers visited the bank’s website, but from there, their paths diverged as they sought different ways to have their questions answered. About 20 percent stayed online, another 20 percent phoned a call center, and 15 percent visited a branch, with the remainder leaving the process.

Exhibit

The channels’ differing performance pointed to specific problems. Ultimately, more than one-fifth of customers who visited a branch ended up getting loans. But in the online channel, less than 1 percent got a loan after almost 80 percent dropped out rather than fill in a registration form. Finally, in call centers, a mere one-tenth of 1 percent of customers received a loan—perhaps not surprising, since only 2 percent even requested an offer.

To integrate digital and traditional channels more effectively, the bank had to become more agile, with the understanding that its one-size-fits-most processes would no longer work. Complex registration forms were simplified and tailored to different types of customers. Revised policies clarified which channel took the lead when customers moved between channels. And new links between the website and the call centers enabled agents to follow up when online customers left a form incomplete. Together, these types of changes helped increase sales of current-account and personal-loan products by more than 25 percent across all channels.

NAB CIO David Boyle’s spoke at FST Media’s Future of Banking and Financial Services conference. He underscored the extent of the digital transformation underway in banking. 95 per cent of all customer interactions are through digital channels and approximately 70 per cent of customer logons in digital are through mobile devices.

Good morning everybody, it’s great to be back. It’s been two years since I last spoke to you at FST media. I’ve always found it a great conference for getting through to the core of what is important. Today, what’s important for me – as I share a little bit about what’s going on in my life – we have just launched overnight, the latest version of our Mobile Banking Application for Apple.

It’s been an incredibly exciting couple of weeks. For the last three weeks we’ve been progressively rolling out in the Android world and it’s gone so successfully we decided to launch last night with the Apple version. Already this morning, 50 000 of our customers used and logged on to the new application. It’s very exciting because at NAB, it’s all about the customer. At the heart of the One NAB plan is the customer experience. We want the customer experience to be personal, to be easy and to be supportive. And making it easy and supportive for our customers really requires a lot of engagement with customers. And we’ve got to engage with our customers where our customers are.

Most of our customers don’t walk into branches these days. 95 per cent of all customer interactions are through digital channels. So our business customer engagement location is on a train, it’s in the passenger seat of a car, it’s walking down the street, it’s sitting in a conference. We do our banking and we engage with our bank wherever we are. So we need to be living in our customers’ world.

Approximately 70 per cent of our customer logons in digital are through mobile devices now. Our customers are raising the bar. Really raising the bar around how always on they expect us to be in a digital world. There’s no nine to five in a digital world – we’ve got to be able to do everything at all times of the day. So that really raises the bar in terms of how reliable and stable technology can be. But it also raises the bar in terms of how agile and how many new features are being delivered into their hands every day. They don’t expect quarterly or six month releases. New features have to be turning up day in and day out.

There’s a lot of innovative ideas at NAB through our NAB Labs team and outside in the industry. And so how do we really engage with the right ones, and join them up with the customer and experiment with the customer involved in the process to then figure out which innovation is relevant to the customer experience, and then get laser focused on industrialising those particular innovations that are going to move the customer experience the most.

I think that’s the way, in a very crowded landscape. it’s our strategy of being customer-focused and keeping our eye on which particular innovations are going to make it easier, more personal, more supportive for our customers that enables us to focus on the ones that matter the most. So what’s fundamentally different today at NAB in the way that we’re executing these three strategic priorities for our customers is we’re changing the ‘how’ we do it. And I want to focus on two particular ‘hows’ of what we’re doing right now.

The first is DevOps and the second is on-platform innovation. When I think about DevOps and continuous integration and continuous delivery, it is one of the most fundamental changes I’ve seen in my career that really does make a difference for the customer. A DevOps approach gets that balance right for the customer of being always on and really fast at delivering things. Today’s launch of our new mobile Internet Banking app is a really good case study, and we’re nailing it.

The original project name for the project that went live last night was called ‘E-301’. E-301 stands for a great customer experience. E stands for a great customer experience – you always start with the customer experience. The ‘three’ is for three seconds – we want it to be really simple and quick for our customers, so they can login and get to any feature within three seconds. ‘Zero’ means zero down time, so it is always on. ‘One’ is what really drove a lot of change in terms of how we do things. One hour from finishing change to a piece of code to getting it into production.

It completely busts all of the norms that we used to have on how we went through things. It has made the biggest difference.

