The year is off to a turbulent start; both in the UK, and around the world. January saw oil prices plummeting, while Chinese growth slowed, spooking investors (but surprising none). But amid the turmoil and confusion of global stock markets, there are a few economic trends which look set to hold sway throughout 2016.

Here’s a wrap up of some of the key developments which will shape our society in the months to come.

Employment for women

Many developed economies are experiencing a rise in total employment. And in most cases, it comes down to one critical factor: the growing number of women joining the work force. This represents one of the biggest social changes of modern times. For example, in the UK, the employment rate for women is the highest since records began, at 68.8% – in part due to the ongoing equalisation of men and women’s retirement ages.

Of course, there are still huge discrepancies between the economic rights and opportunities available for women across the globe. But ultimately, nations where women do not work lose out. Research shows that women’s skills in the labour force add much value to a national economy. Granted, this is partly related to the low pay and promotion inequality facing women, and more progress is needed to address these issues.

Women at work.from www.shutterstock.com

Expect to see women’s employment continuing to rise, and to be associated with economic growth and wider social benefits, despite global economic challenges. In 2016, countries and organisations that give positive employment opportunities to women will have greater chances of doing better, even in tough times.

The debt trap

While women’s employment may inspire hope in today’s challenging economic environment, credit and debt trends offer less reassurance. After the financial crisis, governments and central banks busted a gut to pump money into the banks and get them lending. But there is currently a feeling of déjà vu – as though the world could very easily experience another credit crisis in 2016. There are two clear signs: one in the UK, and one abroad.

Carney’s conundrum.Pool/Reuters

The first one is that premier league central banker Mark Carney – who transferred from Canada to the Bank of England as the ultimate master of inflation – now has a curious problem. He cannot find any inflation to master.

A little inflation is good for the economy, a bit like one glass of wine a week for health. The UK economy currently gets nowhere near its target of 2%. Inflation would decrease the value of current debts, making them less of a burden. In a world without much inflation, it is hard to get wages up. The worse case scenario is that debt costs increase, as prices and wages stagnate.

Elsewhere, the small interest rate rise in the US has made credit more expensive for many. Businesses in rapidly developing countries, which borrowed when the dollar was cheap, look vulnerable. For countries tied into dollar-based lending, there’s cause to fear the appreciation of the dollar against their local currency.

Expect debt statistics to go on spooking commentators throughout 2016. Look for a different policy approach that tries to kick start credit via governments and central banks. New strategies will be needed to get money to the parts of the economy that can enhance productivity and pay real, long-term rewards, such as renewable energy. Better this, than for credit to inflate existing assets such as current housing stock, or company merges and acquisitions.

A transport boom

Speaking of productive growth – transportation has been a key growth area in the world economy, and looks set to continue on this path.

In the UK, the railways have been a growth area for two decades, with more investment planned, albeit not without political pitfalls. And China has seen extraordinary growth in high speed rail development and use.

Meanwhile, air transportation grew globally in 2015 and “hub” countries such as the UK and Gulf States benefit from this. Low oil prices make flights cheaper and encourage growth. Air transportation in the UK is ripe for expansion, but is linked to a difficult political decision over London’s runways.

Business is booming.from www.shutterstock.com

Global car sales continue to rise at a time when oil is cheap. And while the number of electric cars grew more rapidly in 2015, they still represent a small proportion of the total.

This productive growth in transportation has to be debated alongside the need for the uptake of greener technology. Many governments know the ultimate prize will be getting ahead with the production of electric cars and the infrastructure they require, in order to reduce pollution and improve health.

For example, the UK government just financed four UK cities to provide better charging and parking facilities for electric vehicles. In London, the mayoral candidate, Zac Goldsmith, has clearly linked electric cars with a sustainable environment and proposes financial incentives to encourage their use. Tesla in the US has invested huge amounts gambling that the electric car will become more popular. Fortune favours the brave.

Expect to see continuing growth in rail and air travel. Meanwhile, the countries and companies that invest to get ahead with electric cars and other green transport options are likely to see the biggest long term returns. Oil will not stay at $30 a barrel forever.

Young people in poverty

Another key trend is the increase in the poverty experienced by young adults. A growing number of students in the UK are exiting with greater long term debt, while Australia is implementing measures to ensure student loans are paid. In the US, student debt now stands at $1.3 trillion.

Where’s my piece of the pie?www.shutterstock.com

As well as debt, housing will be a major issue for this group. The price of property is increasing in major cities such as Sydney, Vancouver, London and New York: these markets require high deposits, and rents are rising. In the UK, this is making the generation gap worse, when it comes to wealth: those aged 50 and over own most of the UK’s asset wealth, including housing.

And in this age of austerity, these factors will work against governments seeking to reduce the welfare bill. Recent data shows that, in UK cities, growing numbers of low paid jobs have led to rising claims for welfare such as housing benefits, defeating the government’s aims to reduce spending.

