Moody’s says Canada’s Department of Finance announced that it will launch a consultation process with market participants this fall on lender risk sharing, a policy that would require mortgage lenders to absorb a portion of loan losses on insured mortgages that default. Currently, banks are able to transfer virtually all of the risk of insured mortgages to mortgage insurers, and indirectly to taxpayers through a government guarantee.

Any changes to the provisions of mortgage insurance to impose risk sharing on mortgage lenders would be credit negative for Canada’s six large banks, which account for approximately 72% of mortgage lending in the country, because it would reduce their asset quality and risk-adjusted profitability. The six banks are The Toronto-Dominion Bank, Bank of Montreal, Bank of Nova Scotia, Canadian Imperial Bank of Commerce, Royal Bank of Canada and National Bank of Canada.

The details of the Department of Finance’s plan have yet to be released, and it may be some time before they emerge. Possible approaches include imposing first-loss deductibles on banks, whereby the lender would be responsible for an initial portion of the loss, with the insurer only bearing losses beyond that deductible amount. Another option would be to divide losses between the lender and insurer on a pro rata basis, or to charge the lender a fee for a defaulted mortgage. In any case, the concept of the lender retaining some risk on insured mortgages will support stability in the housing market in Canada by encouraging prudent underwriting standards.

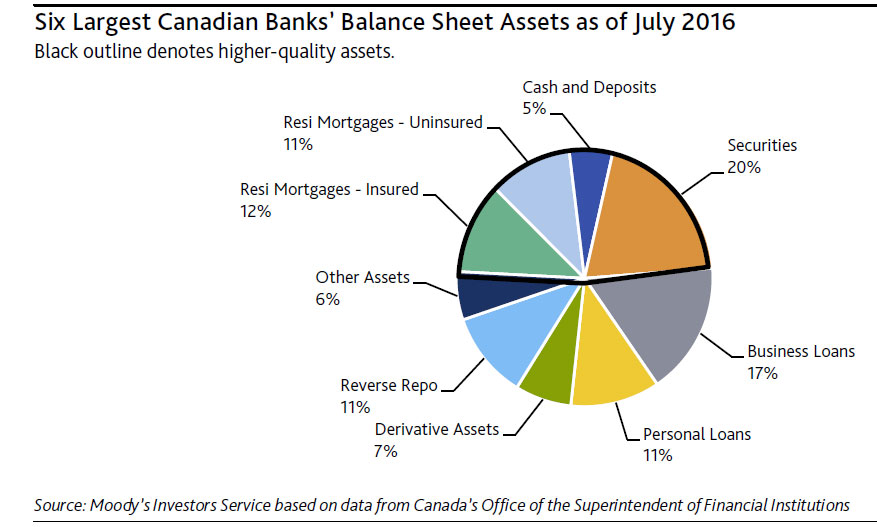

Canadian banks’ high asset quality is largely the result of their significant holdings of government-insured residential mortgages, uninsured mortgages, securities, cash and deposits with financial institutions, which comprise about half the aggregate system’s balance sheet. Canadian mortgage portfolios and home equity lines of credit have performed well historically, owing to the high use (approximately 50%) of government backed mortgage insurance, and conservative underwriting practices. Government-supported insured mortgages make up 12% of total assets. This insurance is primarily sold either directly to the borrower, who is legally required under Canada’s Bank Act to obtain insurance if the loan-to-value of the mortgage exceeds 80%, or is held by the lenders themselves on a portfolio basis as a liquidity and capital management tool.

Canadian banks currently make a solid margin on insured mortgages for which they bear no risk and have no regulatory capital requirements. Under any risk-sharing arrangement, depending on the degree of loss shared and any offsetting concession on insurance premiums paid, profitability on a significant asset class will change. On balance, we expect that risk-adjusted profitability will decline, although a detailed analysis at this point is not possible.