Last night’s launch I think is the exemplar of really pushing the boundaries with that ‘E-301’ mantra, to set a new, high bar. What we did was, we sat down with 4000 customers over the last year and progressively experimented, innovated and evolved a solution with real customers. Our customers gave us 2700 solutions on how to make it better.

We went live last night and it’s all gone smoothly. Today, we’ve already got some feedback from customers that say they would like to see a subtotal of all of their accounts at the bottom, so we’ll put that into the next release.

And this long-running, persistent team that works on a platform continuously builds new features every fortnight in perpetuity. So this is a really different approach – it’s a platform-based approach, it’s a DevOps approach and what it does is not second guess what the customer experience is about. What it does is it works with the customers and continuously delivers that better customer experience. There is a second platform that’s got very similar features that we’ve been working on for a number of years that is now live in production for our consumer bank and that’s the Personal Banking Origination Platform. We’re now starting to plug the digital and the personal banking platforms together to get that experience across a broader range of services, but we’re seeing really good benefits flow from this platform around getting decisions faster, getting times to yes faster and also driving quite a bit of productivity into some complex end-to-end processes.

We’re doing monthly releases on the PBOP platform and that gives us the ability to learn, engage with our customers and continue to build a backlog of new features and continuously evolve the new platform so that it doesn’t become a legacy system, it becomes a long running persistent team that in 10, 20 or 30 years should be continuing to evolve the customer experience.

This is what I call the ‘ever green model of technology.’ Where all of the platforms in the organisation have this long-running persistent team and an agile, consistently delivering model, then the thing that fundamentally changes – and this is where the real strategy comes to life – is our environment actually gets simpler over time.

What tends to happen with these agile platforms is demand comes to them because they are delivering fast. One of the things I’m most proud that we’ve achieved at NAB in the last 12 months is for the first time in my career operating this way. We actually finished this year with less technology than we started. So we turned off more than we added in. What it was, was continuously building more agile platforms, encouraging demand to come on platform and then naturally, you start to see more decommissioning and adding on of new.

Last week the Australian division of global financial institution Citibank became the first local bank to stop handling cash. The bank’s retail head said it was not a precursor to closing bank branches, but it comes as banks are stepping up their investments in technology, while at the same time looking to reduce costs. But evidence shows customers still want branches or personal interaction with bank staff.

Banks today spend a lot of time talking about technology. Their public documents are littered with terms like “simplification”, “process excellence”, “creating a footprint for a digital world”, “stepping up the pace of innovation”, “cloud based solutions”, “digital transformation”, “unparalleled digital capabilities”, “digital security”, “innovation labs”, “technology for leveraging data analytics” – it goes on and on.

It is clear the banks are highly motivated to ride the technology wave to its full extent. And they cite several compelling reasons. The first is improving the customer experience. The banks argue they can build deep customer relationships through technology improvements.

The way customers want to undertake banking is continually changing, and more and more customers want simplified solutions and to be able to do everything on digital devices. Part of the customer service improvement is heavy investment in data analytics to better understand customer profiles and the ways in which customers transact.

Security is a third factor. Customers want their money to be safe and banks need to invest in secure solutions and the prevention of cybercrime.

But what is the role of the traditional bank branch in all of this? Will increasing digital solutions lead to more branch closures? And do customers still want branch based solutions and interactions?

Branch networks are declining, but at a slower pace

APRA figures show there were 5904 “points of presence” in Australia offering a branch level of service as at June 30, 2016. These figures include non-bank entities such as building societies, but the vast majority relate to bank branches.

From 2012 onwards, the number of branches has shown negative growth each year, and there has been a particularly large slide of 5% in 2016. There has been a greater percentage of closure in rural areas. According to APRA’s branch classifications, there was a reduction of 315 branches, of which 173 (-4%) was in highly accessible areas, 75 (-10%) in accessible areas, 36 (-12%) in moderately accessible areas, 25 (-17%) in moderately accessible areas, 6 (-13%) in very remote areas.

These closures need to be put into context. They are small compared to the many closures that were seen in Australia from the early nineties to the early 2000s, when ATMs and other electronic solutions were being increasingly rolled out by banks. APRA figures show a reduction of more than 2,000 branches over this period.

An Australian parliamentary report at that time put this down to banks seeking increased efficiency and reduced costs in a highly competitive global environment, fuelled by an increase in technology and electronic banking solutions.