These major challenges for young people prevail across most developed countries. Expect young adults to be increasingly dependent on wealth transfers from their parents to clear university debt and secure housing, while those without such support face increasing disadvantages. Only major changes in policy can prevent further inequality for this generation.

Politicians are prioritising the needs of the growing older population who are living longer. But the young are paying the price in lost opportunities and look vulnerable to further economic and social change.

Author: Philip Haynes, Professor of Public Policy, University of Brighton

As part of the legislative package implementing the recommendations of the Independent Commission on Banking in the UK, the Financial Policy Committee (FPC) is required to produce a framework for a systemic risk buffer (SRB) for ring-fenced banks and large building societies.

The SRB is one of the elements of the overall capital framework for UK banks and building societies as set out by the FPC in its publication ‘The framework of capital requirements for UK banks’, which was published alongside the December 2015 Financial Stability Report.

The SRB will be applied to individual institutions by the Prudential Regulation Authority (PRA) and will be introduced, like the ring-fencing rules, from 2019.

Deputy Governor, Financial Stability, Jon Cunliffe said:

“These new rules will mean that large UK banks and building societies are more resilient to adverse shocks, enabling them to continue to lend to households and businesses even in times of stress. The financial crisis demonstrated the long-lasting damage that can be caused when large banks become distressed and have to cut back lending to the economy. These proposals are intended to reduce the risk of this happening again.”

Summary of the proposals

It is proposed that those banks and building societies with total assets above £175bn will be set progressively higher SRB rates as total assets increase through defined buckets (see table below). HM Government required the FPC to produce a framework for the SRB at rates between 0% and 3% of risk-weighted assets (RWAs). Under the FPC’s proposals, ring-fenced bank sub-groups and large building societies in scope with total assets below £175bn will be subject to a 0% SRB.

Based on current information, under these proposals the FPC expects the largest ring-fenced bank in 2019 to have a 2.5% SRB. In line with the FPC’s previous announcement on the leverage ratio framework, those institutions subject to the SRB will also be set a 3% minimum leverage ratio requirement, together with an additional leverage ratio buffer calculated at 35% of the applicable SRB rate. For example, an institution with an SRB rate of 1% would have an additional leverage ratio buffer of 0.35%.

As stated in the FPC’s capital framework document in December, the proposed calibration is expected to add around an aggregate 0.5 percentage points of risk-weighted assets to equity requirements of the system in aggregate.

Total Assets (£bns)

Risk weighted

SRB rate

Lower threshold

Upper threshold

0%

-

<175

1%

175

<320

1.5%

320

<465

2%

465

<610

2.5%

610

<755

3%

≥755

The consultation will close on 22 April and the FPC intends to finalise the framework by 31 May 2016. The buffer will apply from 2019.

Smaller banks are likely to have to set aside more Pillar 1 capital to cover potential market risks when the Basel Committee on Banking Supervision’s (Basel Committee) revised market risk framework comes into force in 2019, says Fitch Ratings. This is because banks using the standardised approach to calculate market risk capital requirements, including the bulk of second-tier, less sophisticated banks, will face steeper capital charges once they apply the revised approach.

Impact studies conducted by the Basel Committee show that, for a sample of 44 banks using the standardised approach for market risk, median market-risk capital requirements rise by 80% when the revised standardised guidelines are applied.

But on the whole, market risk is low as a proportion of overall risks faced by banks and the additional capital to be earmarked for market risk under the new rules should not be too onerous. The Basel Committee says that the revised framework produces market risk-weighted assets (RWA) that account for less than 10% of total RWAs, higher than the current framework’s 6%, but still low as a proportion of the total.

The standardised approach for market risk capital calculation is still widely used, especially by banks with limited trading activity or those lacking regulatory approval to use internal models. But some banks involved in straightforward commercial banking have sizeable derivative portfolios to hedge currency- and interest-rate risks.

For these banks, revised capital requirements could be more onerous, depending on the complexity of the instruments. Under the revised approach, capital charges will rise for interest rate, credit, FX and commodity derivatives. Exotic derivatives that cannot be broken down into vanilla constituents, or with complex underlyings, and instruments with embedded optionality will attract a residual risk add-on charge, ranging from 0.1%-1% of the gross notional value of the derivative.

Revisions to the standardised approach will overcome some shortcomings in the current framework, which was last amended in 1996. The new framework amends the assumption that all positions can be sold or hedged within 10 days and addresses both the inability to assign capital based on pricing model sensitivities and the failure to fully capture risks associated with credit products, such as credit spread and jump-to-default risks.

Under the new regime, the revised standardised approach will be the fall-back to the internal models-based approach, meaning that banks with internal model approval will still be required to compute capital under the revised standardised approach. The new framework harmonises key sensitivities and calibrations used under the revised standardised and revised models-based approaches. By sharing methodologies used for assessing tail-risks under stressed market conditions and variation in liquidity horizons, comparing results should become more straightforward. This should simplify the application of the revised standardised approach as a fallback if required.

