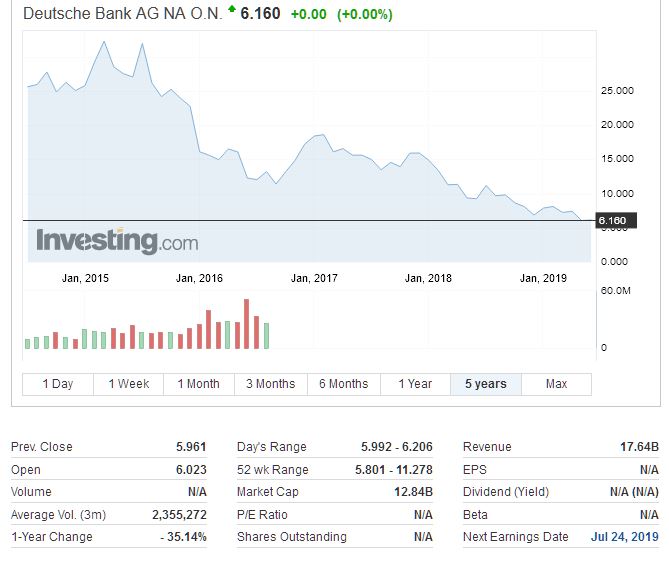

According to a report in the Financial Times, Deutsche Bank is going to overhaul its trading operations and create “bad bank” which will house or sell assets valued at up to €50B (risk adjusted). This would lead to the closure or reduction in its U.S. equity and trading businesses.

While this will likely de-risk the business, it will also reduce profitability (as the US trading division contributed higher returns, and the remaining bank will rely more on deposits for funding. This helps to explain the falls in its share price.

ANZ NZ says David Hisco, its CEO of almost 9 years, is leaving due to ‘ongoing health issues’ and ‘the characterisation of certain transactions following an internal review of personal expenses’

This follows the Reserve Banks’ censure of their operations, as we reported recently.

According to a report in interest.co.nz, ANZ NZ is comfortably New Zealand’s biggest bank. As of March 31, it had total assets of $164.952 billion, total liabilities of $153.224 billion, and gross loans of $132.275 billion. Last year the bank’s annual profit was a shade under $2 billion.

The report says David Hisco, ANZ New Zealand’s CEO since 2010, is leaving the bank under a cloud.

In a statement ANZ says Hisco’s departure follows “ongoing health issues as well as Board concern about the characterisation of certain transactions following an internal review of personal expenses.”

“ANZ today confirmed the appointment of Antonia Watson as Acting CEO of ANZ New Zealand, following the departure of David Hisco,” ANZ says.

“While Mr Hisco does not accept all of the concerns raised by the Board, he accepts accountability given his leadership position and agrees the characterisation of the expenses falls short of the standards required.”

ANZ New Zealand Chairman John Key says it’s disappointing Hisco is leaving ANZ under such circumstances after such a long career, his departure is “the right one in these circumstances given the expectations we have of all our people, no matter how senior or junior.”

Monday’s announcement comes after ANZ NZ announced in late May that Hisco had taken extended sick leave with Antonia Watson, the bank’s managing director for retail and business banking, stepping in as acting CEO.

“We are fortunate to have an experienced executive in Antonia Watson to step in while we conduct a search for a replacement. Antonia’s extensive banking career has her well placed to help ANZ manage through this transition,” Key says.

“Mr Hisco will receive his contracted and statutory entitlements to notice and untaken leave, with all unvested equity to forfeit. The Reserve Bank of New Zealand and Australian Prudential Regulation Authority have been notified of the changes and are being provided all requisite filings.”

Key and Watson will hold a press conference later on Monday morning.

ANZ’s 2018 annual report shows (page 54-55) that in the year to September 2018 Hisco was on a A$1,170,703 fixed salary. On top of this he received A$644,397 in cash as ‘variable remuneration’ and A$864,274 of ‘deferred variable remuneration’, which vested during the year, giving a total remuneration received during the year of A$2,679,384. Hisco was paid in New Zealand dollars, with the amounts converted into Australian dollars.