The US, like Australia, has also shown a relatively small reduction in branches in recent times. The UK on the other hand has had a comparatively huge number of branch closures. A parliamentary report showed branch numbers have fallen from more than 20,000 in the late eighties to less than 9,000 in recent times. These closures even led to an active group called the Campaign for Community Banking Services. It spent nearly two decades trying to stop the closures but disbanded recently, believing the tide could not be stopped.

Despite bank branch closures, there’s evidence to suggest customers still want branches or some sort of personal interaction with bank staff.

A Canstar Blue 2016 survey showed that in Australia the top three drivers of bank customer satisfaction are enquiry and problem handling, fees and charges, and customer service (branch and call centre). Digital banking (mobile, website and apps) ranks only as the sixth key driver. In the UK, a study by McKinsey (2016) showed that customers still want interaction with branches, especially for more complex transactions.

But do branches still deliver value for the banks themselves? Well yes, not only do they serve to satisfy the needs of those customers who want personal interaction with their banks, these branches are also essential sales outlets for the banks. There is also generally a desire among Australian banks to retain, and even expand, the relationship manager model for business customers, in contrast to a strong move over the last two decades by many global banks towards automated business processes such as credit scoring for small businesses.

The banks in Australia have generally been reluctant to dispel further closures. And it’s clear they wish to move much further into technology-based solutions. However, there appears fairly wide acceptance among the banks that branches and personal contact still have an important role to play. This means branches are likely to keep evolving into smaller outlets focusing on sales and more complex transactions, while banks focus on other technology solutions as they evolve.

Author: Robert Powell, Associate Professor, Edith Cowan University

Google, which is set to report Q3 earnings this week, now makes more ad dollars from mobile than from the desktop globally, according to eMarketer’s latest estimates of ad revenues at major publishers. But in its home market of the US, that revenue flip is still in the (very near) future.

The shift in share of Google’s US ad revenues from desktop to mobile was sharp between 2015 and 2016. Last year, eMarketer estimates, just shy of 60% of the search giant’s net US ad revenues came from desktop placements. This year, it will be almost exactly 50/50, with desktop revenues eking out a 0.6-percentage-point edge. But by 2018, more than 60% of Google’s net US ad revenues will be thanks to mobile spending.

Google is already passing this milestone this year on a worldwide basis: About 59.5% of the company’s net global ad revenues will come from mobile internet ads this year, up from about 45.8% in 2015. By 2018, nearly three-quarters of Google’s net ad revenues worldwide will come from mobile internet ad placements.

This year, Google will generate $63.11 billion in net digital ad revenues worldwide, an increase of 19.0% over last year. That represents 32.4% of the worldwide digital ad market, which this year is worth $229.25 billion.

Google continues to be by far the dominant player in worldwide search advertising. eMarketer estimates the company will capture $52.88 billion in search ad revenues in 2016, or 56.9% of the search ad market worldwide.

On the display side, Google is second to Facebook. It will generate $10.23 billion in display ad revenues worldwide this year, or 12.9% of total display spending.

YouTube net ad revenues will grow 30.5% this year to reach $5.58 billion worldwide. In the US, YouTube is the leading over-the-top (OTT) video service, with 180.1 million users this year. That represents 95.7% of OTT video service users in the US. Net ad revenues on the site will reach nearly $3 billion this year in the US, according for almost 10% of Google’s net ad revenues in the country. That share will rise slightly by the end of eMarketer’s forecast period.

“Google’s accelerating ad revenues have been driven by capitalizing on usage and marketing trends like mobile search, YouTube’s popularity and programmatic buying,” said eMarketer senior forecasting analyst Martín Utreras.

“We see data and advertising at the heart of Google’s new product offerings,” said Utreras. “The new devices are not only aimed at diversifying Google’s revenues but also at enriching Google’s advertising targeting capabilities as consumers engage and share information with Pixel, Google Assistant, Daydream View, Chromecast and other Google ecosystem devices. We see this as contributing to both device sales and advertising revenues in the future.”

