Macquarie Group announced a net profit after tax attributable to ordinary shareholders of $A1,070 million for the half-year ended 30 September 2015 (1H16), up 58 percent on the half-year ended 30 September 2014 (1H15) and up 16 percent on the half-year ended 31 March 2015 (2H15). Net operating income of $A5.3 billion for 1H16 increased 24 percent on 1H15, while total operating expenses of $A3.7 billion for 1H16 increased 17 percent on 1H15. Return on equity was 15.8%.

Macquarie’s annuity-style businesses (Macquarie Asset Management (MAM), Corporate and Asset Finance (CAF) and Banking and Financial Services (BFS)) continued to perform well, with 1H16 combined net profit contribution up 38 percent on 1H15. Macquarie’s capital markets facing businesses (Macquarie Securities (MSG), Macquarie Capital and Commodities and Financial Markets (CFM)) continued to improve with combined net profit contribution up 66 percent on 1H15.

Net operating income of $A5.3 billion in 1H16 was up 24 percent on 1H15 and up seven percent on 2H15, while operating expenses of $A3.7 billion were up 17 percent on 1H15 and up three percent on 2H15.

International income accounted for 71 percent of the Group’s total income for 1H16. A 10 percent movement4 in the Australian dollar is estimated to have approximately seven percent impact on full year net profit. Given currency movements, Macquarie estimates approximately a quarter of the increase in 1H16 net profit on 1H15 is attributable to foreign exchange.

The effective tax rate of 33.1 percent was down from 38.9 percent in 1H15 and down on the full year ended 31 March 2015 (FY15).

Macquarie’s assets under management (AUM) at 30 September 2015 were $A504 billion, up four percent on 31 March 2015.

Key drivers of the change from the prior corresponding period were:

- A 38 percent increase in combined net interest and trading income to $A2.3 billion, up from $A1.6 billion in 1H15, with key drivers being improved trading opportunities in MSG driven by increased market volatility, increased client activity across most of the CFM platforms as a result of price volatility, the accretion of interest income on loans acquired at a discount and the favourable impact of the depreciation of the Australian dollar, partially offset by increased funding costs associated with growth of the operating lease portfolio in CAF and strong volume growth in Australian mortgages, business lending and deposits in BFS.

- A 29 percent increase in fee and commission income to $A2.8 billion, up from $A2.2 billion in 1H15, primarily driven by a significant increase in MAM performance fees; an increase in MAM base fees, largely due to higher AUM that benefited from favourable currency and market movements, fund raisings and investments in Macquarie Infrastructure and Real Assets (MIRA), together with net flows into higher fee margin products in Macquarie Investment Management (MIM); increased mergers and acquisitions, advisory and underwriting fees in Macquarie Capital; as well as increased brokerage and commissions income in MSG.

- A 31 percent decrease in other operating income and charges to $A0.3 billion, down from $A0.5 billion in 1H15, due to an increase in impairment charges and collective provisions particularly in CFM and Macquarie Capital, partially offset by an increase in net operating lease income in CAF.

- A 17 percent increase in total operating expenses, driven by higher employment expenses primarily due to higher staff compensation resulting from the improved performance of the Group, increased brokerage, commission and trading-related expenses driven by increased trading-related activity in MSG, higher non-salary technology expenses due to ongoing investment in technology projects to support business growth, and an increase in other operating expenses resulting from increased activity across Macquarie and the amortisation of capitalised technology costs. Overall operating expenses were also impacted by the depreciation of the Australian dollar on offshore expenses.

Staff numbers were 13,582 at 30 September 2015, down from 14,085 at 31 March 2015.

Macquarie also announced today an interim dividend of $A1.60 per share, 40 percent franked, up from the 1H15 dividend of $A1.30 per share and down from the 2H15 dividend of $A2.00 per share, both 40 percent franked. This represents a payout ratio of 51 percent. The record date is 11 November 2015 and the payment date for the interim dividend is 16 December 2015.

While the impact of future market conditions makes forecasting difficult, it is currently expected that the combined net profit contribution from operating groups for the year ending 31 March 2016 (FY16) will be up on FY15.

