ANZ has today announced its collaboration with Honcho by Business Switch an online platform offering customers the opportunity to set up their small business in one day, along with tools to help their business grow.

Using the tool, Business Ready powered by Honcho, customers can register their ABN, business and domain name, set up a simple website, email addresses and ANZ business bank accounts without having to visit multiple websites and suppliers.

ANZ Managing Director Corporate and Commercial Banking Mark Hand said: “Each year in Australia around 300,000 small businesses are set up and one of the biggest frustrations our customers have is it takes weeks to get started and they often don’t know what steps to take next. This tool is a simple, efficient and cost effective solution that guides customers through the process. “Combined with our $2 billion dollar pledge for new small businesses and discounted banking packages, our Business Ready initiative is another way ANZ is providing ongoing support from the start-up phase through to the growth phase and beyond,” Mr Hand said.

Honcho Chief Executive Officer Matthew Abrahams said: “We chose to work with ANZ because of its commitment to small businesses and our shared goal of making life easier for small business owners. “The single biggest issue that new small businesses face is time. Being able to fast track starting up a business from weeks to hours with only a small capital outlay enables people to start earning revenue faster and to concentrate on building their customer base,” Mr Abrahams said.

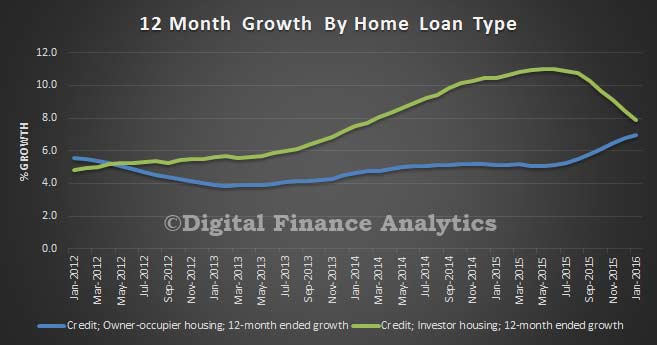

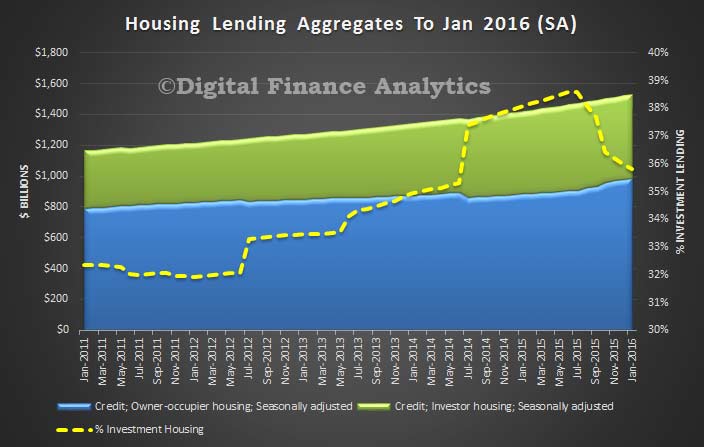

The APRA Monthly banking statistics for January 2016 came out today. Whilst overall ADI lending for housing grew 0.6%, lending for owner occupation grew 0.9%, from $898 bn in December to $906 billion in January. Much of this will be refinancing of existing loans, and some first time buyer activity. Investment lending grew very slightly. However, there was a $1.4 bn adjustment between OO and investment loans, so the splits are not that reliable. So, whilst lending may be slowing a little, there was significant momentum in the market in January. Total lending reached $1,424 bn, up by $8.1 bn.

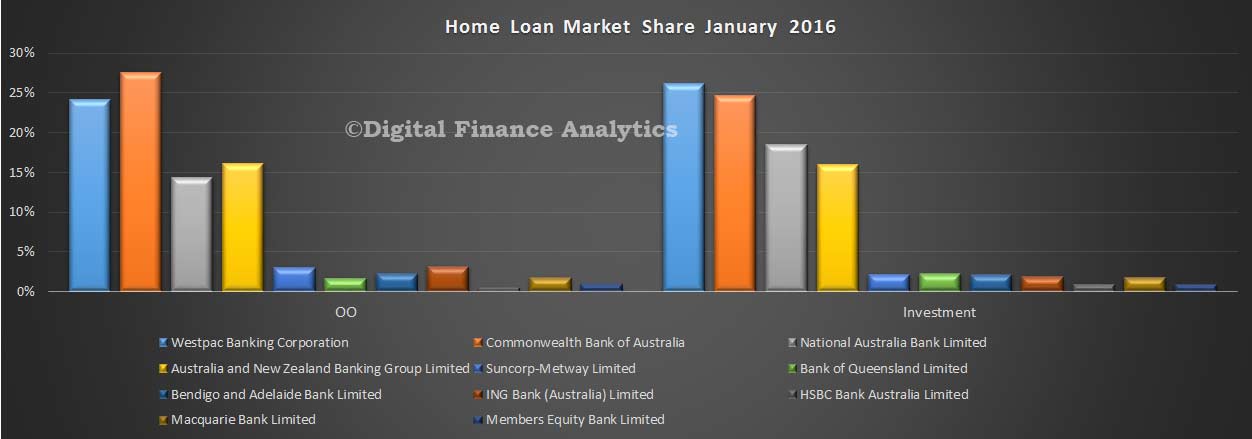

Looking at the individual banks, the market shares did not change that much, with CBA holding 27.6% of owner occupied loans, whilst Westpac holds 26.13% of investment loans.

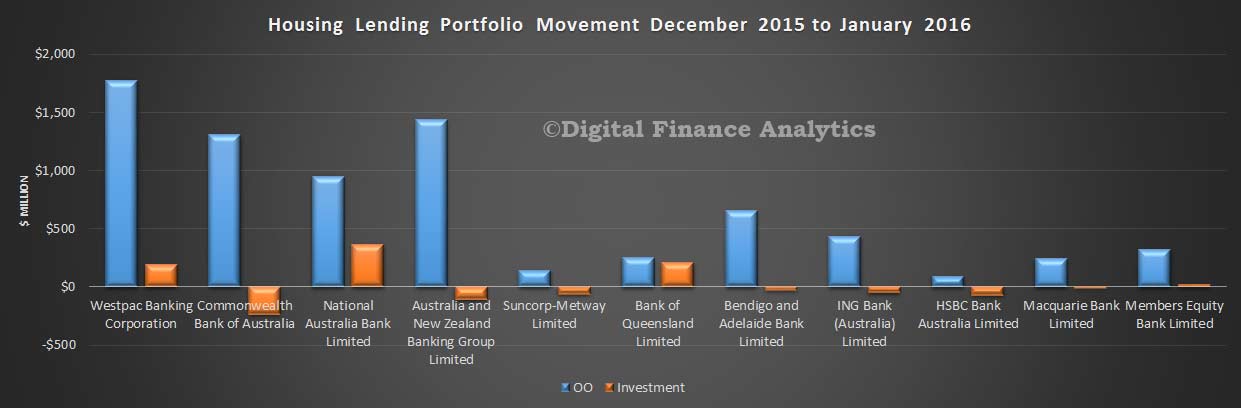

The portfolio movements (which are not adjusted for reclassifications between OO and investment loans) highlights growth in OO loans across the board. Movements in investment loans is more patchy.

