‘In Search Of …. Unquestionably Strong’ was the title of a speech given by APRA Chairman Wayne Byres. It is he highlights that there is an ongoing journey towards building greater capital ratios for the banks.

He makes two points of note. First banks around the world are on the same journey, so it must continue, and second, what ‘unquestionably strong’ meant precisely was largely left for APRA to determine. Its not a matter of mechanically moving in step with international benchmarks to maintain top quartile position.

He went ahead to reinforce the point that top quartile positioning is just one means of looking at the issue, and certainly not the only one to use; highlighted that there are many unknowns about the way capital adequacy will be measured in future, so it is not the end of the story; and that capital is just one measure of the strength of an ADI, and ideally we should think about ‘unquestionably strong’ with a broader perspective.

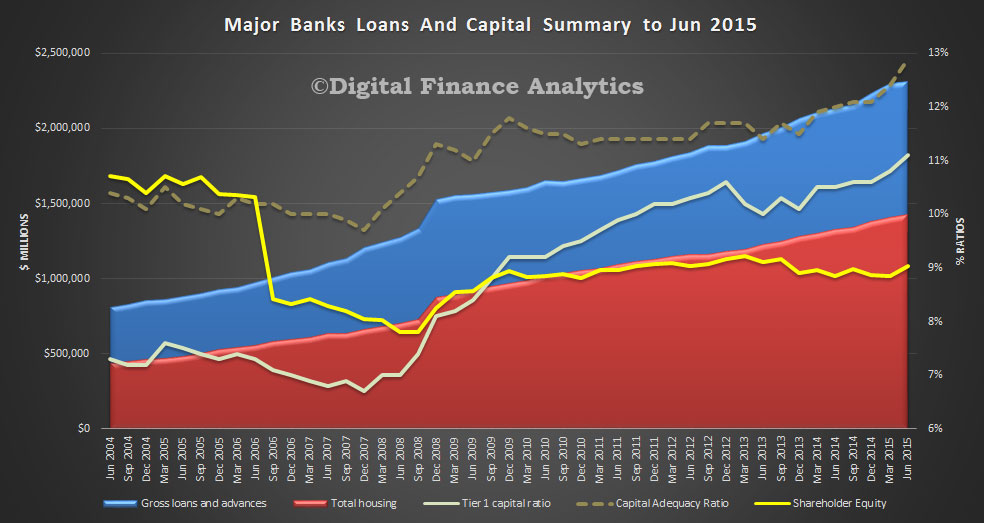

Using the data from the quarterly performance statistics he compared the capital ratios again CET1 and other measures. We have highlighted the fact that the ratio of loans to shareholder capital has not improved and concluded “We also see the capital adequacy ratio and tier 1 ratios rising. However, the ratio of loans to shareholder equity is just 4.7% now. This should rise a bit in the next quarter reflecting recent capital raisings, but this ratio is LOWER than in 2009. This is a reflection of the greater proportion of home lending, and the more generous risk weightings which are applied under APRA’s regulatory framework. It also shows how leveraged the majors are, and that the bulk of the risk in the system sits with borrowers, including mortgage holders. No surprise then that capital ratios are being tweaked by the regulator, better late then never”.

He concluded that APRA was still thinking about how to define ‘unquestionably strong’ and the role of top quartile positioning and made five closing points.

He concluded that APRA was still thinking about how to define ‘unquestionably strong’ and the role of top quartile positioning and made five closing points.

- we have a soundly capitalised banking system overall in Australia;

- with the aid of recent capital raisings, the initial 70 basis point CET1 gap to the top quartile that we identified is likely to have been substantially closed;

- higher capital ratios are likely to be needed if current relative positioning is to be retained and enhanced, particularly if measures beyond CET1 are examined;

- by quickly moving on the FSI recommendation regarding mortgage risk weights, APRA has created time to consider international developments emerging over the next year or so; and

- given where we are today, APRA and the banking industry have time to manage any transition to higher capital requirements in an orderly fashion.

We would observe that the first two statements seem contradictory – if we are so well capitalised, why the lift in capital by 70 basis points? Why also are regulators all round the world desperately lifting ratio? The short answer is because they let the ratios get too lean and mean – as demonstrated by the GFC. This has to be addressed.

So, in short, the journey lays ahead. Then of course Basel IV is just round the corner. Australian banks are likely to find the costs of doing business will continue to rise. with consequences for loan pricing, loan availability and bank profitability.