According to Moody’s last Thursday, Canada’s Office of the Superintendent of Financial Institutions (OSFI) notified the country’s regulated mortgage lenders that it will intensify its supervisory oversight of their residential mortgage underwriting practices.

In the past 10 years home prices in Canada have lifted more than in Australia, although the debt to disposable income ratio at around 155% is still lower than Australia (175%) but higher than the UK (~130%). The Canadian market is also exposed to the impact of future interest rate rises.

Moody’s says that Canadian housing prices have risen faster than most other industrialized countries, resulting in house price levels increasing substantially over the past 10 years to be among the highest in major industrialized countries (see Exhibit 2), and raising the risk of a price correction. Over the past 25 years, house prices in Canada have steadily increased, primarily in urban centres such as Toronto, Ontario, and Vancouver, British Columbia.

The regulator vowed a heightened focus on income verification, mortgages with loan-to-value ratios of less than 65% (which OSFI indicated was a category in which underwriting practices are often less rigorous), stress assumptions related to debt-service ratios and the reliability of property appraisals. OSFI’s announcement is credit positive for Canadian banks because heightened regulatory scrutiny will force them to maintain or enhance existing residential mortgage underwriting controls and practices amid growing concerns about increasing household debt and elevated housing prices.

Residential mortgage debt, including home equity lines of credit (HELOCs), has doubled over the past decade. Canadian conventional mortgage debt, excluding home equity lines of credit (HELOCs), has grown at a compound annual rate of 7% over the past decade. Almost CAD1.6 trillion in mortgage debt, including HELOCs, was outstanding as of 31 March 2016, more than double the amount outstanding for the same period 10 years ago (see Exhibit 1).

Over the past 25 years, Canadian consumer debt-to-income levels, which include mortgage debt, almost doubled and are at a record high. As a result, housing indebtedness has tracked closely to house price increases as borrowers take larger loans, while at the same time, incomes have not kept pace. These higher debt levels make Canadian consumers vulnerable to an employment or interest rate shock that would exacerbate their debt-servicing burden (see Exhibit 3).

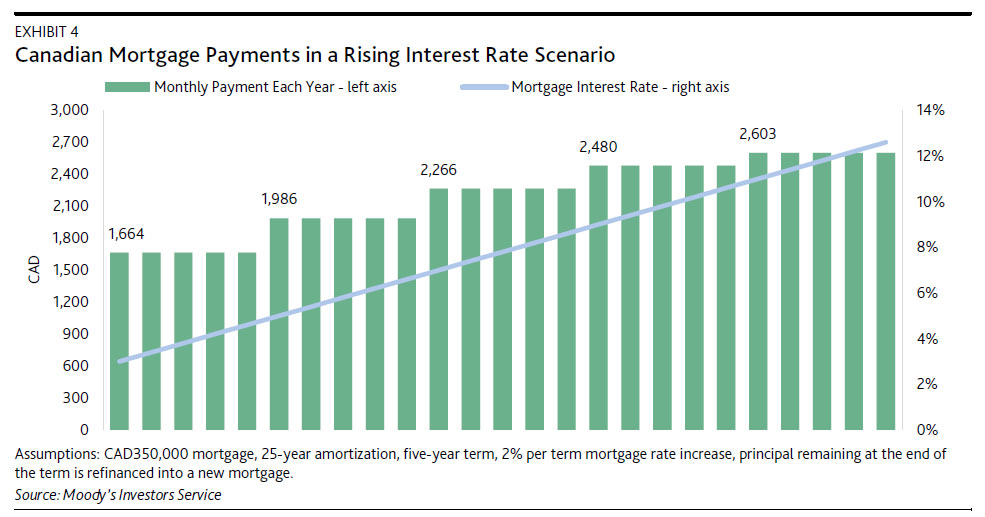

Of note, OSFI specifically indicated its interest in debt service ratios because current underwriting requirements may not adequately capture the stress effect of refinancing a mortgage into one with a higher mortgage interest rate. This is important because of the unique characteristic of a Canadian mortgage. A Canadian mortgage is structured as a balloon loan whereby the term (typically five years) is shorter than its amortization (typically 25 years). This means borrowers must periodically refinance their mortgages (see Exhibit 4), exposing them to changes in interest rates over the life of the mortgage. This refinancing risk is greatest for recent borrowers with high loan-to-value mortgages in a rising interest rate environment. OSFI noted that a rapidly rising interest rate environment would place considerable stress on existing debt service ratios, particularly on investment properties with rental income.