Banks with large trading books use internal models to calculate market risk capital requirements and the Basel Committee’s new framework also overhauled the models-based approach.

Structural flaws in the way banks calculated capital charges for market risk were exposed during periods of severe market stress at the height of the 2008-2009 financial crisis. Post-crisis, the Basel Committee undertook a fundamental review of the trading book. The original proposals were watered down, but we think the final revised minimum capital requirements for market risk will be positive for creditors because traded market risks will be more rigorously capitalised, with banks using more risk-sensitive approaches, rather than the current simplistic and outdated approach.

In a surprise decision, the Bank of Japan (BoJ) has announced a policy of negative interest rates in an attempt to boost the country’s flagging economy.

“At the Monetary Policy Meeting held today, the Policy Board of the Bank of Japan decided to introduce “Quantitative and Qualitative Monetary Easing (QQE) with a Negative Interest Rate” in order to achieve the price stability target of 2 percent at the earliest possible time. Going forward, the Bank will pursue monetary easing by making full use of possible measures in terms of three dimensions; quantity, quality, and interest rate”.

In a 5-4 vote, the Bank of Japan’s board imposed a 0.1% fee on deposits left with the Bank of Japan, effectively a negative interest rate, from the reserve maintenance period, which commences from February16, 2016.

The authorities hope negative interest rates will encourage commercial banks to lend more to promote investment and growth, and drive inflation higher. Latest data showed that Japan’s inflation rate came in at 0.5% in 2015, well below the BoJ’s 2.0% target.

This experiment takes Japan into new and uncharted territory.

“Japan’s economy has continued to recover moderately, with a virtuous cycle from income to spending operating in both the household and corporate sectors, and the underlying trend in inflation has been rising steadily. Recently, however, global financial markets have been volatile against the backdrop of the further decline in crude oil prices and uncertainty such as over future developments in emerging and commodity-exporting economies, particularly the Chinese economy. For these reasons, there is an increasing risk that an improvement in the business confidence of Japanese firms and conversion of the deflationary mindset might be delayed and that the underlying trend in inflation might be negatively affected”.

The Bank will adopt a three-tier system in which the outstanding balance of each financial institution’s current account at the Bank will be divided into three tiers, to each of which a positive interest rate, a zero interest rate or a negative interest rate will be applied, respectively.

1. The Three-Tier System

(1) Basic Balance: a positive interest rate of 0.1 percent will be applied With regard to the outstanding balance of current account at the Bank that each financial institution accumulated under QQE, the Bank will continue to apply the same interest rate as before. The average outstanding balance of current account, which each financial institution held during benchmark reserve maintenance periods from January 2015 to December 2015, corresponds to the existing balance and will be regarded as the basic balance to which a positive interest rate of 0.1 percent will be applied.

(2) Macro Add-on Balance: a zero interest rate will be applied A zero interest rate will be applied to the sum of the following amounts outstanding.

a) The amount outstanding of the required reserves held by financial institutions subject to the Reserve Requirement System

b) The amount outstanding of the Bank’s provision of credit through the Loan Support Program and the Funds-Supplying Operation to Support Financial Institutions in Disaster Areas affected by the Great East Japan Earthquake for financial institutions that are using these programs c) The balance calculated as a certain ratio of the amount outstanding of its basic balance in (1) (macro add-on). The calculation will be made at an appropriate timing, taking account of the fact that the outstanding balances of current accounts at the Bank will increase on an aggregate basis as the asset purchases progress under “QQE with a Negative Interest Rate.”

(3) Policy-Rate Balance: a negative interest rate of minus 0.1 percent will be applied A negative interest rate of minus 0.1 percent will be applied to the outstanding balance of each financial institution’s current account at the Bank in excess of the amounts outstanding of (1) and (2) combined.

Also, the Bank decided, by an 8-1 majority vote, to set the following guideline for money market operations for the intermeeting period. The Bank of Japan will conduct money market operations so that the monetary base will increase at an annual pace of about 80 trillion yen.

“a) The Bank will purchase Japanese government bonds (JGBs) so that their amount outstanding will increase at an annual pace of about 80 trillion yen.3 With a view to encouraging a decline in interest rates across the entire yield curve, the Bank will conduct purchases in a flexible manner in accordance with financial market conditions. The average remaining maturity of the Bank’s JGB purchases will be about 7-12 years.

b) The Bank will purchase exchange-traded funds (ETFs) and Japan real estate investment trusts (J-REITs) so that their amounts outstanding will increase at annual paces of about 3 trillion yen4 and about 90 billion yen, respectively.

c) As for CP and corporate bonds, the Bank will maintain their amounts outstanding at about 2.2 trillion yen and about 3.2 trillion yen, respectively”.

