Moody’s says the newly released Basel Committee Guidelines on Prudential Treatment of Problem Assets Are Credit Positive for Banks.

Last Tuesday, the Basel Committee on Banking Supervision (BCBS) published Guidelines on the prudential treatment of problem assets (definition of nonperforming exposures and forbearance). The guidelines address the current absence of a common and internationally applicable definition of nonperforming exposures and forbearance and will help harmonize the definition and treatment of banks’ problem loans, a credit positive for banks.

Uniformity across jurisdictions and banks will reduce discrepancies in the recognition and treatment of problem assets. Uniformity will also make international comparisons of banks’ nonperforming exposures, loss recognition and provisioning less challenging.

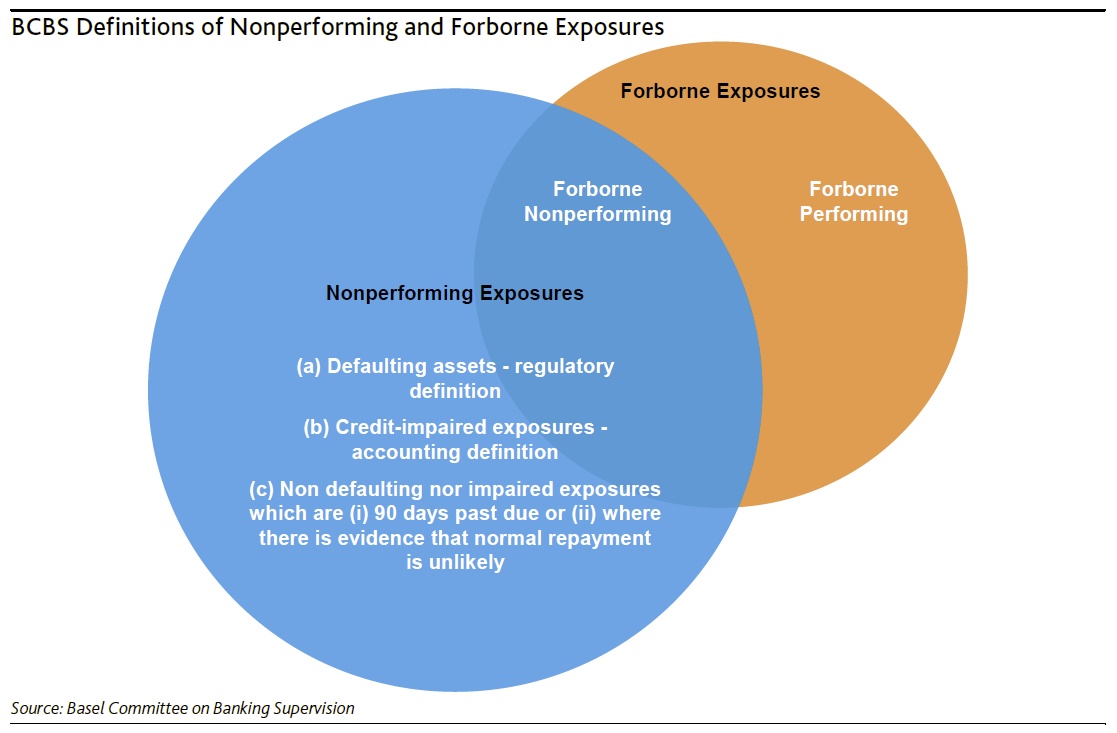

The BCBS definition of nonperforming exposures is not a substitute for the regulatory classification of defaulting assets and the accounting definition of impaired assets, but supplements these other designations. The BCBS definition extends the nonperforming categorization to all exposures (excluding trading book and derivatives) that are more than 90 days past due or where there is evidence that a full repayment is unlikely.

The scope is wider than under regulatory standards, where default is recognized only after 180 days past due for exposures secured by real estate and exposures to the public sector. It also goes beyond the accounting concept of credit-impaired exposures defined in International Financial Reporting Standard No. 9.5 In addition, nonperforming exposures can be re-categorized as performing only after standards on debt repayment and a debtor’s creditworthiness are met. The re-categorization rule will increase the stock of nonperforming exposures for some banks under this measure.As shown in the exhibit below, forbearance is defined as a concession granted on exposures where counterparties have financial difficulties, and which the bank would not otherwise have considered. Concessions can take various forms, including extension of term, rescheduling and interest rate reduction. Forbearance is a newly identified concept that can apply to performing or nonperforming exposures. A forborne exposure can return to normal status only if all payments have been made during a probation period of one year and the debtor has resolved its financial difficulty.

In the European Union (EU), similar standards became effective in September 2014. The implementation of these new standards was a critical step in the recognition and treatment of problem assets by EU banks. At the implementation date, the ratio of nonperforming exposures on gross loans published by EU banks was 7%, one percentage point higher than the ratio of impaired and past-due loans, and subsequently decreased to 5.1% in December 2016. The ratio of forborne exposures was 3.2% as of the same date.

An international standard for nonperforming and forborne exposures will require cross-border banks to implement a common definition of problem assets, forcing them to address rising risks in timely manner. It will translate into some disclosure requirements whereby banks will have to publish amounts of nonperforming and forborne exposures, allowing market participants to compare banks’ problem assets, risk provisioning and credit loss recognition. This guideline is key for a harmonized framework to assess asset risk, but it does not address other sources of discrepancies, such as the definition of default, which makes the comparison of banks’ risk-weighting calculation challenging.