The income tax expense for 1H16 was $A530 million, up 23 percent from $A432 million in the prior corresponding period. The effective tax rate of 33.1 percent was down on FY15.

Total customer deposits increased 7.8 percent from 31 March 2015 to $A42.8 billion at 30 September 2015. During 1H16, $A10.3 billion of term funding was raised covering a range of sources, tenors, currencies and product types as well as $A4.0 billion raised as an AWAS Aviation Capital Limited (AWAS) acquisition debt facility.

During 1H16, Macquarie completed the on-market purchase of shares to satisfy the FY15 Macquarie Group Employee Retained Equity Plan (MEREP) requirements of $A383 million at a weighted average price of $A80.68.

In October 2015, the Group issued $A0.4 billion in equity via an Institutional Placement (Placement) to provide capital for the acquisition of the Esanda dealer finance portfolio from ANZ Banking Group. An associated Share Purchase Plan (SPP) will be offered to eligible shareholders in Australia and New Zealand from 2 November 2015, who can apply for shares with a dollar value of up to $A10,000. If eligible shareholders participated in the March 2015 SPP, the maximum value of shares allocated from both the March 2015 SPP and this offer is limited to $A15,000. The record date for participation in the SPP was 7 October 2015 (the day prior to the launch of the Placement).

SPP Shares will not be eligible for the 1H16 dividend, however the offer price will be adjusted to reflect this. SPP shares will be offered at the lower of:

– $A78.40 representing the issue price paid under the Placement ($A80.00) less the 1H16 dividend ($A1.60); and

– a 1.0 percent discount to the volume weighted average price of shares traded during the pricing period7.

Macquarie intends to redeem the Preferred Membership Interests $US400m hybrid in December 2015 and expects to replace these in due course.