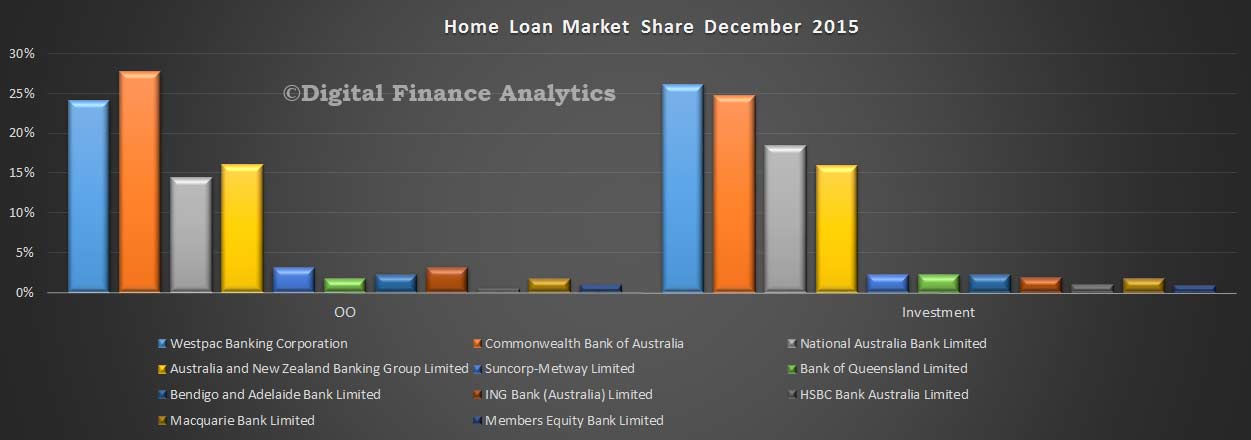

The latest data from APRA, the monthly banking stats to December, provide data on the stock of loans and deposits held by the banks. Total housing loans on book were $1.42 trillion, up 0.7% from last month. Within the mix, owner occupied loans grew 1% ($898 bn) and investment loans by 0.17% ($518 bn). There were no declared adjustments between owner occupied and investment loans this month (first clear result for several months). Investment loans were 36.6% of book, still a big number.

Looking at the individual lenders portfolios, CBA still has the largest owner occupied share, and Westpac the biggest share of investment loans.

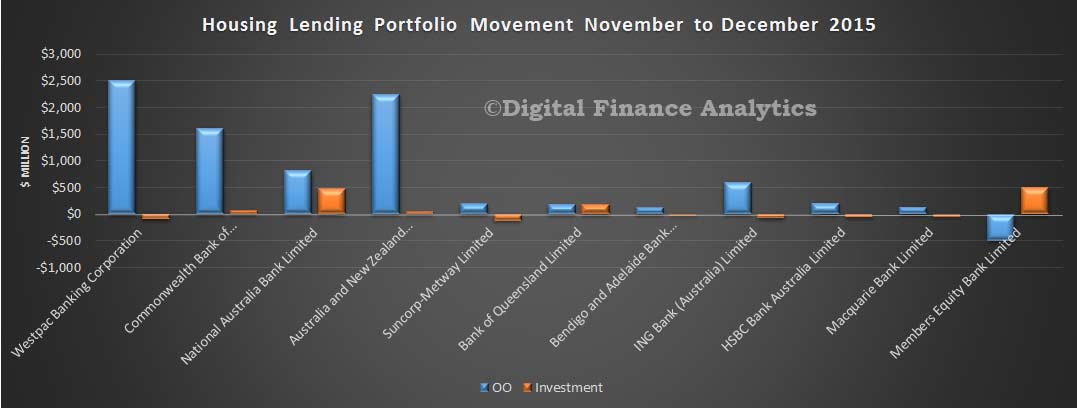

The main movements were in the owner occupied stream, with all the main lenders growing their footprint, other than Members Equity Bank who grew their investment loans. Among the majors, NAB made (net) most investment loans.

