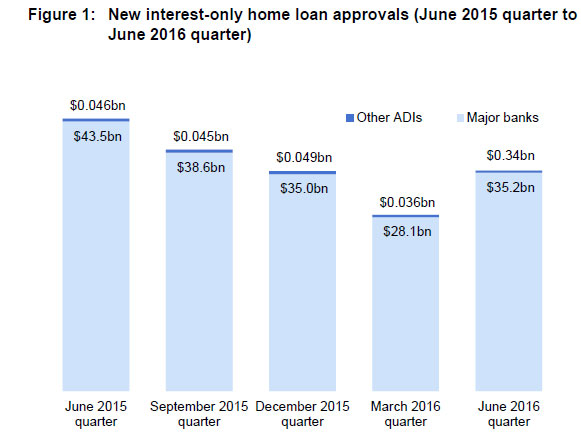

ASIC says the volume of interest only loan approvals rose significantly in the June 2016 quarter. But Australia’s home loans industry has improved its performance over the past year, adopting better ‘responsible lending’ practices, though there is still room for improvement.

ASIC has released its report (REP 493) ‘Review of interest-only home loans: Mortgage brokers’ inquiries into consumers’ requirements and objectives’ on the responsible lending practices of 11 large mortgage brokers with a particular focus on how they inquire into and record consumers’ requirements and objectives.

It also examined how the changes implemented by lenders in response to the findings from ASIC’s report into interest-only home loans from 12 months ago last year (refer: Report 445) have flowed through to mortgage brokers.

Since the release of Report 445 in August 2015,

- the percentage of new home loans approved by lenders which are interest-only has decreased by 12%; and

- the amount that can be borrowed by an individual consumer through an interest-only home loan has decreased, as lenders have adjusted their assessment of consumers’ ability to repay, in line with ASIC’s recommendation in Report 445.

Information provided by the mortgage brokers showed that for the six months from July 2015 to December 2015,

- the number of new interest-only home loans fell by 16.3%, with total value of these loans reducing by 15.6%; and

- the percentage of interest-only loans with a term greater than five years reduced by more than half, from 11.2% to 5.1%.

Almost 80% of applications reviewed included a statement summarising how the interest-only feature specifically met the consumer’s requirements and objectives. This compared favourably with Report 445’s finding that more than 30% of applications reviewed showed no evidence the lender had considered whether the interest-only loan met the consumer’s requirements.

‘It is vital that mortgage brokers understand consumers’ requirements and objectives to ensure they are not placed in unsuitable credit contracts,’ said ASIC deputy chairman Peter Kell.

‘ASIC is pleased that our concerns about interest-only loans and responsible lending are being acted on by the home lending industry, but there is still room for improvement.’

ASIC identified practices that place brokers at increased risk of non-compliance with their responsible lending obligations, and identified opportunities for brokers to improve their practices. Key compliance risks identified included:

- Policies and procedures—Mortgage broker policies and procedures provided only general information, rather than tailored information on specific products and loan features that may impose increased financial obligations or restrict repayment flexibility (such as interest-only home loans);

- Recording of inquiries—Record keeping was inconsistent and in some cases records were fragmented and incomplete;

- Explaining the loan choice—More than 20% of applications reviewed did not include a statement explaining how the interest-only feature of the loan specifically met the consumer’s underlying requirements and objectives. The level of detail in these statements varied considerably and in some cases, where an interest-only loan was specifically sought by a consumer (including where this option was recommended by a third party, such as an accountant), the reason for this was not clear;

- Consumer understanding of risks and costs—In some cases, where the potential benefit of the interest-only loan depended on the consumer taking specific action (for example, allocating additional funds to higher interest debt), it was unclear whether the consumer understood the potential risks/additional costs if the specific action was not taken.

The report details steps that mortgage brokers should take to improve their current practices, including:

- Ensuring they understand the consumer’s underlying objectives for requesting specific loan products and features;

- Recording concise summaries of consumers’ requirements and objectives and the reason why a particular product, features and lender was chosen;

- Providing a statement summarising the broker’s understanding of the consumer’s requirements and objectives, which could also include the reason a particular loan is suggested, for the consumer to confirm before obtaining a loan.

- Where the potential benefits of a loan feature might require the consumer to undertake specific behaviour, ensuring consumers were aware of the action they needed to take to obtain the potential benefit, as well as the potential costs should this action not be taken.

2 thoughts on “ASIC on mortgage brokers’ interest only loans”