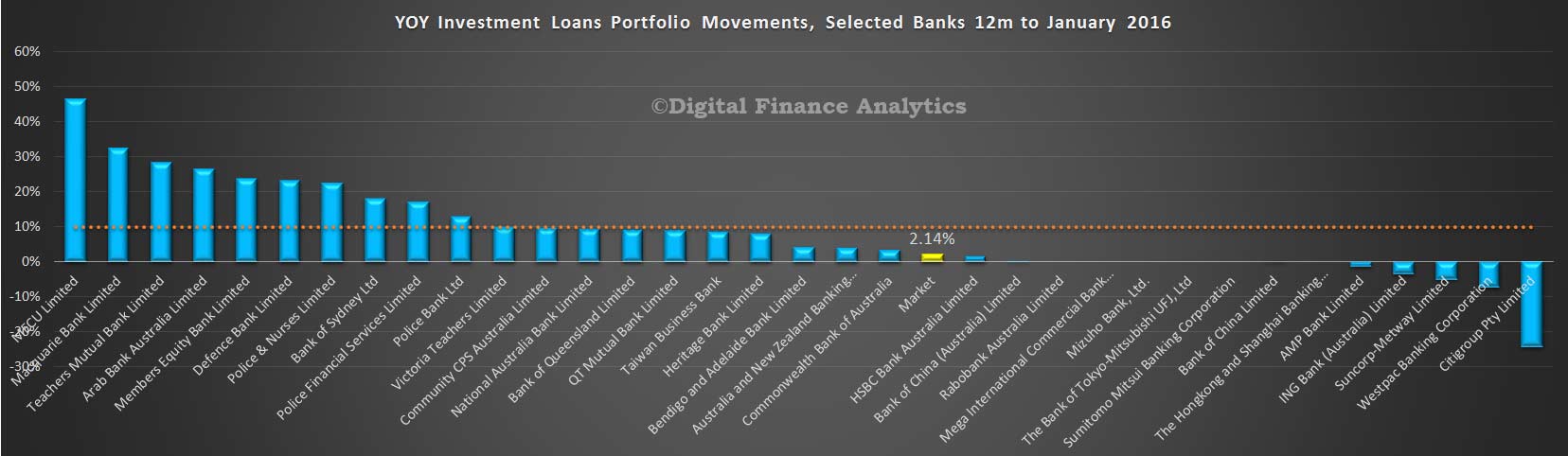

For what it is worth (and we have consistently used the monthly data, adjusted where we can), we see that market growth in investment loans is now sitting at 2.14%, for the 12 months to January 2016. The big four are all below the APRA 10% speed limit. Others, for various reasons are still speeding.

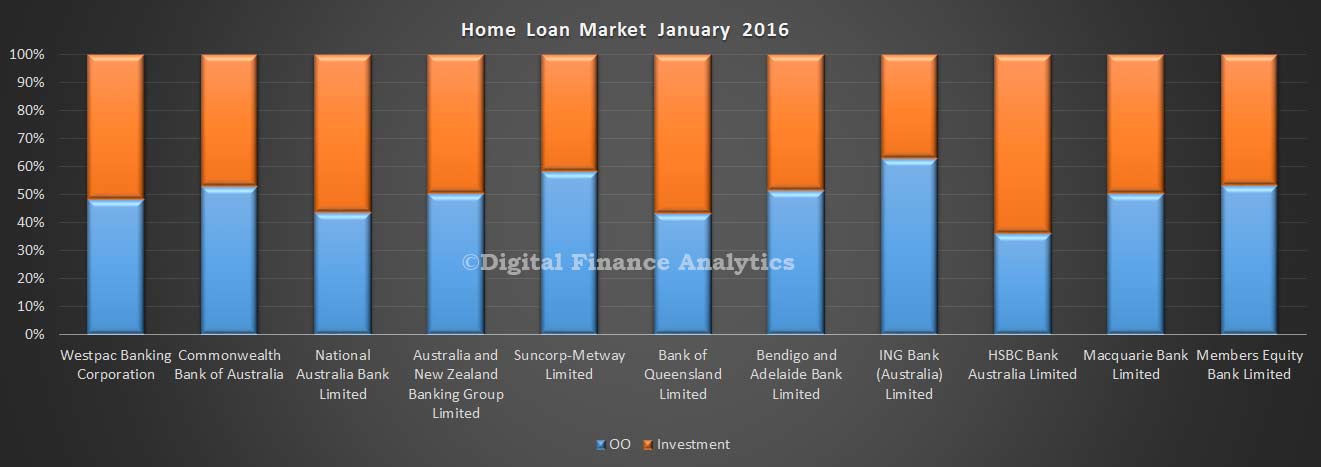

The splits between OO and investment lending varies by lender, with HSBC, Bank of Queensland and NAB holding the larger proportion of investment loans, expressed as relative market shares.

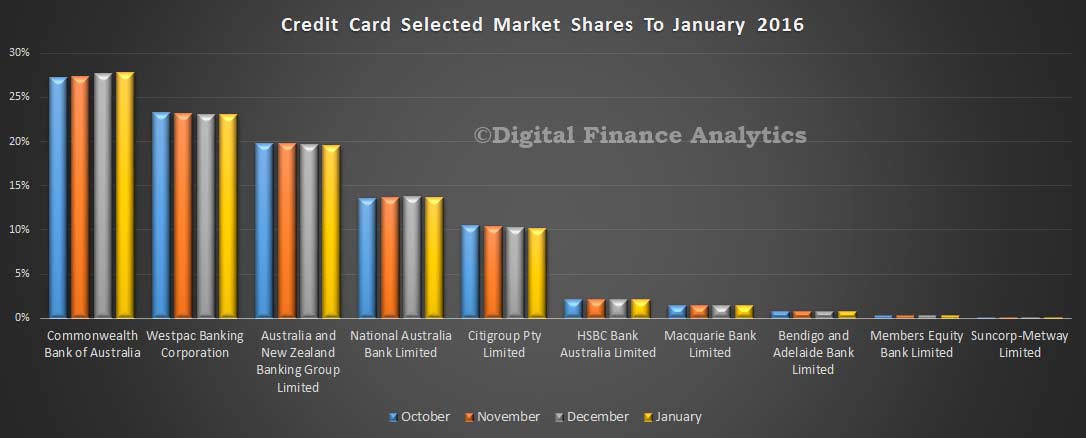

Tuning to credit cards, total balances fell $747m in the month, to $41 billion. CBA is growing its relative share of cards, with 27.8% of the market. NAB also grew slightly in relative terms, whilst ANZ and WBC fell a little.