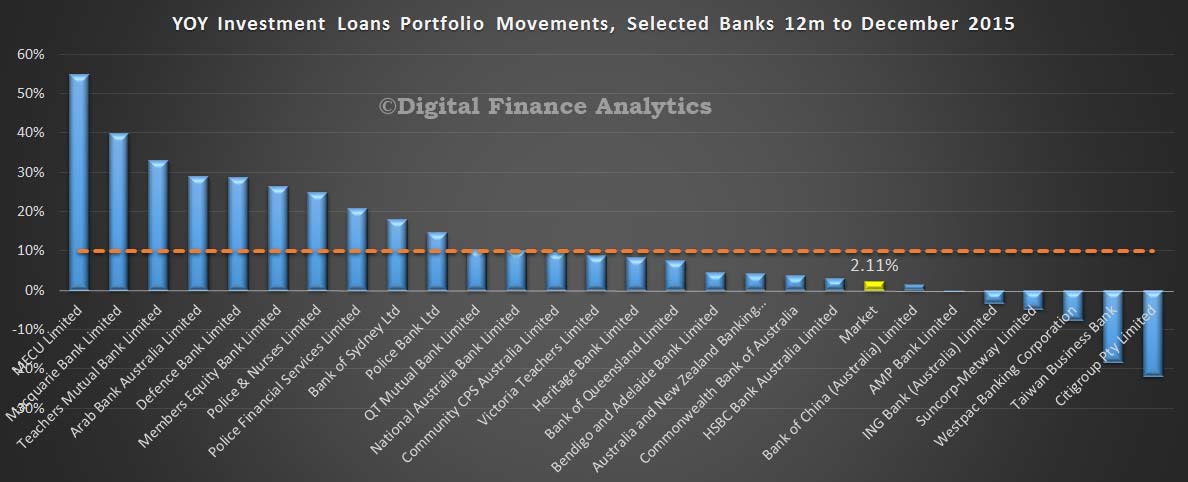

If we look at the 12 month portfolio movements by bank, we see that the investment loans market since January has now settled at 2.1% (after all the various tweaks and adjustments). This is below the APRA 10% speed limit. Now most of the major lenders are at or below the 10% hurdle, through a number of other players are still well above. Some, like Macquarie are explained by acquisitions, others by relative lending growth alone.

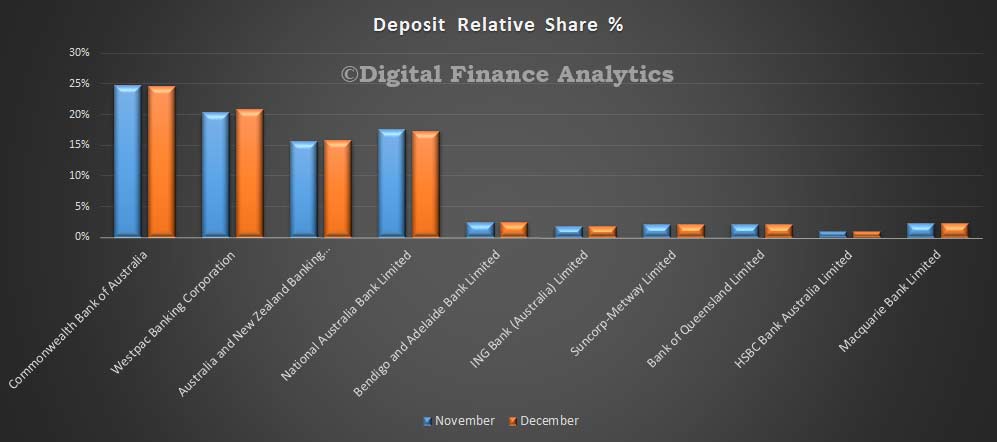

Turning to deposits, we see CBA still is the largest savings bank in Australia, though Westpac has been growing share, at the expense of NAB. Total deposits were $1.9 trillion, up $11 bn in the month – or 0.62%. This is a larger rise than the previous two months.

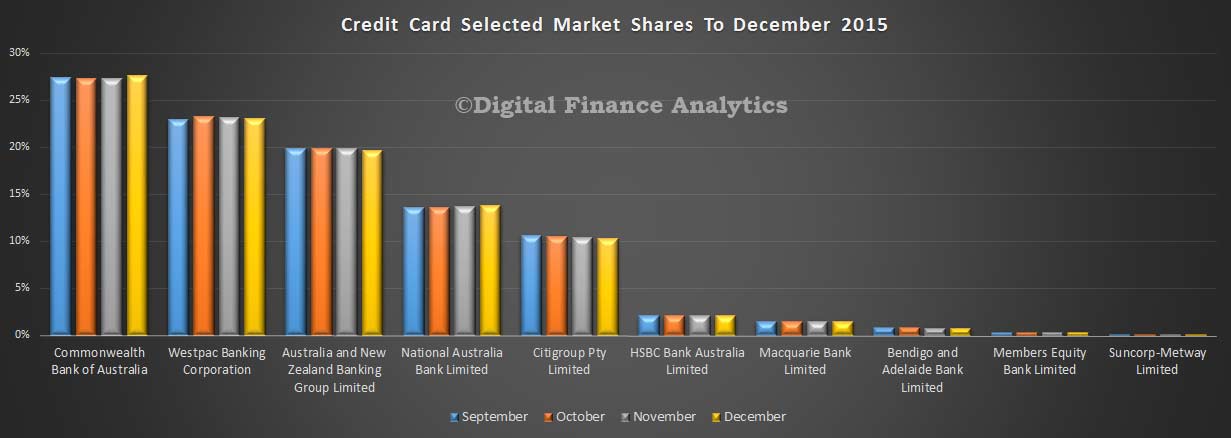

Looking at the cards portfolio, total balances were up slightly (thanks to Christmas) by $832 m to $42.2 bn. CBA lifted their share of cards balances, and they remain the largest cards player, followed by Westpac and ANZ Bank. We expect balances to fall in January as households repay their festive bloat.