Hisco’s appointment as ANZ NZ CEO was announced in September 2010, with him succeeding Jenny Fagg. An Australian, he had previously been managing director of ANZ NZ subsidiary UDC Finance between 1998 and 2000. Hisco, 55, has also been a member of Australian parent the ANZ Banking Group’s group executive committee with responsibility for Asia wealth, Pacific, and international retail.

An undoubted high-point of Hisco’s time as CEO of ANZ NZ was the successful culling of the National Bank brand, and movingANZ onto National Bank’s core ‘Systematics’ banking platformin 2012. The two moves effectively unified the two banks nine years after the ANZ Banking Group bought the National Bank from Britain’s Lloyds TSB for A$4.915 billionplus a dividend of NZ$575 million paid from National Bank’s retained earnings.

Australia and New Zealand Banking Group Limited (ANZ) has complied

with the Court Enforceable Undertaking (CEU) entered into with ASIC in

March 2018 regarding ANZ’s fees for no service conduct for its Prime

Access service.

On 31 May 2019, ASIC received an audited attestation from ANZ signed

by Mr Michael Norfolk, Managing Director Private Banking and Advice, and

an independent expert report from Ernst & Young (EY).

ASIC is satisfied with the audited attestation and the independent

expert report. Compliance with the obligations under the CEU is now

finalised, save for the payment of some remaining refunds due to

clients, to be completed by mid-July 2019.

ANZ has attested to the following as required under the CEU:

the changes to ANZ’s systems, controls and processes that have been implemented in response to the fees for no service conduct;

subject to (c), that ANZ has provided documented annual reviews to

Prime Access customers who were entitled to such reviews in the period

from January 2014 to March 2018;

in the 1,410 instances where documented annual reviews were found to

have not been provided, ANZ is in the process of refunding those

customers (with remediation expected to be complete by mid-July 2019);

and

that ANZ now has systems, controls and processes that seek to ensure

documented annual reviews are being provided, and that instances of

non-delivery are detected and remediated.

ASIC is aware that ANZ has announced it will no longer offer the

Prime Access service to new customers and will phase it out for current

customers over the next 18 months. ASIC will monitor the phasing out of

Prime Access.

APRA says it has issued directions and additional licence conditions to AMP Superannuation Limited and N.M. Superannuation Proprietary Limited (collectively AMP Super).

APRA has imposed the directions and additional licence conditions to address a range of concerns regarding AMP Super’s compliance with the Superannuation Industry (Supervision) Act 1993 (SIS Act). The action arises from issues identified during APRA’s ongoing prudential supervision of AMP Super, along with matters that emerged during the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

The new directions and conditions are designed to deliver enhanced member outcomes by requiring AMP Super to make significant changes to its business practices. Areas identified for improvement include conflicts of interest management, governance and risk management practices, breach remediation processes, addressing poor risk culture and strengthening accountability mechanisms. The directions also require AMP Super to renew and strengthen its board.

Additionally, APRA requires AMP Super to engage an external expert to report on remediation and compliance with the new directions and conditions.

This is the second time APRA has used the broader directions power that was granted in April following the passage of the Treasury Laws Amendment (Improving Accountability and Member Outcomes in Superannuation Measures No 1) Bill 2019. It also demonstrates APRA’s commitment to embedding the “constructively tough” enforcement appetite outlined in April’s new Enforcement Approach

A somewhat obscure fact about the marching orders for Australia’s Reserve Bank is that, usually, when a government is elected or re-elected or a new governor takes office, the official agreement between the government and the Reserve Bank changes.

There have been seven such agreements so far, each signed by the

federal treasurer and bank governor of the time, and each entitled “Statement on the Conduct of Monetary Policy”.