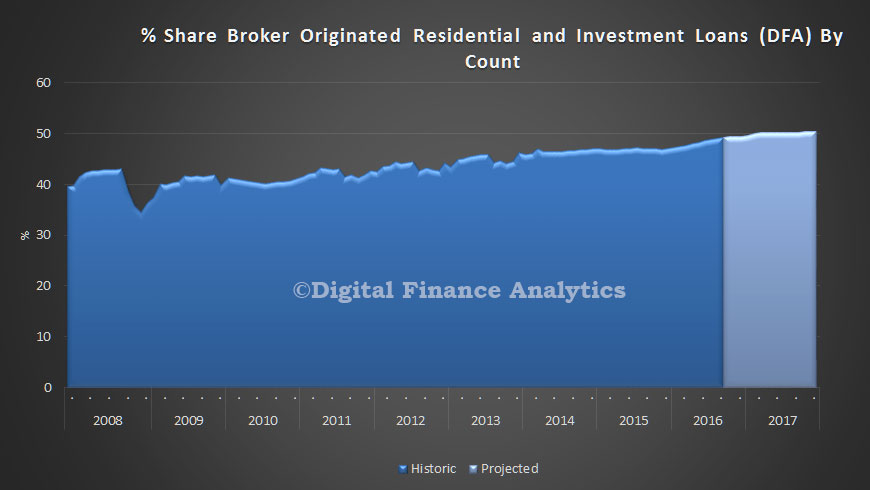

The JP Morgan Australian Mortgage Industry Report – Volume 23, released yesterday, noted that Westpac was rationalising its branch footprint and improving systems to support the group’s multi-brand strategy.

“Over the last 12 months, Westpac have closed 173 branches (from 1,261 to 1,088) and have improved growth by increasing broker flow modestly from 47 per cent to 49 per cent,” the report said.

“The rationalisation of the distribution network (and ultimate culmination of heritage St.George and Westpac systems nearly 10 years after the merger announcement) should see a ‘cheaper cost to serve’, and allow system growth while protecting margins,” it said.

Commenting on the bank’s decision to close branches in favour of the third-party channel, JP Morgan banking analyst Scott Manning said that while the physical cost of distribution was not actually that high, Westpac’s branches were far less profitable than some of its peers’.

Digital Finance Analytics (DFA) principal Martin North, co-author of the report, highlighted that when it comes to distribution and weighing up branches against brokers, cost is not the key issue.

“It’s not so much a cost question,” Mr North explained, “but more a customer-driven issue. Customers are voting with their feet and choosing to go to mortgage brokers for their mortgage needs, which the banks are now adapting their strategies to,” he said.

“The broker channel has a big influence and we expect it to be a bigger influence going forward.”

The report found that despite being the smallest of the four majors in the domestic mortgage market, ANZ has been successful in achieving the same dollar growth in mortgage balances since 2010.

“We believe a key driver of this result has been the success ANZ has had with the broker channel, with originations rising from ~40 per cent of flow to ~50 per cent of flow since 2010,” the report said.

Importantly, the report noted that ANZ has been steadily reducing its branch presence since 2011.

“ANZ is in the unique position where it has consistently grown its loan book above market for the last [few] years at the same time as it is actively reducing its branch presence and increasing its broker presence,” Mr Manning said at the time.

“That is acting as a bit of a business case potentially for other banks to follow,” he said.

“We have previously highlighted our concern for Westpac in particular where they have quite a duplication of their branch presence across different brands.”

At the release of yesterday’s report, Mr Manning said Westpac must work to remove duplications arising from its multi-brand strategy in order to streamline mortgage distribution going forward.

New research from analysts Juniper Research, finds that over 2bn mobile users will have used their devices for banking purposes by the end of 2021, compared to 1.2bn this year globally. Growth in mobile banking is being driven by consumer adoption of banking apps the changing way consumers manage their finances.

The new research, Retail Banking: Digital Transformation & Disruptor Opportunities 2016-2021, found that the number of mobile banking logins are now exceeding that of internet banking logins in many markets. For example, the BBA (British Trade Association for Banking) announced that banking app logins in the UK reached a record 11m per day during 2015, compared to 4.3m internet banking logins during the same period.

Meanwhile, a recent Consumer Survey conducted by Juniper Research found that around 65% of mobile banking customers in the US and the UK uses an app to conduct banking services.Digital Disruption in Banking ~ What Next?

The report found that banks are becoming increasingly concerned that their market position is being undermined by tech-companies and pure-play vendors enabled by technology and regulations to enter the marketplace. For example, in the UK alone 5 new digital banks received licences or launched services so far in 2016, including Starling, Tandem, Atom, N26, and Monzo, with around 20 banks currently in talks with regulators to receive a licence.