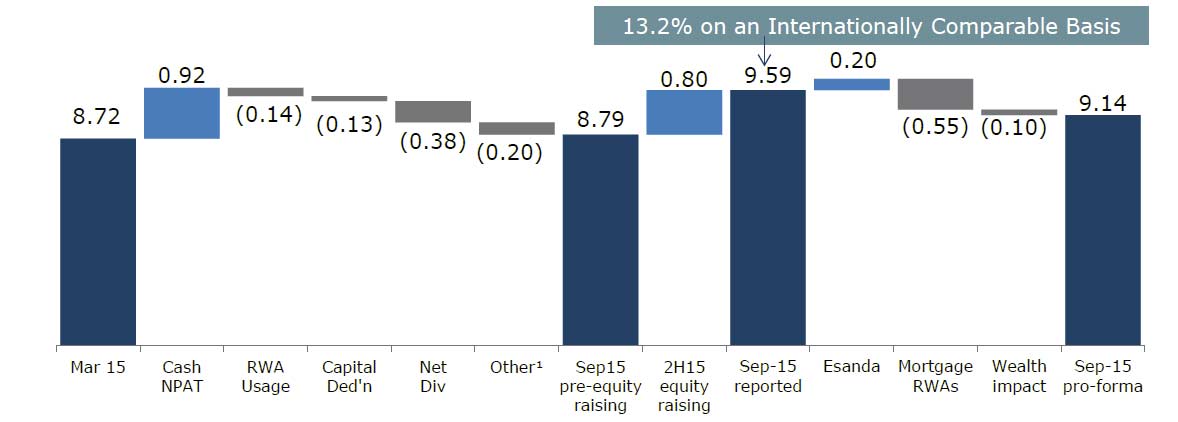

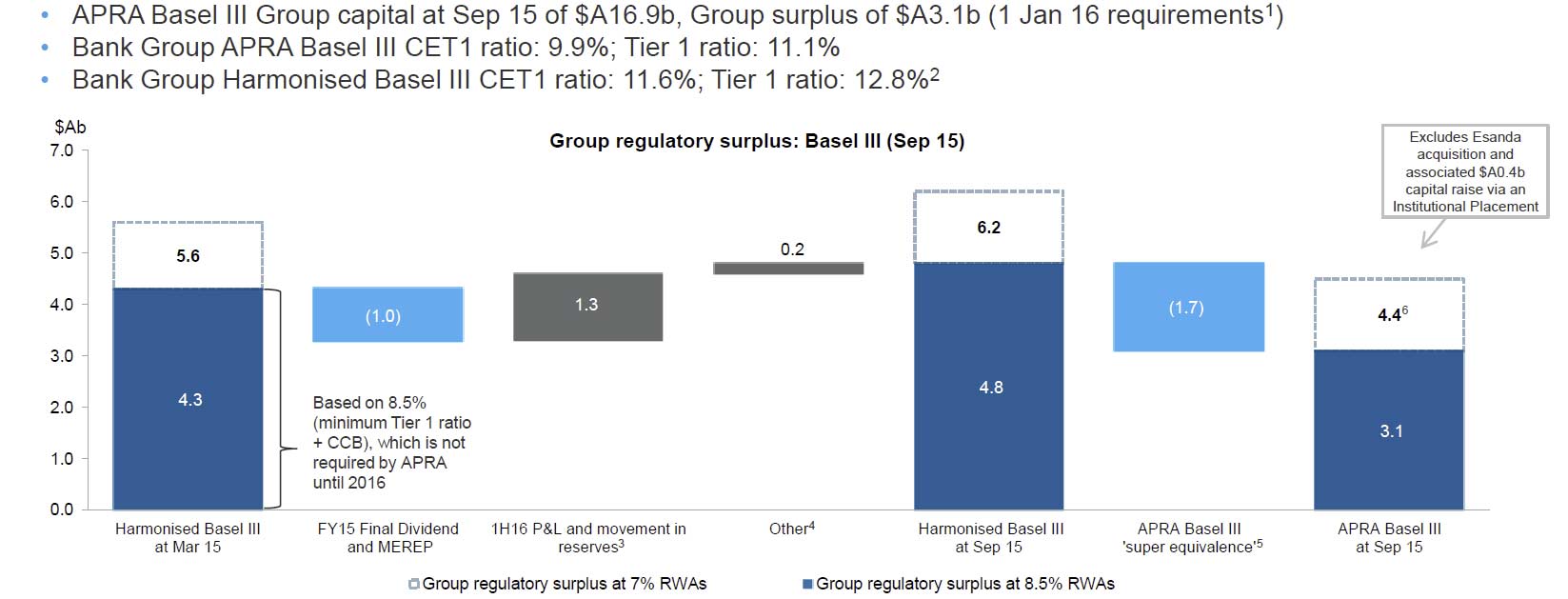

Macquarie Group remains very well capitalised with APRA Basel III Group capital of $A16.9 billion at 30 September 2015, a $A3.1 billion surplus to Macquarie’s minimum regulatory capital requirement from 1 January 2016. The Bank Group APRA Basel III Common Equity Tier 1 capital ratio was 9.9 percent at 30 September 2015, which was up from 9.7 percent at 31 March 2015.

In August 2014, APRA issued its final rules for Conglomerates with implementation timing yet to be announced. Macquarie continues to work through the application of the rules with APRA and the current assessment remains that Macquarie has sufficient capital to meet the minimum APRA capital requirements for Conglomerates.

In August 2014, APRA issued its final rules for Conglomerates with implementation timing yet to be announced. Macquarie continues to work through the application of the rules with APRA and the current assessment remains that Macquarie has sufficient capital to meet the minimum APRA capital requirements for Conglomerates.

The government released its response to the Financial System Inquiry on 20 October 2015, agreeing with the majority of the recommendations and setting a timetable for their implementation. The government endorsed APRA to implement most of the resilience recommendations and so the final design of any policy changes has yet to be determined.

Based on finalised BCBS leverage ratio requirements9 released in January 2014, the Bank Group is well in excess of the currently proposed Basel III 3.0 percent minimum10, with a 6.0 percent leverage ratio as at 30 September 2015. APRA’s ‘super equivalence’ in relation to the definition of capital carries over to the leverage ratio. On an APRA basis, the Bank Group’s leverage ratio is 5.1 percent as at 30 September 2015.