The first was signed by treasurer Peter Costello and incoming

governor Ian Macfarlane in 1996, the second when Costello reappointed

Macfarlane in 2003, and the third when Costello appointed Glenn Stevens

in 2006.

The fourth was between new treasurer Wayne Swan and Stevens on

Labor’s election in 2007, and the fifth between Swan and Stevens on

Labor’s reelection in 2010.

The sixth was between incoming treasurer Joe Hockey and Stevens on

the Coaition’s election in 2013, and the most recent one between

treasurer Scott Morrison and incoming governor Philip Lowe in 2016.

The Statement on the Conduct of Monetary Policy (the Statement) has

recorded the common understanding of the Governor, as Chair of the

Reserve Bank Board, and the Government on key aspects of Australia’s

monetary and central banking policy framework since 1996.

For nearly a quarter of a century, as the statement goes on to note,

there has been a core component of how monetary policy is conducted:

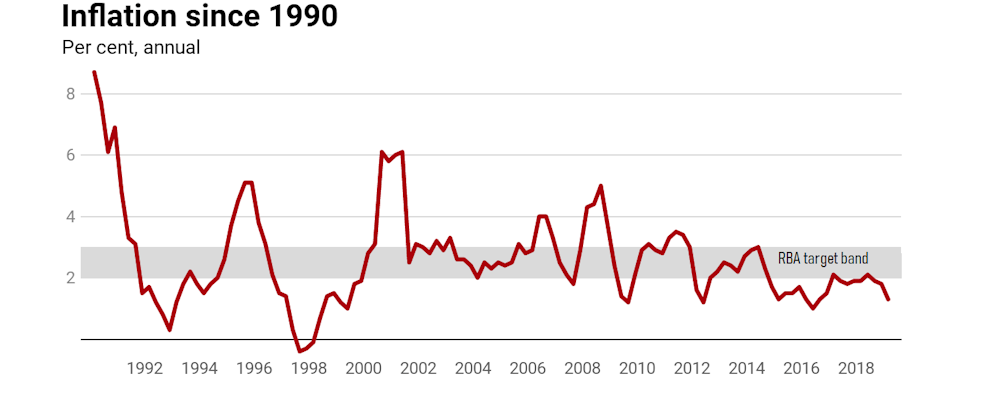

The centrepiece of the Statement is the inflation targeting

framework, which has formed the basis of Australia’s monetary policy

framework since the early 1990s.

But over the years, there have been tweaks. One was this change between the 2013 and 2016 statements.

Effective management of inflation to provide greater certainty and to

guide expectations assists businesses and households in making sound

investment decisions…

The change from “low inflation” to “effective management of

inflation” sounds subtle, but was no accident. It gave the Reserve Bank

extra wiggle room around the inflation target.

And boy, did it come in handy.

The target that’s rarely met

The big question about the agreement is whether the next one (between

Frydenberg and Lowe on the Coalition’s reelection) will tweak the

target again, change it completely, or do something in between.

Because it presumably can’t remain the same.

One reason to think it will change, perhaps significantly, is the

bank’s utter inability to even get particularly close to its target

inflation band of 2-3%, let alone to get within tit, “on average, over time” as required by the agreement.

For years now, inflation has mostly been below the band.

ABS 6401.0

You might not think this matters too much. But it does.

The inflation target is crucial in setting stable expectations for consumers, businesses and markets.

Don’t just take my word for it.

Here is what the previous Reserve Bank governor, Glenn Stevens, said in his last official speech before handing over to Philip Lowe in August 2016:

From 1993 to 2016, a period of 23 years, the average rate of

inflation has been 2.5% – as measured by the CPI, and adjusting for the

introduction of the goods and services tax in 2000. When we began to

articulate the target in the early 1990s and talked about achieving

“2–3%, on average, over the cycle”, this is the sort of thing we meant. I

recall very well how much scepticism we encountered at the time. But

the objective has been delivered.