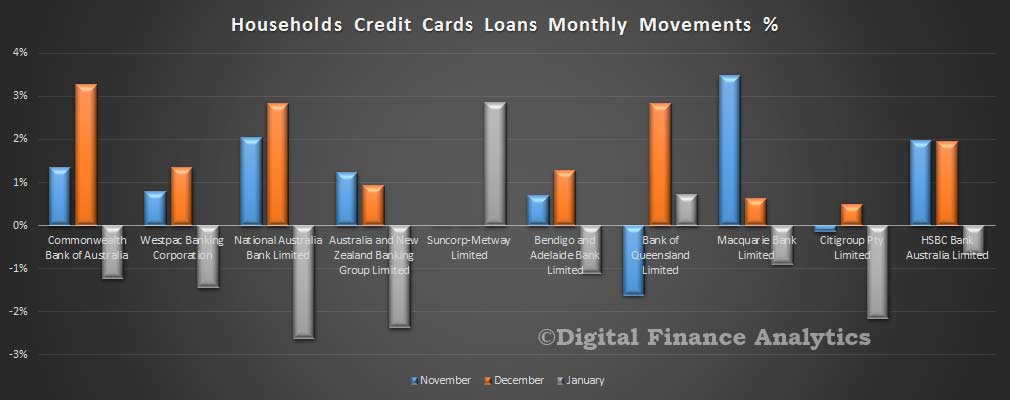

Looking at the monthly movements, we see that households are paying down loans they took over the Christmas.

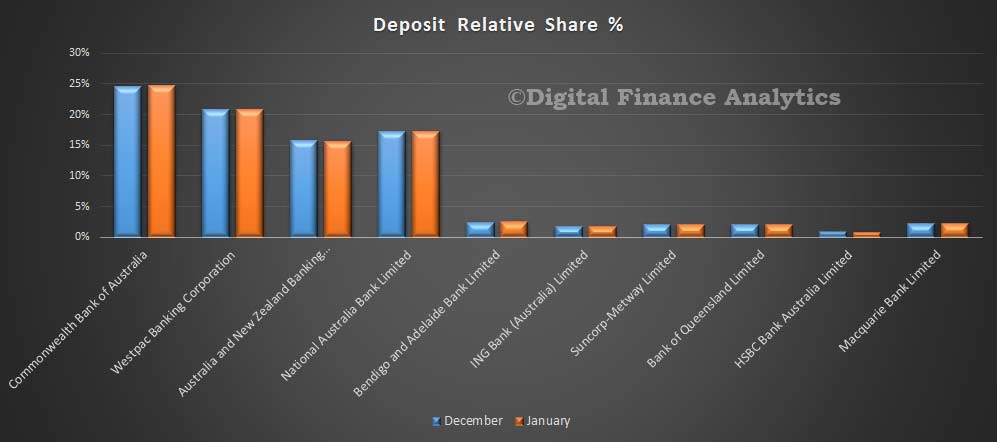

Turning to deposits, total deposits grew 0.8% to $1.92 trillion. CBA grew its share a little, from 24.6% to 24.8% and remains the largest holder of deposits in Australia.

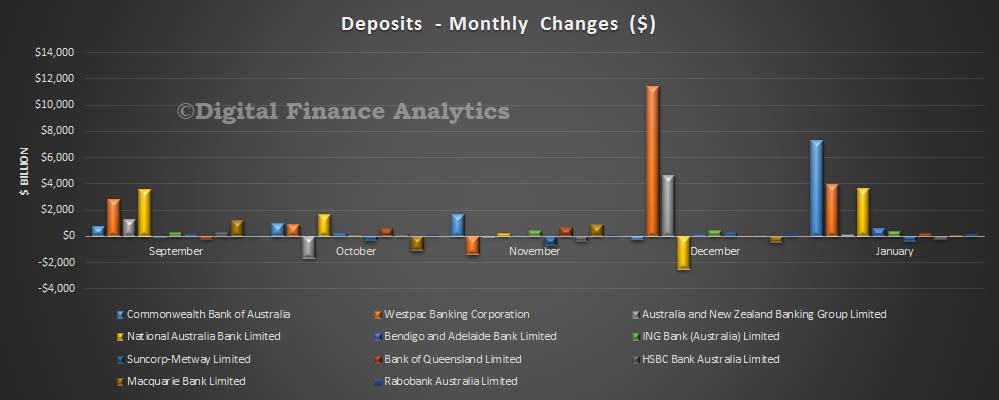

ANZ lost a little share in the month as it attracted less money in than the other three majors. CBA lifted net balances by $7.3 bn, compared with WBC’s $3.9 bn and NAB’s 3.6 bn.

Given the higher margins on overseas funding at the moment, with speads elevated thanks to a range of global uncertainties, local deposits are more valuable, and we expect to see some strong competition for balances in the months ahead.

Total home lending was up 0.53% in the month, and $8bn was for owner occupied lending. Investment lending went sideways, but note also though that there were further adjustments between OO and investment loans.

“Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $35.3 billion over the period of July 2015 to January 2016 of which $1.4 billion occurred in January. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes”.

As a result, the proportion of loans for housing investment purposes has fallen a little further, from 35.98% to 35.8%, but this is still a big number.

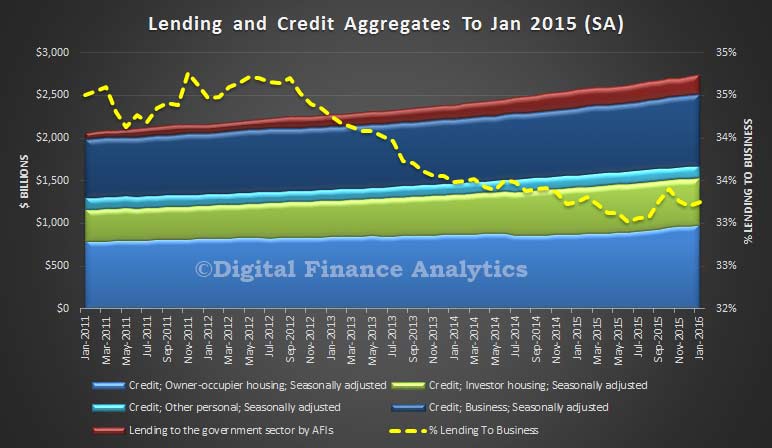

Turning to the overall aggregates, home lending was up 0.53%, business lending rose 0.63% and personal credit fell 0.79% as households paid off their Christmas binge.

Business investment remains at a relative low level, with one third of all lending going to business, once again showing how debt to households is being relied on to grow the economy.

We know from our own analysis that significant numbers of households would find any rise in interest rates a big problem, and loading up households further with ever more debt is a flawed strategy. When are we going to get serious about getting real long term growth via business investment?

We will discuss the parallel APRA data, also released today, later.

Anyone who’s dug into the 2008 financial crisis knows the role that bundling and selling subprime housing loans played in bringing the world to the brink of economic collapse – out-of-control behaviors well-depicted in the movie “The Big Short.”

But one thing I hope “The Big Short” doesn’t do is further tarnish the image of subprime lending.