Liquidity Coverage Ratio (LCR) requirements came into effect from 1 January 2015, with disclosure required from 1 July 2015. For the quarter ended September 2015 the Bank Group’s average LCR was 170 percent11.

Operating Group performance:

- Macquarie Asset Management (MAM) net profit contribution of $A1,139 million for 1H16 increased 45 percent from $A785 million in 1H15. MAM’s base fee income of $A784 million for 1H16 increased 22 percent from $A641 million in 1H15, largely due to increased AUM that benefited from favourable currency and market movements, fund raisings and investments in MIRA, together with net flows into higher fee margin products in MIM. Performance fees of $A609 million for 1H16 increased significantly from $A373 million in 1H15, including performance fees from Macquarie Infrastructure Corporation (MIC) and Macquarie European Infrastructure Fund 1 (MEIF1), as well as performance fee income from co-investors in respect of a UK asset.

- Corporate and Asset Finance (CAF) net profit contribution of $A611 million for 1H16 increased 31 percent from $A468 million in 1H15. The improved result was largely driven by the favourable impact of the depreciation of the Australian dollar, the accretion of interest income on loans acquired at a discount in the Lending portfolio and increased net operating lease income mainly due to the contribution of aircraft acquired to date from AWAS. CAF’s asset and loan portfolio increased 13 percent from $A28.7 billion at 31 March 2015 to $A32.3 billion at 30 September 2015 mainly driven by the impact of the depreciation of the Australian dollar, the acquisition of aircraft during the period as well as and the acquisition of Advantage Funding in July 2015.

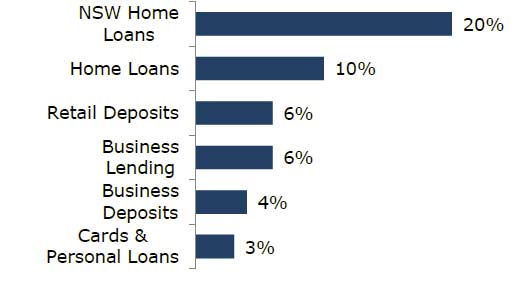

- Banking and Financial Services (BFS) net profit contribution of $A170 million for 1H16 increased 21 percent from $A141 million in 1H15. In 1H16, BFS benefited from strong volume growth in Australian mortgages, business lending and deposits partially offset by increased investment in technology projects to support growth in the business, including the development of a new Core Banking system. The Australian mortgage portfolio increased to $A27.6 billion, up 13 percent on 31 March 2015, representing approximately 1.8 percent of the Australian mortgage market. Macquarie platform assets under administration were broadly in line with 31 March 2015 at $A46.7 billion.

- Macquarie Securities Group (MSG) net profit contribution of $A240 million for 1H16 increased significantly from $A17 million in 1H15. MSG benefited from improved market and trading conditions in Australia and Asia due to increased market volatility, particularly in China, driving strong growth in trading-related income as well as increased brokerage and commissions income. Income growth was partly offset by increased operating expenses relative to 1H15 driven by the depreciation of the Australian dollar.

- Macquarie Capital net profit contribution of $A170 million for 1H16 increased 13 percent from $A150 million in 1H15 predominately due to increased mergers and acquisitions fee revenue, particularly in Australia and the US, partially offset by increased impairment charges relating to certain underperforming principal investments. During 1H16, Macquarie Capital advised on 208 transactions valued at $A116b including acting as joint lead manager and joint underwriter on National Australia Bank’s $A5.5b accelerated renounceable entitlement offer and financial adviser, debt and equity arranger to Freeport LNG on its $US4.6b project financing of Train 3 of its Liquefaction and Export Project.

- Commodities and Financial Markets (CFM) net profit contribution for 1H16 was $A282 million, an increase of 13 percent from $A250 million in 1H15. This result reflected improved returns across the commodities trading platform and the favourable impact of the depreciation in the Australian dollar while income from credit, interest rates and foreign exchange markets remained flat compared with 1H15. These were partially offset by higher provisions for impairments taken on certain underperforming commodity related loans.