As I pointed out last month, expectations about price movements depend on Australians believing that the bank will do what it says it will do.

Once people lose faith in the bank’s commitment to or ability to

achieve the target, inflation expectations become unmoored. People react

to what they think what might happen rather than what they are told

will happen. This is what led to Australia’s wage-price spirals in the

1970s and 1980s, and to Japan’s lost decades of deflation.

Three possible outcomes

One possibility is the same statement, word for word. It would be

meant to signal that the bank and the government think things are under

control.

A second possibility is a tweak that further emphasises the “flexible” nature of the target, along the lines Lowe mentioned in his speech at this month’s Reserve Bank board board dinner in Sydney. It would provide more cover for the bank’s inability to hit its target.

A third option would be to add some discussion of the importance of

fiscal policy – government spending and tax policy – as a complement to

the Reserve Bank’s work on monetary policy. Lowe is keen to mention that

he is keen on it, every chance he gets.

But that would put the government under implicit pressure to run

budget deficits at times like those we are in rather than surpluses.

It’s hard to see the Morrison government signing up for that, given its

repeated talk during the election about the importance of being

“responsible”.

Or something more

At the more radical end of the spectrum would be a genuinely new framework for monetary policy.

In the United States, which has also missed its inflation target,

though by not as much as Australia, there has been much discussion of

moving to a “nominal GDP target”. The range mentioned is 5-6% a year.

Advocates of this include former US Treasury secretary Larry Summers, who outlined his rationale in a Brookings Institution report in mid-2018.

ANU economist and former Reserve Bank board member Warwick McKibbin

championed the idea along with economists John Quiggin, Danny Price and

then Senator Nick Xenophon in the leadup to the 2016 agreement between Morrison and Lowe.

Nominal GDP is gross domestic product before adjustment for prices.

In countries subject to big changes in export prices such as Australia,

it can provide a better guide to changes in income.

When nominal GDP is strong (as it is when minerals prices are high)

consumer spending is likely to be strong – perhaps too strong. When it

is weak (as it is when minerals prices collapse) consumer spending is

likely to be weak and in need of support.

But don’t get your hopes up

Given the natural caution of the bank and of this government, we

should probably expect something at the modest end of the spectrum –

even if something like a nominal GDP target would make sense.

Perhaps what’s most important isn’t what the statement says, but that

it says something and that the Reserve Bank sticks to it. It will lose

an awful lot of credibility if it sticks to nothing.

CBA has today entered into an agreement to sell Count Financial Limited to ASX-listed CountPlus Limited.

Commonwealth Bank of Australia (CBA) has today entered into an agreement to sell Count Financial Limited (Count Financial) to ASX-listed CountPlus Limited (CountPlus) for $2.5 million (the Transaction). CountPlus is a logical owner of Count Financial given its historical corporate relationship and equity holdings in 15 Count Financial member firms.

CBA will continue to support and manage customer remediation matters

arising from past issues at Count Financial, including after completion

of the Transaction. CBA will provide an indemnity to CountPlus of $200

million and all claims under the indemnity must be notified to CBA

within 4 years of completion. This indemnity amount represents a

potential contingent liability of $56 million in excess of the

previously disclosed customer remediation provisions that CBA has made

in relation to Count Financial of $144 million (which formed part of the

remediation provisions announced in the 3Q19 Trading Update). CBA has

already provided for the program costs associated with these remediation

activities.

The Transaction is subject to a CountPlus shareholder vote to be held

in August 2019 and completion is expected to occur in October 2019. The

Transaction is not expected to have a material impact on the Group’s

net profit after tax.

CBA currently owns a 35.9% shareholding in CountPlus and intends,

subject to market conditions, to sell its shareholding in an orderly

manner over time following completion of the Transaction.

From a financial perspective, the Transaction will result in CBA

exiting a business that, in FY19, is estimated to incur a post-tax loss

of approximately $13 million.