Despite their poor reputation, such loans remain a key tool in easing the housing affordability crisis and expanding the availability of mortgages to low-income Americans seeking to realize the dream of homeownership. They also can help policymakers cope with the growing ranks of the homeless.

I’ve been studying the world of subprime in recent years, and these are some of the lessons from my current and past research. First, we need to fix the subprime mortgage market, so that the ways in which it contributed to the financial crisis aren’t repeated.

Shocking levels of homelessness

Los Angeles, New York and other cities in America are struggling to cope with the problem of homelessness and the lack of affordable housing.

On a single night in January 2015, more than 560,000 people nationwide were homeless – meaning they slept outside, in an emergency shelter or in a transitional housing program. Almost a quarter were children. Meanwhile, homeownership is hovering at 20-year lows, while about half of renters struggle to pay their landlords.

Last fall, Los Angeles Mayor Eric Carcetti asked the City Council to declare “a state of emergency” on homelessness and committed US$100 million to solving the problem, suggesting that subsidies would play a role.

But a focus on rental subsidies to solve homelessness and other affordable housing issues has adverse consequences, as evidenced by New York’s experience.

Its cluster-site housing program, in which privately owned apartment buildings are used to house homeless families when the city’s shelters are full, relies on such subsidies. But because the city typically pays market rents (or more), many landlords responded by pushing out regular (and low-income) tenants in favor of this steady stream from the government.

Such programs reduce the overall supply of affordable units, crowding out other groups in need. As more affordable housing units are allotted to the homeless, there are fewer available for low-income residents who don’t qualify for those programs and are at risk of becoming homeless themselves.

Fortunately, Mayor Bill de Blasio aims to phase out the costly program over the next three years.

While there are many other approaches to tackling homelessness, they rely on addressing an important underlying problem: the housing affordability crisis. It may seem improbable, but subprime lending could help ease the housing affordability crisis.

The role of subprime lending

The relationship between homelessness and the strains in the housing rental market is well-known: when there are more rental vacancies available, homelessness decreases (I survey the academic findings on the topic here).

This suggests that if we reduce home affordability problems, we can effectively reduce homelessness.

A powerful tool to help ease the housing affordability crisis is subprime mortgage lending – defined as loans made to borrowers with credit scores below 640.

The idea is simple: by helping more low-income tenants qualified to take out a subprime mortgage become homeowners, there’ll be more affordable rental housing available for everyone else. More supply on the market helps reduce average rents, which in turns helps more of those pushed to the streets afford a roof over their heads with less government aid. Thus this makes the policies still based on rental subsidies more effective.

However, this idea cannot be implemented until we fix the subprime mortgage market. As you can see from the graph below, the market has not yet recovered from its collapse in 2008.

The subprime market has yet to recover from its collapse.Inside Mortgage Finance, Author provided

One of the reasons the market collapsed was that investors lost confidence in the ability of loan originators and regulators to use credit scoring models to accurately assess a borrower’s creditworthiness – remember the NINJA loans (no income, no job, no assets)?

This market won’t be back up and running at full strength – and able to help address the affordability crisis – until these credit-scoring models improve and mechanisms are put in place to ensure loan quality remains adequate.

The FHFA sets new goals

There has been some movement to get the subprime market moving again.

The Federal Housing Finance Agency (FHFA), an independent federal agency that regulates Fannie Mae, Freddie Mac and the 12 Federal Home Loan Banks, recently set goals for the next two years meant to expand the availability of mortgages to low-income buyers.

This policy will keep its focus on helping a small segment of borrowers with incomes no greater than 50 percent of their area’s median income to purchase or refinance a single-family home.

But many affordable housing advocates expressed concern that these targets do not go far enough. The Woodstock Institute – a leading research and policy nonprofit organization focused on fair lending, wealth creation and financial systems reform – for example, argued that the policy won’t do enough to promote affordable and sustainable home ownership for low-income families.

How to bring back subprime

Even with the FHFA embracing the idea of expanding the availability of subprime mortgages to low-income buyers, their perceived role in the 2008 crisis and bringing down the housing market may cause justifiable resistance from the general public as a means of tackling the affordability crisis.

And one cannot blame this reaction, as it was the average American taxpayer who bailed out the reckless financial system, brought down by greedy bankers and weak politicians and regulators.

So how we can encourage more subprime lending while avoiding a repeat of 2008? In my recent research, I suggest a few ways to do this.

One of the reasons subprime loans became such a problem in the run-up to the crisis is just the sheer volume (see the boom in subprime lending from 2001 to 2005 in the above graph). This expansion was fueled by the generous homeownership subsidies given to low-income households.

One way to help prevent this is to vary the size of the homeownership subsidy countercyclically to control the amount of credit flowing into the economy and prevent overborrowing during expansionary periods. It would be higher at times when the housing market contracts, and lower when it’s booming.

Another problem was that lenders had an incentive to originate mortgages to borrowers who couldn’t afford them because all the risk was passed along to banks and other investors through collateralized mortgage obligations (CMO) and other sophisticated financial instruments.

The Federal Reserve in conjunction with other regulators could reduce this risk by carefully monitoring how many mortgages lenders keep in their own portfolios. When the share lenders hold increases, they have more incentives to better screen borrowers and thus originate better mortgages.

Lastly, the so-called adverse selection problem on the part of the mortgage originator in the secondary market should also be taken into account. This problem occurs when the mortgage originator has more information about the quality of mortgages that are securitized than the secondary market investors who snap up the CMO. That allows the originator to keep the low-risk mortgages in its own portfolio while distributing the high-risk mortgages to investors.

Improving existing credit scoring models is crucial to ameliorating this problem. Also, the Fed should more carefully monitor the quality of mortgages that are sold to investors and share its information with them. At the very least, that would reduce the investors’ information disadvantage with respect to originators.

Accompanied by the right means to regulate the housing market, we can support subprime while avoiding the disastrous outcomes highlighted in “The Big Short.“ And we can create an environment in which making low-cost mortgages available to people helps resolve the problem of unaffordable housing and homelessness.

Author: Jaime Luque, Assistant Professor, Real Estate & Urban Land Economics, University of Wisconsin-Madison

Governor Lael Brainard, spoke at the 2016 U.S. Monetary Policy Forum, New York, New York. The speech highlighted that whilst there was a phase when different economic centres were diverging, now there are more common elements, including low growth, low interest rates and low inflation. Global shocks are being transmitted via the financial system, creating volatility and spillover effects.

To the extent that we are observing limited divergence in inflation outcomes and less divergence in realized policy paths than many anticipated, this could be attributable to common shocks or trends that cause economic conditions to be synchronized across economies. The sharp repeated declines in the price of oil have been a major common factor depressing headline inflation and are also likely feeding into low core inflation, although to a lesser extent. As noted previously, these price declines have led headline inflation across the globe to behave quite similarly over this time period. Even so, most observers expect this source of convergence in inflationary outcomes to eventually fade and thereafter not affect monetary policy paths over the medium term.