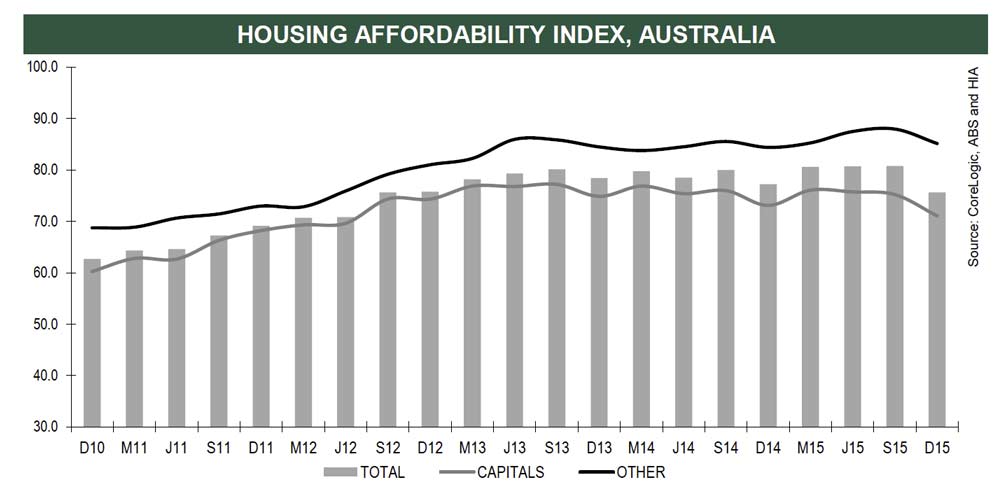

November’s increase in the major banks’ variable mortgage interest rate was a setback for housing

affordability, according to the latest Affordability Report from the Housing Industry Association.

Affordability deteriorated by some 6.4 per cent during the December 2015 quarter. Canberra saw the most unfavourable change in affordability (-11.4 per cent), with affordability worsening by 10.5 per cent in Melbourne and by 3.3 per cent in Sydney. Darwin was the only one of the eight capital cities to see improved affordability during the quarter. Just two of the seven regional markets covered by the report saw more favourable affordability during the December 2015 quarter.

“The unilateral increase in the major banks’ variable mortgage rates which came despite the absence of

any change in the official cash rate has delivered a significant blow to housing affordability,” noted HIA

Senior Economist, Shane Garrett.

“Combined with double-digit dwelling price growth in cities like Sydney and Melbourne, the shock jump

in interest rates has pushed home affordability to its least favourable position in over three years,”

Shane Garrett pointed out.

“The affordability challenge has been compounded by the slow pace of earnings growth which means

that the buying power of households has not kept pace with dwelling prices.”

“The increase in mortgage interest rates during November was an unpleasant surprise for homeowners, and housing affordability will be damaged even further if this tactic is repeated,” warned Shane Garrett.

“Governments must play their part too. Stamp duty is a huge source of woe for those trying to come up

with the funds for a home. HIA research has shown how the typical stamp duty bill of around $20,000

eventually costs homebuyers about $50,000 over the course of the mortgage due to higher LMI

premiums and mortgage interest costs. It’s time for this inefficient tax to be addressed,” concluded

Shane Garrett.

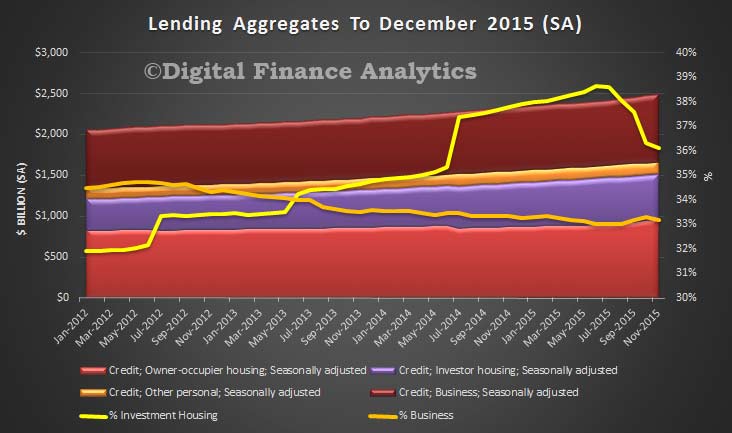

The RBA Credit Aggregates for December, released today, shows a continued rise in lending for housing, up 0.7% in the past month seasonally adjusted by $10.6 bn to $1.52 trillion. This includes all lending, including non-banks, seasonally adjusted. There are no reported series breaks this past month, so no abnormal shifts between investment and owner occupied loans . This is a rise of 7.1% over the past year.

The splits between owner occupied and investment lending shows that loans for owner occupation rose $10 bn, up 1.1%, to $967.7 billion. Loans for investment purposes also rose – just 0.09% or $0.49 billion to $546 billion, so investors are still in the market. The proportion of loans on book relating to investment lending has fallen again, to 36.1% from a high of 38.6% last year. This is still a big number, and higher that the levels which were thought to be a concern (as expressed by the regulators) last year, before recent swapping between categories. Remember the Bank of England is worried by their 16% share of investment loans – in Australia it is much higher!