Implications for NewCo

Following completion of the Transaction, NewCo will comprise Colonial

First State, Financial Wisdom, Aussie Home Loans and CBA’s 16% stake in

Mortgage Choice. Consistent with the announcement in March 2019, CBA

remains committed to the exit of these businesses over time. The current

focus is on continuing to implement the recommendations from the Royal

Commission and ensuring CBA puts things right by its customers.

Here is an extended discussion between Ex APRA/ASIC Executive Wilson N. Sy, Economist John Adams and Analyst Martin North. We look at how banking is regulated and who is really pulling the strings.

After successfully leading Westpac’s consumer bank, BOQ’s new boss George Frazis has landed a big job at a much smaller bank with a shrinking mortgage book, via InvestorDaily.

In

April, Bank of Queensland reported reporting negative mortgage growth

of $248 million, down from positive growth of $11 million in 1H18, with

its portfolio dropping to $24.7 billion.

The fall was driven by a

$717 million contraction in settlements through BOQ’s retail bank,

offset by a $469 million rise in home loan volumes through its

subsidiary, Virgin Money Home Loans.

The regional lender is well

aware of the challenges within its retail bank, which is effectively

franchised with branches being run by ‘owner-managers’. Given the

negative press generated by the royal commission, attracting new owner

managers has been difficult for BOQ.

Prior to the appointment of

George Frazis as CEO on 6 June, interim chief executive Anthony Rose

delivered an 8 per cent drop in cash earnings in the first half of

FY19.

“Across

the industry, as you are well aware, there have been significant

changes in the banking landscape which has created revenue headwinds for

the sector. In addition, the outcome from the royal commission is

lifting expectations of the regulators. Adjusting to the new regulatory

environment will come with a higher cost profile, absent any mitigating

actions which we are of course exploring,” Mr Rose said in April.

“BOQ

also has challenges that are specific to our business, particularly in

the retail bank. Our digital customer offering, lending processes and

the inability to attract new owner-managers with the overlay of

regulatory uncertainty, has hampered customer acquisition and returns.”

Mr

Rose, BOQ’s chief operating officer, will remain as interim CEO until

Mr Frazis takes over in September. Rose took charge following the

resignation of John Sutton in December 2018.

Morningstar analyst

David Ellis praised the appointment of Mr Frazis, an experienced banker

with 17 years in the industry, most recently as CEO of Westpac’s

consumer bank and CEO at St George Bank.

“While Frazis has strong

credentials and deeply understands the dynamics of Australia’s consumer

banking industry, he will be taking control of a regional player with a

small geographic distribution footprint, higher funding and operational

costs, a lower credit rating and tougher regulatory capital burden,” Mr

Ellis said.

The Morningstar analyst believes the challenge for

Mr Frazis is to assume a bigger role in a smaller organisation that

lacks market share, brand awareness, distribution capabilities and

funding advantages that major banks enjoy.

“Bank of Queensland’s

lending growth has been subdued for several years,” Mr Ellis said.

“Based on APRA banking statistics for April 2019, the bank’s 12-month

growth in home loans sit at just 0.3 per cent in April, compared to 1.7

per cent a year ago and 11.8 per cent three years prior.”

Bank system home loan growth is 3.3 per cent for the year to April 2019.

With

the RBA cutting rates this month, BOQ has lowered its fixed rates in an

effort to remain competitive in a mortgage market dominated by the big

four. However, with more cash rate cuts expected, Morningstar is

concerned whether BOQ can sustain its course of passing on the

reductions.

“The bank lacks access to lower-cost funding options

and has a much lower return on equity than the major banks,” Mr Ellis

said.

Under Mr Frazis’ leadership, Westpac’s consumer bank

attracted more than a million new customers in the past four years.

Digital channels now account for a third of sales.

“Frazis will have to do the same at Bank of Queensland,” Mr Ellis said