In contrast, a more persistent source of convergence may be found in an apparent decline in the neutral rate of interest. The neutral rate of interest–or the rate of interest consistent with the economy remaining at its potential rate of output and inflation remaining at target level–appears to have declined over the past 30 years in the United States and is now at historically low levels. Similarly, longer-run interest rates appear also to have fallen across a broad group of advanced and emerging market economies, suggesting that neutral rates are at historically low levels in many countries around the world and near or below zero in the major advanced foreign economies. Although the reasons for the declines in neutral rates are not perfectly understood and may differ across countries, there are some common drivers, such as slower productivity and labor force growth and a heightened sensitivity to risk.

The very low levels of the shorter run neutral rate reflect in part headwinds from the crisis that are likely to dissipate over time. However, if many of the common forces holding down neutral rates prove persistent, then neutral rates may remain low through the medium term, implying a shallower path for policy trajectories.

The global economy is also experiencing a downshift in emerging market growth momentum led by China, which may prove somewhat persistent. Whereas earlier in the recovery there was a striking divergence between the relatively buoyant growth in major emerging economies and depressed growth in advanced economies, lately the extent of divergence has diminished noticeably. China is undergoing a challenging set of economic transitions. Trend growth has slowed substantially and is expected to slow further, and the composition of growth is shifting away from resource-intensive manufacturing and exports toward a greater share for consumption and services. China’s investment has slowed sharply recently after accounting for nearly one-third of global investment over the past three years and about one-half of global consumption in certain metals such as iron ore, aluminum, copper, and nickel. Commodity exporters and close trading partners in Asia will be most affected, but the changes in the composition and rate of growth in a country that has accounted for about one-third of the growth in world output and trade will likely ripple through the global economy much more generally.

Amplified Spillovers

Of course, policy divergence among major economies could be limited by rapid and strong transmission of foreign shocks across borders. In particular, although the U.S. real economy has traditionally been seen as more insulated from foreign trade shocks than many smaller economies, the combination of the highly global role of the dollar and U.S. financial markets and the proximity to the zero lower bound may be amplifying spillovers from foreign financial conditions. By one rough estimate, accounting for the net effect of exchange rate appreciation and changes in equity valuations and long term yields, over the past year and a half, the United States has experienced a tightening of financial conditions that is the equivalent of an additional increase of over 75 basis points in the federal funds rate.10

The transmission of divergent economic conditions across borders typically occurs though a couple of different channels. First, a decline in demand in one country reduces its demand for imports from other countries. Second, the fall in economic activity would be expected to trigger a more accommodative monetary policy, which helps offset the effect of the shock by both supporting domestic demand and weakening the exchange rate. The weaker exchange rate in turn leads domestic consumers to switch their expenditures away from more expensive foreign imports to cheaper domestic products while increasing the competitiveness of exports. The extent to which monetary policy offsets the shock by dispersing it to trade partners as opposed to strengthening domestic demand depends on the responsiveness of domestic demand relative to the exchange rate. The exchange rate channel, by raising the price of imports in domestic currency, also pushes up domestic inflation and exerts downward pressure on foreign inflation.

The strength of spillovers across countries and the extent to which that affects policy divergence across countries depend on a foreign economy’s openness to these different channels. The recent experience of Sweden suggests that for highly open economies, the effect of foreign shocks can be extremely powerful. Sweden’s economic growth has been relatively rapid recently, reaching nearly 4 percent over the most recent four quarters. Moreover, the employment gap is estimated to be nearly closed, and there are signs of financial excess in the housing market. In ordinary times, these conditions would be consistent with relatively tight monetary policy. However, inflation has run persistently well below the central bank’s 2 percent inflation target. Given the relative openness of Sweden’s economy, moving the inflation rate back up to target has been greatly complicated by the sensitivity of Sweden’s exchange rate and financial conditions to developments in the euro area, where domestic economic conditions are consistent with much more accommodative policy. As a result, the Riksbank has been pursuing extremely accommodative monetary policy, most recently lowering the interest rate on deposits to minus 0.5 percent and authorizing the Governor and Deputy Governor to intervene in foreign currency markets.

Even in the much larger United States economy, with imports accounting for a little over 15 percent of gross domestic product (GDP), spillovers can be quite strong, in part reflecting the international role of U.S. financial markets and the dollar. Since the middle of 2014, with a reassessment of demand growth in the euro area and subsequently in emerging markets and other commodity exporters, the real trade-weighted value of the dollar has increased nearly 20 percent. As a result, in 2014 and 2015, net exports subtracted a little over 1/2 percentage point from GDP growth each year, and econometric models point to a subtraction of a further 1 percentage point this year.12 In addition, the dollar’s appreciation is estimated to have put significant downward pressure on inflation: Non-oil import prices fell 3-1/2 percent in 2015, subtracting an estimated 1/2 percentage point from core PCE inflation.

Financial channels can powerfully propagate negative shocks in one market by catalyzing a broader reassessment of risks and increases in risk spreads across many financial markets. Since the beginning of the year, U.S. financial markets have reacted strongly to adverse news on emerging market growth, even though the news on the U.S. labor market has remained positive. In this regard, although China’s direct imports from the United States are modest, uncertainty about changes to its exchange rate system and financial imbalances, together with changes in the composition of its growth, have had broader global spillovers that may pose risks to the U.S. outlook.

Recent events suggest the transmission of foreign shocks can take place extremely quickly such that financial markets anticipate and indeed may thereby front-run the expected monetary policy reactions to these developments. It also appears that the exchange rate channel may have played a particularly important role recently in transmitting economic and financial developments across national borders. Indeed, recent research suggests that financial transmission is likely to be amplified in economies with near-zero interest rates, such that anticipated monetary policy adjustments in one economy may contribute more to a shifting of demand across borders than a boost to overall demand. This finding could explain why the sensitivity of exchange rate movements to economic news and to changes in foreign monetary policy appear to have been relatively elevated recently.

Financial tightening associated with cross-border spillovers may be limiting the extent to which U.S. policy diverges from major economies. As policy adjusts to the evolution of the data, the combination of heightened spillovers from weaker foreign economies, along with a lower neutral rate, could result in a lower policy path in the United States relative to what many had predicted.

Policy

In circumstances where many economies face common negative shocks or where negative shocks in one country are quickly transmitted across borders, it is natural to consider whether coordination can improve outcomes. Under certain conditions–such as flexible exchange rates, deep and well-regulated financial markets, and flexible product and labor markets–policies designed for the domestic economy can readily offset any spillovers from economic conditions abroad, and policies designed to address domestic conditions can achieve desirable outcomes both within the national economy and more broadly.

In some circumstances, however, cooperation can be quite helpful. If, for example, economies face a common challenge, coordination can communicate to markets that policymakers recognize the challenge and will work to address it. Reducing uncertainty about the direction of policy and addressing concerns about policies working at cross-purposes can boost the confidence of businesses and households. With intensified transmission effects in the vicinity of the zero lower bound, there is a risk that uncoordinated policy on its own could have the effect of shifting demand across borders rather than addressing the underlying weakness in global demand. The difficult start to the year should be a prompt for greater policy coherence and clarity. This might be a good time for policymakers to reaffirm their commitment to work toward the common goal of strengthening global demand.