Personal credit has fallen again, down 0.2% to $148 billion. But lending for business was only up 0.11%, or $0.94 billion to $826 billion. This represents a low 33.2% of all lending, down from 33.3% last month, and down from 34.7% in 2012. This continues to highlight the lack of investment in the grown engine of the economy – business – as compared to the easy money going towards housing. Structurally, we continue to have a problem, as housing growth is not productive and cannot lead to the right economic outcomes. Remember this is with interest rates at rock bottom.

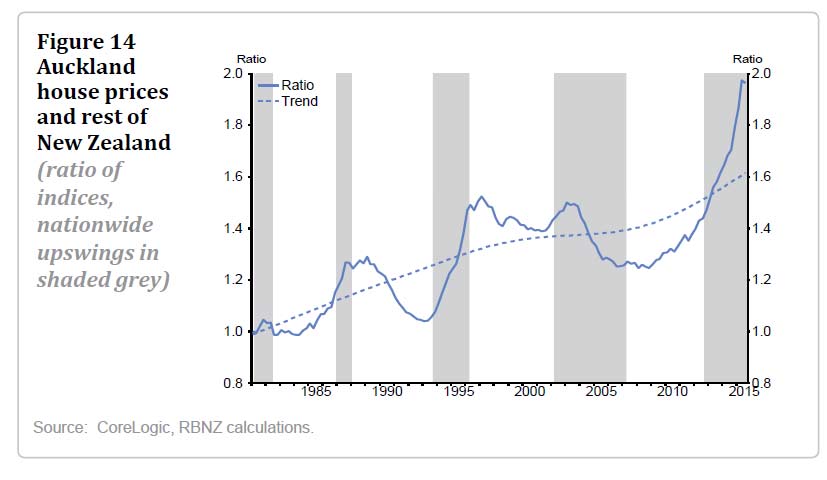

The Reserve Bank NZ, released a Bulletin today which looks at house price trends across New Zealand. Since mid-2012, Auckland house prices have increased 52 percent, but house prices in the rest of New Zealand have increased only 11 percent. The extent of this divergence is unprecedented.

Since 1981, house prices in Auckland have increased much more than those in the rest of New Zealand. House prices in North Island provinces – where house prices have grown the least – are only 63 percent higher than they were in 1981. By contrast, Auckland house prices are 352 percent higher.

Figure 14 shows Auckland house prices as a ratio to those in the rest of New Zealand. High average rates of house price inflation in Auckland relative to the rest of the country have seen this ratio trend upwards since 1981. The extent of the increase in this ratio since 2009 is unprecedented.

An upward trend in this ratio might be expected over time, but it is not clear how steep that trend should be, whether it is time-varying, or whether it will persist. Notwithstanding that uncertainty, the ratio is currently 22 percent above a simple filtered trend. A divergence of this magnitude is also evident when Auckland is compared with urban centres only. This means that the upward trend has not been driven by a more general divergence between house prices in urban and provincial centres, but is an Auckland-specific phenomenon.

In previous instances when the ratio has increased relatively quickly – namely, during the late 1980s and mid-1990s – this has subsequently been followed by a period of lower growth. In 1987, house prices in Auckland increased while they were flat in the rest of the country. Then in subsequent years, Auckland house prices fell while those in the rest of New Zealand continued increasing. In the upswing of the 1990s, Auckland house prices increased relative to the rest of the country, and stayed elevated until the latter part of the 2000s cycle, at which time house prices in the rest of the country increased at a faster pace than those in Auckland.

DFA believes that the same forces are at work here, as in Sydney, London and other metro centres. Lack of supply, high levels of finance available, investors active, foreign investors active, and weak regulatory control. The perfect storm.

John Fraser’s speech yesterday as Secretary to the Treasury, is significant because it does highlight some of the key issues driving future economic outcomes, and even our credit rating.

“The clear message is that we cannot rely on any cyclical bounce to reduce outlays as a percentage of GDP or, for that matter, the deficit. We are not in a crisis. But the Budget is rightly a focus of attention”.

“We have a structural budget problem that arose before the global financial crisis. A very substantial amount of the revenue windfall was used to lock-in long-term spending commitments”.

“Much of the deterioration in the budget position has been the result of revenue collections falling short of forecasts as we experience the flipside of the mining investment boom”.

“As a result, at 25.9 per cent of GDP, spending in 2015 16 is forecast to be close to the post-GFC peak, and could have been higher were it not for the measures taken by the Government in MYEFO”.”The Commonwealth’s interest bill has reached over a billion dollars a month. This is projected to more than double within the decade, unless action is taken to improve our budgetary position”.

“The Commonwealth achieving surpluses means that the States can run small overall deficits that they can use to finance productive infrastructure investment. This was a key conclusion of the 1993 National Savings Report commissioned by the then Treasurer, John Dawkins. In my view, this is still a sound framework for thinking about fiscal policy today. The rising structural deficits and debt give rise to intergenerational issues”.