Additionally, by 2017, banks in the EU will be compelled to open their APIs. This will result in many innovative new products that analyse (with permission) user data to create more attractive financial services for customers.

“Recent industry shifts highlight why traditional banks must respond rapidly to retain market share by cultivating new revenue channels and enhancing existing base through sustained innovation. However the challenge here for new players is to increase market share and maintain profitability in the long-run”, added research author Nitin Bhas.

The whitepaper, ‘Futureproofing Digital Banking’ is available to download from the Juniper website together with further details of the full research.

Juniper Research is acknowledged as the leading analyst house in the digital commerce and Fintech sector, delivering pioneering research into payments, banking and financial services for more than a decade.

Suncorp is all but quitting over-the-counter banking in WA, closing eight of its nine Perth branches.

The Queensland financial services group says the decision reflects the declining use of branches by customers, who are increasingly going online to do their everyday banking.

“The decision to close a branch is never taken lightly, but we’re finding that fewer customers do their banking at the branch,” Suncorp said in a statement.

“Since 2010, national over-the-counter transactions have declined by 30 per cent, from 685,000 to 478,000 in August 2015, while mobile transactions have grown from 312,000 transactions to more than 5 million in July 2015,” it said.

Banks, however, are also intent on cutting expenses in what is a low-growth environment, with Suncorp chief executive Michael Cameron telling shareholders just last month that “recalibrating” the group’s costs was a priority.

WA accounts for about 7 per cent of Suncorp’s $54.3 billion loan book.

Perth customers who prefer face-to-face banking will have to rely on the one branch not slated for closure, in St Georges Terrace.

The group was unable to say how many staff were affected by the closures, adding that it was trying to redeploy them elsewhere within Suncorp.

One of Australia’s biggest banks has revealed an overhaul in it broker offering that places a strong emphasis on customer service and reducing channel conflict.

NAB today officially launched its updated broker offering, which now means NAB borrowers introduced through the broker channel will have the same access to NAB services and products as any other customer.

Through the NAB broker platform, brokers now have access to four more home loans; NAB Choice Package, NAB FlexiPlus Mortgage, NAB Tailored Home Loan and NAB Base Variable Rate Home Loan, as well as 10-year interest only periods for investment loans.

Upfront and trail commission is offered on the expanded suite of home loan products, while brokers also have access to a wider range of credit card offerings.

Steve Kane, NAB broker offering general manager, said today’s launch is a significant step for the bank and signifies the final step in an ongoing process to strengthen the connection between it and the broker network.

“We had the Homeside brand that didn’t really resonate and put a hurdle in front of brokers when they were talking to their customers. We made a decision to move to NAB Broker and remove the Homeside brand, but the operation stayed the same,” Kane told Australian Broker.

“This is the final stage of that journey, which is really about using the full power of the NAB brand, all the process and services of NAB and all the channels of NAB to support brokers. This is really as much a statement about launching NAB back into the broker market,” he said.

As well as allowing broker clients access to a wider range of products, Kane said the new NAB Broker offering will have a strong emphasis on customer service, which will hopefully lead to a stronger broker–client relationship.

“The position that brokers are now taking is… more and more a long term relationship, rather than transactional one,” Kane told Australian Broker.

“A significant number of brokers are now looking at the whole lifecycle of the customer and part of this rebrand is talking about the broker as a trusted adviser and we’re talking about broking for life.

“We need to be able to offer a holistic range of products and services to support the brokers in doing that, rather than just a mortgage.”

Kane said a new initiative, where select NAB Branches will have staff dedicated solely to broker introduced customers, will hopefully achieve that goal as well as helping to reduce channel conflict.

Under the initiative, brokers can refer their clients to a NAB branch, where dedicated broker channel staff will ensure their accounts and other facilities are set up properly. Those staff are not on a sales incentive program meaning brokers don’t have to fear losing the client.

“The broker is in charge of the products they want to sell the customer. We’re not trying to say we’ll take it all over. What we’ll be doing is ensuring all their accounts and facilities are set up correctly,” Kane told Australian Broker.

“It’s not about competition between channels; it’s targeted at customer service. But it’s not targeted at customer service to the detriment of the broker channel.

“We will always respect the primacy of the broker-client relationship. If a customer came in and said I want a transaction account, we might set them up for that, but on their file brokers can indicate they have a financial planning business or whatever else we won’t do anything that conflicts with that.”