Similarly, with anemic global demand and interest rates near zero, in some economies there is scope for monetary policy to be more effective with fiscal policy working in the same direction. With potential growth and nominal borrowing rates both low, public investment that increases potential in the longer run and demand in the shorter run could make an important contribution. A joint determination by policymakers across major economies to better deploy policy tools to provide support for global demand could be beneficial.

The Mortgage and Finance Association of Australia (MFAA) has branded a report in the Australian Financial Review (AFR) – which questions the ethics of mortgage brokers and likened some to a Ponzi scheme – as a “serious allegation”.

The AFR report, titled ‘Uncovering the big Aussie short’ claims mortgage brokers in the western suburbs of Sydney encouraged the undercover hedge-fund manager and economist posing as a low income couple to lie on loan application documents about the deposit for a house and about income.

Jonathan Tepper, economist and founder of Variant Perception, wrote in a report, “we asked if the bank would call our employer, and both reputable and disreputable brokers said banks rarely verified payslips”.

John Hempton, Bronte Capital’s chief investment officer added that they were also told the checking of documents was sometimes done by Indian call centres.

Tepper and Hempton also claimed they encountered many investors who were able to get revaluations on their properties to increase their equity for speculative purposes.

According to Hempton, in north-western Sydney they met one mortgage broker who told them which of the big four banks would revalue properties quickly.

“They wanted to put you in 10 to 15 apartments. The only way they could do that was getting the bank to revalue the property so you could borrow more money. They were acute about which banks had bad practices,” the AFR report quotes Hempton.

Siobhan Hayden, the chief executive of the MFAA, says this sort of behaviour has no place in the mortgage broking industry and she is calling on the AFR to provide the names of the offending brokers.

“The practices of brokers are well documented and require the provision of supporting upfront documents such as payslips, group certificates, tax returns and identification check as part of the upfront application. Lying has no place in this industry and we take swift action if members are acting unethically. It should also be noted that brokers who act outside of the law represent an incredibly small portion of the industry,” Hayden said.

“We call on the AFR or the research firm provides the names of these mortgage brokers, as the MFAA has a strict code of practice and ethics attached to its membership. If these are MFAA members we would initiate a full investigation and work in partnership with the industry regulator, ASIC.”

She is also condemning the authors of the report, Tepper and Hempton, as well as the AFR for not seeking out either industry body for comment.

“We would have hoped that with any story of this nature the industry body would have been contacted to seek commentary and supporting data for validation. The article is based on invalid research samples sizes and infers that overseas outsourcing of administration is somehow inferior. Both sides of the story should be told.”

Hayden also pointed to the ‘Observations on the value of mortgage broking’ report, commissioned by the MFAA and prepared by Ernst & Young, which showed that 92% of consumers who had used a broker were satisfied with the experience, stating that the convenience and access to a range of suitable deals were the best qualities.

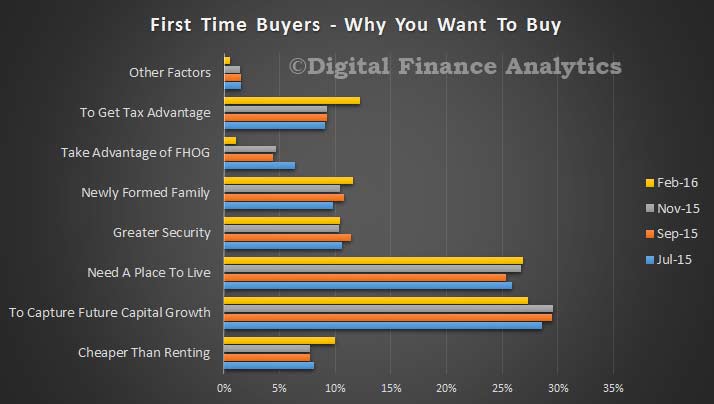

Continuing our series on the results from our latest household surveys, today we look at first time buyers. Data from our surveys, combined with recently released ABS data, highlights that first time buyers are more active now compared with last year. Whilst many first time buyers are seeking to buy a place to call home, an increasing number are looking to go direct to the investment sector to buy a cheaper place as a means of getting on the property ladder, assisted by tax breaks and negative gearing. This trend continues to build.

So, looking at first time buyer motivations, we find that prospective capital growth is the strongest driver (27%), compared with needing a place to live (26%). Significantly, tax advantage figures as a decision driver (12%), up from 9% last year. This is worth noting in the context of the current quasi-discussion about negative gearing! The fact that buying is cheaper than renting (10%), up from 8% last year influences the decision, as does forming a family (12%). The potential to access first home owner grants (FHOG) has reduced in importance as their availability has diminished (and that is a good think, because FHOG’s simply are another market distortion).

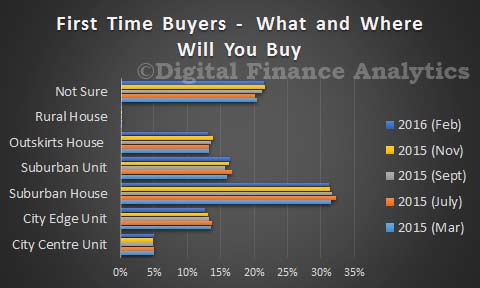

Many first time buyers are not all that sure where to buy, with a high 21% saying there is no simple choice. A significant proportion (33%) will look for a unit whilst nearly 60% still want to buy a house.

Most prospective first time buyers going direct to the investment sector are seeking to buy a unit, as the purchase price will be significantly lower. Purchasing preference is spread from CBD (12%), city fringe (35%) and suburban outskirts/regional centres (23%). Underlying this is a strong motivation to get onto the housing escalator anyway they can. We also noted that around 35% of prospective first time buyers were expecting to get help from the wider family to assist in the purchase, so the “bank of mum and dad” remains an important factor in the first time buyer equation. Yesterday we highlighted that more than half of prospective first time buyers believe house prices will continue to rise – so they wish to transact to avoid seeing prices move further against them and to enjoy capital appreciation at a time when interest rates are really low. Property purchase is hard wired into the Australian psyche.

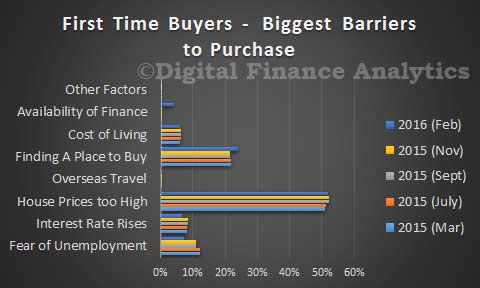

Finally, there are a number of barriers first time buyers are encountering. More than half think property prices are too high (this has been pretty constant in recent surveys), 22% said they were having difficulty finding a place to buy (lack of supply, and competition with investors – both local and overseas) and around 5% said that they are finding it difficult to get finance. This reflects tightening lending criteria and flat incomes in real terms and is a marked change from last year. More than 60% of first time buyers will be consulting a mortgage broker to assist with finding a loan.