“Around two-thirds of Commonwealth public debt is held by non-resident investors. This share has risen since 2009 and remains historically high. This, if anything, leaves Australia’s fiscal position a little more exposed to shocks in global capital markets”.

“It’s important that Australia maintain its top credit ratings, which helps to contain the costs associated with servicing public debt. Australia is one of only ten countries with a triple A credit rating from all three of the major rating agencies, reflecting our reputation for fiscal prudence”.

“But there have also been a number of policy decisions over recent years that have pushed the ratio higher: including increasing base pensions and supplementary payments, increased Defence operations and border protection spending, expenditure related to the carbon compensation package and the outcomes of negotiations around the repeal of the Minerals Resource Rent Tax. And the Government continues to face spending pressures”.

“There are many worthwhile spending programs and, every year, there are more good ideas than government resources to support them. There is also often, a mismatch between what the community expects the government to support and what they are prepared to pay for either in tax or in user charges. In framing budgets, we are really asking ourselves now and in the longer term what sort of society we want to have”.

“The ageing of Australia’s population will weigh heavily on Australia’s potential growth rate and long-term fiscal position. Demographic and broader medium-term pressures will place greater demands on government finances, making deficit and debt reduction more difficult”.

“Structural reform is critical and this includes reforming competition policy and implementing the Harper Review recomendations”.

“Improving productivity is a far more sustainable way to boost economic growth than relying unduly on an exchange rate depreciation”.

“These growth-enhancing policies also very much include tax reform. Tax is not just about raising revenue, it is also about helping to shape the economy so that we attract and deploy resources in a manner to promote long term growth. The arguments for a tax mix switch rest heavily on encouraging more jobs through a higher growth path. Tax reform is a complex issue and is very much the focus of the Government at the current time”.

Recent turbulence in the share markets has caused some experts to point the finger of culpability at computerised High-Frequency Trading (HFT). There are few complaints about HFT when computers push share markets up, but in the ebbing tide of today’s markets, it’s blamed both for exaggerating the share market dive as well as for the heightened volatility.

The logic behind the fears is this: algorithms and software do not muse about global economic events; they merely chase mechanical patterns that they are programmed to find, such as movements in trend or momentum. They do not make decisions based on real-world eventualities, such as political events.

Can the algorithms express a view on Chinese consumer confidence? The economic impacts of Middle-Eastern sectarian conflicts? These real world factors aren’t taken into account in the programming of algorithms.

Yet the computers hold substantial sway and can execute a barrage of trades that create unprecedented volatility at a rate that human reactions simply cannot match.

What is truly problematic is that the algorithms are not cognisant of when to stop or change a trade and thus can continue to pile money and exaggerate a trade well beyond what the market would consider a correct response. The computers do not have the ‘affirmative obligation’ to keep the markets orderly.

In fact, this sort of financial competition has been described as ‘a new world of a war between machines’.

Research has explained that stock prices tend to overreact to news when HFT activity is at a high volume, and that this can have ‘harmful effects’ for capital markets. Additionally, financial experts have found that HFT “exacerbates the adverse impacts of trading-related mistakes”, while also leading to “extremely higher market volatility and surprises about suddenly-diminished liquidity”, which in turn “raises concerns about the stability and health of the financial markets for regulators.”

In Australia HFT has made significant inroads into the market. In 2015 it accounted for nearly one-third of all equity market trades, a level similar to Canada, the European Union, and Japan.

ASIC estimates that HFTs in Australia are collectively earning an not inconsequential $100 million to $180 million annually.

Securities regulators have tolerated HFT so far, but as we may be entering a “new normal” of higher volatility and with algorithms helping exert a downward pressure on the markets, the regulators may find themselves revisiting the HFT issue.

Australian financial traders may also be put in jeopardy by the sheer magnitude of large foreign-funded HFT players. In recent times, the incursion of HFT into other asset classes such as interest rates futures has shown that local traders are being forced out by the computing power of internationally-funded “flash boys”.

Nonetheless, the track record of Australian regulators has been very positive and they have been proactive about creating mechanisms such as ‘kill switches’ to mitigate potential losses.

From a theoretical standpoint, the proponents of HFT have argued that it provides the most up-to-date information and thus facilitates price discovery. However, if the algorithms are merely exaggerating sentiments by moving large sums at instantaneous speeds – then they are not facilitating price discovery but in fact preventing that goal from being achieved.

The movie, The Big Short, based on the book by Michael Lewis, (who also wrote about “flash boys”) has infused narratives of the financial world with a “human element”. They have put faces to the names we read about in financial scandals.

However, if HFT grows in size and share markets continue to perform negatively, it may be that the computerised antagonists of finance’s future, the diaboli ex machina, may have no face at all.

Author: Usman W. Chohan, Doctoral Candidate, Economics, Policy Reform, UNSW Australia