Next time we will do a deep dive on the refinancing sector.

There is much confusion about the effects of Labor’s tax proposals with respect to investors in rental housing. They propose to grandfather existing arrangements. But investors in the future can only negatively gear newly constructed housing, while the policy recommends the capital gains discount fall from 50% to 25%.

Claims by Prime Minister Malcolm Turnbull that house prices will collapse appear to be contradicted by his assistant treasurer Kelly O’Dwyer who claims that housing costs will soar. These puzzling assertions arise due to a failure to distinguish between the market in rental housing, where housing is leased, and the market in which investors and owner occupiers buy and sell housing. Critically these two markets are interrelated.

To see why, consider the first round effects of Labor’s proposals when we put the grandfathering arrangements to one side (for the moment). Some existing investors will sell up when leases come up for renewal. There are now more tenants seeking rental housing opportunities than there is supply to meet their demand. Rents will begin to rise.

But the houses which investors quit add to the properties available for sale; there are now more houses available for purchase than there are buyers. House prices will begin to fall.

These market signals trigger a second round of effects. Some tenants will elect to buy rather than rent. After all renting has become more expensive and home ownership has become cheaper. These second round effects help to put a floor under falls in house prices, and help cap rent rises.

By considering the inter-relationships between the two markets we can understand how the government has issued apparently contradictory statements. Rents will rise and so the housing costs of tenants will increase. But there will be falls in house prices (or more likely a slower growth in prices); while existing owners take a hit, first home buyers housing costs are lower and attainment of home ownership becomes more affordable.

The second round effects mean that impacts are likely to be muted. This is made even more likely by a grandfathering proposal that should prevent a stampede by existing investors seeking to relinquish their property investments.

A disappointing aspect of the debate so far has been its neglect of the longer term structural consequences of Labor’s suggested reforms. Our current arrangements encourage high tax bracket investors to take on debt in the “chase” for capital gains. Capital gains are leniently taxed as compared to ordinary sources of income, such as earnings and rents.

Only 50% of capital gains are added to assessable incomes. This is particularly attractive to high tax bracket investors. Moreover, they are taxed on realisation rather than as they accrue. The shrewd investor realises the gains when assessable income from other sources declines; for example, following retirement when the investor’s marginal tax rate commonly falls.

There are not enough high tax bracket investors willing and able to invest in all our private rental housing stock. They tend to cluster in those segments of the market where healthy capital growth is expected, but rental yields are lower. Low tax bracket investors tend to cluster in segments where capital growth is expected to be subdued. Typically these are areas with lower house prices. To ensure adequate returns rental yields have to be higher in these low house price segments.

We therefore get a distorted investment pattern that disadvantages the supply of affordable rental housing.

Labor’s proposals will curb these distortionary effects by reducing the capital gains discount. They will also reduce the tax incentives to leverage investments. Rising indebtedness is a threat to the resilience and stability of our housing market.

Many believe that repayment and investment risks carried by heavily indebted home buyers played a central role in precipitating the global financial crisis. Tax concessions that favour taking on debt exacerbate those risks. If Labor’s proposals succeed in attracting attention to these and other structural problems that plague Australian housing markets, they will have a much wider significance.

Author: Gavin Wood, Professor of Housing, RMIT University

Journalism is in an existential crisis: revenue to news organisations has fallen off a cliff over the past two decades and no clear business model is emerging to sustain news in the digital era.

In the latest in our series on business models for the news media, journalist and academic Jane Singer looks at the use of micropayments.

Once upon a time, the gap between the relatively low supply of something in high demand – timely and trustworthy information – generated enormous profits for news publishers. But over the past 15 years or so, the digital, social and mobile revolutions have all but obliterated that gap.

In response, publishers have scrambled for new revenue streams, and much recent attention has turned to “micropayments” – the payment of a very small amount to access a comparably small bit of content, such as a single story.

The traditional media world is one of bundled information, with a lot of diverse content in one package that aims to provide something for everyone. The digital world, though, is an unbundled one. It enables each individual to select one item at a time from among the billions of things on offer. Are we willing to pay for this content? Sometimes yes – see iTunes.

But the question for news outlets is whether personalised news can follow the lead of personalised entertainment in generating interest and – in their fondest dreams – income.

Blendle is poised to take on the US market.Blendle

So far, news micropayment initiatives are – at best – a work in progress. The most buzz has been around a Dutch service called Blendle, which claims half a million registered users in Europe and is poised to tackle the US market. Most items on Blendle, which come from diverse outlets, cost between 10 cents and 90 cents and come with a money-back guarantee: you only pay for stories you actually read – and if you then don’t like them, you can ask for your pennies back.

The slick interface appeals to fans, as does the lack of advertising (and advertising’s attendant clickbait). But others have flatly predicted the concept is doomed to fail. News consumers want to pay nothing, they say, and even a very small amount of money is not nothing.

Who pays the piper?

But perhaps the model here is not an “iTunes for journalism”, if by journalism we mean big-name branded content. Perhaps a crowdfunding site such as Kickstarter offers a better template – the ability for users to stack their coins behind ideas they want to see developed rather than existing stories they want to read.

Experiments with crowdfunded journalism have proliferated. One flavour is essentially a low-cost membership model that allows its member – or donors – to steer journalists to topics of interest. MinnPost, a non-profit site in Minnesota, has made good use of this approach. For instance, a New Americans beat, which covers the state’s immigrant and refugee communities, was launched last October based on pledges from interested donors.

In Scotland, a new investigative journalism site called The Ferret also pursues topics that its users say they want; fracking was an early example. And in the Netherlands, de Correspondent drew donations of more than a million euros in just eight days simply on the promise of delivering high-quality stories about important topics rather than “the latest hype”.

The other approach reverses the process, in a way, and is closer to the familiar crowdfunding concept – journalists propose ideas they would like to pursue and users back the ones they like. Stories that meet their funding target get written; those that don’t, don’t. Perhaps the most innovative example came from a British site called Contributoria, backed by the Guardian Media Group. Over a period of 21 months in 2014 and 2015, Contributoria published nearly 800 articles on topics from urban regeneration in Beirut to a day in the life of a bookie; its writers earned a total of £260,000 over that time, most of it built up from quite small individual payments.

Sustainability

However, such experiments have proved hard to sustain. Contributoria closed in October 2015, with its co-founder declaring that crowdfunding was just one piece of the puzzle. What the initiative really showed, he told journalism.co.uk, was that people have a “voracious appetite … to be part of the journalism process, including the way it gets financed”.

Perhaps that is, for now, the takeaway point on micropayments. The desire being given voice is less about paying for journalism than for having a stake in it. News organisations fervently hope that stake will be financial, but for users, “ownership” of the news seems more important than the payment involved.

As information proliferates wildly, consumers are saying they want a sense of control over it. Digital media gives them the ability to be reporters, but mostly, they seem to want to be editors: the gatekeepers who decide what news they will see by commissioning a freelance article, or steering an investigative team toward a topic, or engaging with this niche news app but not that one.

Getting the mix right

For news organisations, then, micropayments are just one option among many in a fragile and fractured digital ecosystem – something to add to the revenue mix if doing so requires only small investments of time, effort or money.

While experimentation is all to the good, the pay-off from this option seems inherently small. The vast majority of online users do not pay now for digital news and have no plans to change their ways. There’s no evidence of a massive demand from users for the ability to pay upfront to read news content – and, even if there were, the small amount of revenue generated on any given day would fluctuate considerably depending on what was on offer. This is not the most desirable funding model for organisations that need a stable financial base to support staff, infrastructure and the ongoing ability to hold the powerful to account.

The reverse option – enabling news consumers to steer the direction of journalistic investigations – seems more plausible and the various non-profit enterprises I’ve mentioned are among those offering examples of ways this might work.

But news users aren’t the only ones who like to be in control. Journalists tend to be fiercely committed to the notion of editorial independence – which is another way of saying that they like to decide for themselves what is and isn’t news. Whether they will be willing to share that control – and, if so, what they might be able to extract from users in exchange – remains to be seen.

Author: Jane B. Singer, Professor of Journalism Innovation , City University London

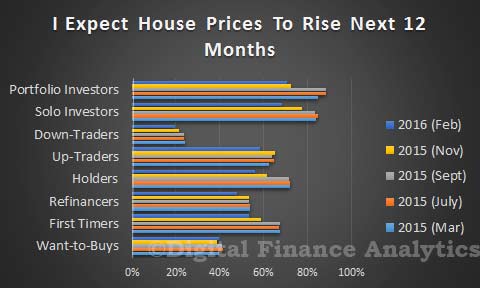

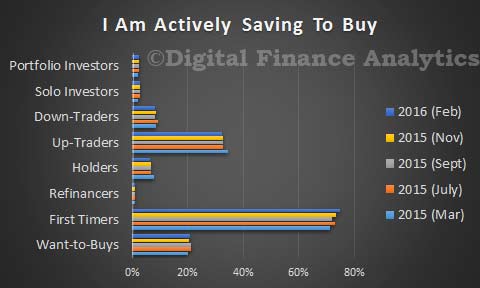

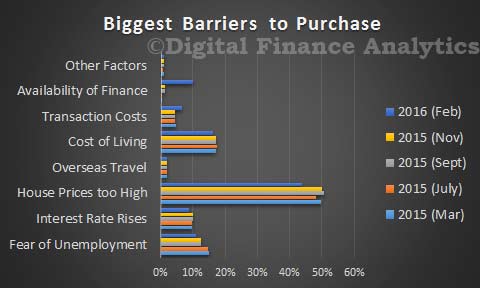

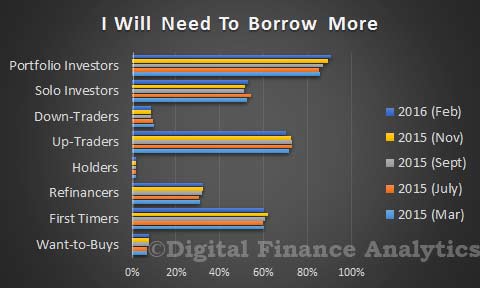

The latest results from the Digital Finance Analytic Household Surveys are in, and demand has recovered somewhat after the wobble late last year. Worth also remembering that Sirens were dangerous yet beautiful creatures, who lured nearby sailors with their enchanting music and voices to shipwreck on the rocky coast of their island! Over the next few days we will present the summary results, using our household segmentation, and examine why property remains so alluring despite being in bubble territory.

By way of background, we are using data from our rolling 26,000 household data set, the most recent data is up to 20th February 2016, so this captures the state of play after the recent stock market and resource sector ructions. Today we will overview some of the main cross-segment data, and in later posts dive into more detailed analysis of specific segment behaviour. These results will then flow into the next edition of the Property Imperative – the last edition is still available from September 2015, and the new edition will be out in March.

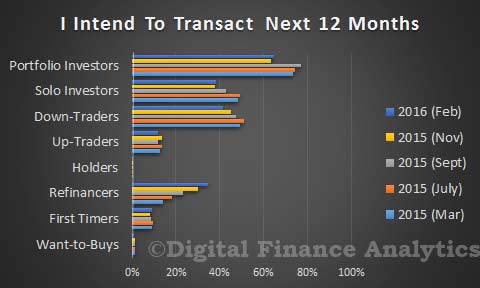

We start with transaction intentions. The most significant move is the rise in those expecting to refinance their existing mortgage, from 29% last time to 34% now. This despite record refinance volumes which have already been written. We found that many households were reacting to the strong discounts available for existing borrowers, especially with loan-to-value ratios below 80%. Three quarters of these households will use a broker, so no surprise we see brokers volumes on the rise. First time buyers are still in the market, from 8.2% to 8.9% this time. Property investors, whether holding a portfolio of properties, or just one, are still in the market, despite the rise in interest rates for investment loans, and tighter lending criteria. Portfolio investors moved form 63% to 64% this time, whilst solo investors moved from 37% to 38%. Up traders and down traders are a little less inclined to transact, whilst those wanting to buy, but who cannot, remain on the sidelines.

House price rise expectations are still quite strong, though lower than at their peak last year. More than half of property investors still think the market will go higher in the next 12 months. Down traders are the least optimistic with only 20% expecting further price hikes. First time buyers are still bullish, with 53% expecting a rise, though a fall from 67% last year.

Savings behaviour has not changed that much, with first time buyers still saving the hardest. Some of those wanting to buy are also saving, but it continues to sit at around 20%.

Of note is the significant rise in households who say that availability of finance is now a barrier to transacting, with nearly 10% saying finding a loan is now a problem compared with just 1.5% last year. Of course house prices remains high, so 43% say this is a barrier to transacting, down from 49% last year. On the other hand, unemployment fears are down compared with last year, down from 15% to 11%.

Prospective purchasers are still looking for finance, with investors and first time buyers seeking to borrow more. Around 15% of those refinancing will look to increase the size of their loan, which explains some of the ongoing loan portfolio growth noted in recent statistics.

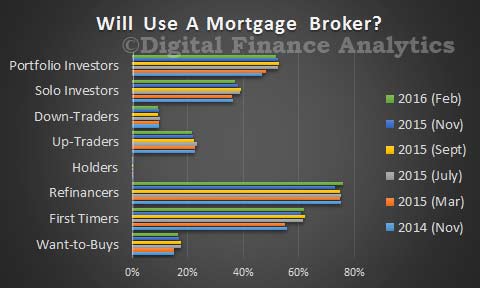

Finally, in this over view, we note the importance of mortgage brokers as noted in the recent APRA data, with first time buyers and those seeking to refinance the most likely to consult a broker. Investors are also still broker aligned, especially portfolio investors.

So, the expectations are for ongoing demand for property still to be strong, and refinance volumes will remain elevated. Banks are competing hard to offer deep discounts for owner occupied loans. Next time we will look in more detail at first time buyers, and then those seeking to refinance.